![]()

Search Market Research Report

Blood and Fluid Warmer Market Size, Share Global Analysis Report, 2026-2034

Blood and Fluid Warmer Market Size, Share, Growth Analysis Report By Product (Portable, Stationary, and Others), By Application (Surgery, Acute Care, Newborn Care, Preoperative Care, Homecare, and Others), By End User (Hospitals, Clinics, Ambulatory Services, Blood Banks, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

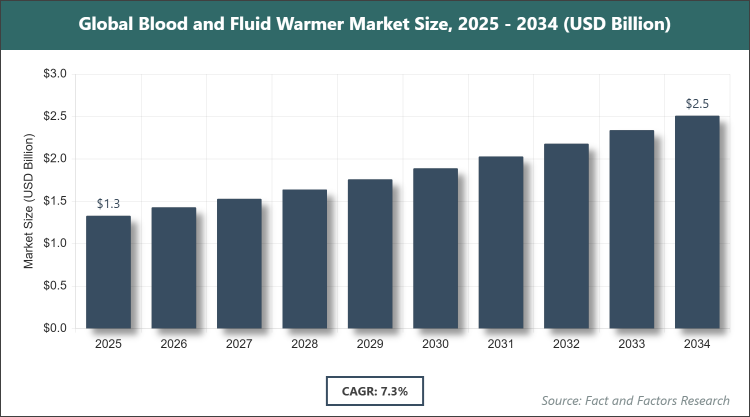

[232 Pages Report] According to Facts & Factors, the global blood and fluid warmer market size was estimated at USD 1.33 billion in 2025 and is expected to reach USD 2.51 billion by the end of 2034. The Blood and Fluid Warmer industry is anticipated to grow by a CAGR of 7.3% between 2026 and 2034. The Blood and Fluid Warmer Market is driven by increasing surgical procedures and rising awareness of hypothermia prevention in medical settings.

Market Overview

Market Overview

The blood and fluid warmer market encompasses the development, manufacturing, and distribution of medical devices designed to heat intravenous fluids, blood, and blood products to body temperature before administration, preventing hypothermia in patients during surgeries, trauma care, and other medical procedures, thereby improving patient outcomes and safety in healthcare environments ranging from hospitals to ambulatory settings. This market involves technological advancements in portable and stationary systems to ensure efficient warming without compromising fluid integrity, addressing critical needs in emergency and routine medical care while integrating with broader patient temperature management strategies.

Key Insights

- As per the analysis shared by our research analyst, the Blood and Fluid Warmer market is expected to grow at a CAGR of 7.3% during the forecast period of 2026-2034.

- In terms of revenue, the Blood and Fluid Warmer market size was valued at about USD 1.33 billion in 2025 and is expected to reach USD 2.51 billion by 2034.

- The Blood and Fluid Warmer market is driven by increasing surgical procedures and rising awareness of hypothermia prevention in medical settings.

- Based on the product, the Portable segment dominated the market with a share of 60% in 2025 due to its flexibility and suitability for emergency and pre-hospital use, enabling rapid deployment in diverse clinical scenarios.

- Based on the application, the Surgery segment dominated the market with a share of 45% in 2025 owing to the high volume of intraoperative procedures requiring precise temperature management to reduce complications.

- Based on the end user, the Hospitals segment dominated the market with a share of 70% in 2025 because of the extensive use in inpatient care and surgical units with advanced infrastructure.

- North America dominated the market with a share of 40% in 2025 due to robust healthcare infrastructure, high surgical volumes, and strong adoption of advanced medical technologies.

Growth Drivers

- Increasing Number of Surgical Procedures

The rising global volume of surgeries, driven by aging populations and advancements in medical treatments, is boosting demand for blood and fluid warmers to maintain normothermia and prevent perioperative hypothermia, which can lead to complications like infections and prolonged recovery. This driver is supported by expanding healthcare access in developing regions.

Furthermore, integration with surgical protocols and guidelines from organizations like WHO emphasizes temperature management, fostering adoption through training and standardization in operating rooms worldwide.

- Rising Awareness of Hypothermia Risks

Heightened recognition among healthcare professionals of hypothermia's adverse effects on patient outcomes is propelling warmer usage in trauma and critical care, aligned with evidence-based practices and quality improvement initiatives. This is amplified by educational campaigns and research highlighting benefits.

Additionally, reimbursement policies for preventive devices in developed markets incentivize procurement, sustaining growth through cost-benefit analyses demonstrating reduced hospital stays and complications.

- Technological Advancements

Innovations in portable, battery-operated warmers with precise temperature control are enhancing usability in diverse settings, attracting investments and expanding applications beyond hospitals. This includes smart features for monitoring and alerts.

Moreover, collaborations between tech firms and medical device manufacturers are accelerating product development, improving efficacy and user-friendliness to meet evolving clinical needs.

Restraints

- High Device Costs

The elevated price of advanced warmers limits adoption in resource-constrained settings, particularly in developing countries where budget constraints prioritize essential equipment. This is compounded by maintenance expenses.

Strategies like cost-effective models and financing options are emerging, but slow implementation hinders broader market penetration.

- Regulatory Compliance Challenges

Stringent approval processes and standards for medical devices delay market entry and increase development costs, affecting innovation pace. This varies by region, complicating global strategies.

Harmonization efforts and streamlined pathways are needed, though ongoing scrutiny ensures safety but restrains agility.

Opportunities

- Expansion in Emerging Markets

Growing healthcare infrastructure in Asia and Latin America offers potential for affordable warmers, with increasing trauma cases and surgeries creating demand. This aligns with government investments.

Local manufacturing partnerships can reduce costs, unlocking access to untapped populations.

- Integration with Telemedicine

Combining warmers with remote monitoring enhances pre-hospital care, opening avenues in ambulance services. This leverages digital health trends.

R&D in connected devices can improve outcomes, attracting funding for innovative solutions.

Challenges

- Competition from Alternatives

Availability of passive warming methods like blankets diverts adoption, especially in low-acuity settings. This requires education on superior efficacy.

Differentiation through evidence is key to overcoming preferences for simpler options.

- Supply Chain Vulnerabilities

Disruptions in component sourcing affect production, leading to shortages. This demands diversified suppliers.

Building resilience through local sourcing mitigates risks, though initial adjustments are challenging.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.33 Billion |

Projected Market Size in 2034 |

USD 2.51 Billion |

CAGR Growth Rate |

7.3% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Stryker Corporation, Gentherm Medical, Belmont Medical, 3M, ICU Medical, Vyaire Medical, Inc., The Surgical Company, Life Warmer, MEQU, Estill Medical Technologies, Inc., Smisson-Cartledge Biomedical, Biegler GmbH, Smiths Medical, QinFlow Inc., Baxter International Inc., and Others. |

Key Segment |

By Product, By Application, By End User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Blood and Fluid Warmer market is segmented by product, application, end user, and region.

Based on Product Segment, the blood and fluid warmer market is divided into Portable, Stationary, and others. The most dominant segment is Portable, leading due to its mobility for emergency and transport use, reducing hypothermia risks in pre-hospital scenarios and driving market growth through versatility in critical care; the second most dominant is Stationary, preferred in fixed settings like operating rooms for consistent high-volume warming, contributing to expansion by supporting routine surgical demands.

Based on Application Segment, the blood and fluid warmer market is divided into Surgery, Acute Care, Newborn Care, Preoperative Care, Homecare, and others. The most dominant segment is Surgery, dominating owing to essential normothermia maintenance during operations, boosting growth via reduced complications; the second most dominant is Acute Care, vital for trauma patients, aiding market drive in emergency departments.

Based on End User Segment, the blood and fluid warmer market is divided into Hospitals, Clinics, Ambulatory Services, Blood Banks, and others. The most dominant segment is Hospitals, commanding leadership due to high procedural volumes and infrastructure, propelling overall growth; the second most dominant is Ambulatory Services, growing with outpatient trends, supporting portability needs.

Recent Developments

- In June 2024, MEQU received 510(k) clearance from the U.S. FDA for its °M Warmer System, a portable blood and IV fluid warming device designed for military and civilian applications, enabling expansion into the U.S. market.

- In April 2024, TSC Life launched its direct sales operations in the UK, focusing on increasing customer engagement and providing personalized support for blood warming products.

- In January 2025, Smiths Medical launched a new compact and portable blood warmer device for emergency and pre-hospital settings, enhancing mobility and usability.

- In December 2024, ThermoMedic Systems acquired VitalCare Technologies, expanding its portfolio in mobile blood warming systems for emerging markets.

- In November 2024, Becton Dickinson announced a strategic partnership with CareFusion to develop smart blood warmer devices integrated with real-time patient monitoring.

- In June 2023, QinFlow Inc. and Life-Assist completed a distribution partnership for the Warrior line of high-performance portable blood and IV fluid warmers.

- In April 2023, Baxter International Inc. unveiled the new Baxter Patient Warming system, including innovations for surgical applications.

Regional Analysis

- North America to dominate the global market

North America holds the forefront in the blood and fluid warmer market, with the United States as the dominating country, benefiting from advanced healthcare systems and high surgical rates that necessitate precise temperature management, while robust R&D ecosystems foster innovations in portable devices, supported by favorable reimbursements and awareness campaigns on hypothermia prevention, enabling widespread adoption across hospitals and emergency services.

Europe follows closely, dominated by Germany, where stringent patient safety regulations drive demand for efficient warmers in operating theaters, with collaborative healthcare networks enhancing distribution, alongside aging populations increasing procedural needs, and emphasis on sustainable medical technologies integrating eco-friendly features to meet EU standards.

Asia Pacific is rapidly expanding, led by China, fueled by urbanization and rising trauma incidents requiring quick warming solutions, with government investments in hospital infrastructure boosting accessibility, while local manufacturing reduces costs, catering to diverse clinical settings from urban centers to rural areas.

Latin America exhibits promising growth, with Brazil as the key country, driven by improving healthcare access and surgical advancements addressing hypothermia in tropical climates, supported by international partnerships introducing advanced warmers, and focus on emergency care in densely populated regions.

The Middle East & Africa region is emerging, dominated by South Africa, where increasing medical tourism and infrastructure developments promote warmer usage in surgeries, aided by aid programs enhancing equipment availability, and regional collaborations improving training for effective implementation in varied healthcare environments.

Competitive Analysis

The global Blood and Fluid Warmer market is dominated by players:

- Stryker Corporation

- Gentherm Medical

- Belmont Medical

- 3M

- ICU Medical

- Vyaire Medical, Inc.

- The Surgical Company

- Life Warmer

- MEQU

- Estill Medical Technologies, Inc.

- Smisson-Cartledge Biomedical

- Biegler GmbH

- Smiths Medical

- QinFlow Inc.

- Baxter International Inc.

The global Blood and Fluid Warmer market is segmented as follows:

By Product

- Portable

- Stationary

- Others

By Application

- Surgery

- Acute Care

- Newborn Care

- Preoperative Care

- Homecare

- Others

By End User

- Hospitals

- Clinics

- Ambulatory Services

- Blood Banks

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Blood and Fluid Warmer market is dominated by players:

Stryker Corporation

Gentherm Medical

Belmont Medical

3M

ICU Medical

Vyaire Medical, Inc.

The Surgical Company

Life Warmer

MEQU

Estill Medical Technologies, Inc.

Smisson-Cartledge Biomedical

Biegler GmbH

Smiths Medical

QinFlow Inc.

Baxter International Inc.

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors