![]()

Search Market Research Report

Aviation Test Equipment Market Size, Share Global Analysis Report, 2026-2034

Aviation Test Equipment Market Size, Share, Growth Analysis Report By Equipment Type (Electrical Aviation Test Equipment, Hydraulic Aviation Test Equipment, Pneumatic Aviation Test Equipment, Avionics Test Equipment, and Others), By Application (Commercial Aviation, Military Aviation), By End-User (Original Equipment Manufacturers, Maintenance Repair and Overhaul, Airlines and Operators, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

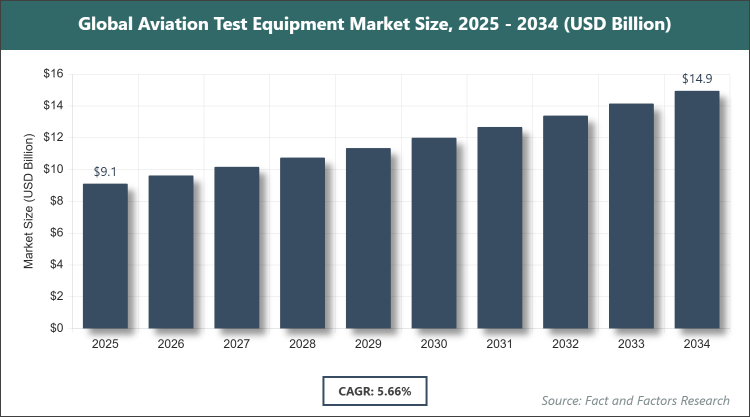

[225+ Pages Report] According to Facts & Factors, the global Aviation Test Equipment market size was estimated at USD 9.11 billion in 2025 and is expected to reach USD 14.87 billion by the end of 2034. The Aviation Test Equipment industry is anticipated to grow by a CAGR of 5.66% between 2026 and 2034. The Aviation Test Equipment Market is driven by the growing complexity of aircraft systems, fleet modernization programs, and the increasing emphasis on predictive maintenance and regulatory compliance.

Market Overview

Market Overview

The aviation test equipment market encompasses a wide range of specialized instruments, systems, and software designed to evaluate, diagnose, and verify the performance and safety of aircraft components and subsystems. These tools are critical for ensuring airworthiness, operational efficiency, and compliance with international aviation standards across commercial, military, and general aviation sectors. From electrical and hydraulic testers to advanced avionics diagnostic platforms, the equipment supports everything from routine inspections to complex system integrations during manufacturing, maintenance, repair, and overhaul activities.

As aviation technology evolves toward more electric, connected, and autonomous aircraft, the demand for sophisticated, automated, and data-driven testing solutions continues to rise. The market plays a foundational role in the broader aerospace ecosystem, bridging design validation, production quality assurance, and lifecycle support to minimize downtime, reduce costs, and enhance overall flight safety.

Key Insights

- As per the analysis shared by our research analyst, the global aviation test equipment market is estimated to grow annually at a CAGR of around 5.66% over the forecast period (2026-2034).

- In terms of revenue, the global aviation test equipment market size was valued at around USD 9.11 billion in 2025 and is projected to reach USD 14.87 billion by 2034.

- The market is driven by the rising complexity of modern aircraft electronics, increasing air traffic, fleet expansion, and stringent safety regulations.

- Based on the equipment type segment, the electrical aviation test equipment dominated the market with approximately 38% share because of its critical role in testing the growing number of electrical and electronic systems in next-generation aircraft.

- Based on the application segment, the commercial aviation segment dominated with over 58% share due to the massive global commercial fleet size and the need for continuous maintenance to support high utilization rates.

- Based on the end-user segment, the maintenance repair and overhaul providers dominated with around 42% share as airlines and operators increasingly outsource testing to specialized MRO facilities for cost efficiency and expertise.

- Based on the region segment, North America dominated the global market with over 42% share due to its established aerospace infrastructure, high defense spending, and leadership in aircraft manufacturing and innovation.

Growth Drivers

- Advancements in Aircraft Technology and Electrification

The shift toward more electric aircraft (MEA) and hybrid-electric propulsion systems has significantly increased the demand for advanced electrical and avionics test equipment. Modern aircraft incorporate thousands of sensors, digital flight controls, and integrated modular avionics that require precise, high-speed testing to ensure reliability and fault tolerance.

This technological evolution is further accelerated by the integration of artificial intelligence, machine learning, and predictive analytics into test platforms, enabling real-time diagnostics and reducing human error during maintenance operations.

- Expansion of Global Air Travel and Defense Budgets

Rising passenger traffic, particularly in emerging markets, combined with military modernization programs in major economies, is driving the need for expanded testing capabilities across both commercial and defense sectors. Governments and airlines are investing heavily in new aircraft acquisitions and retrofitting existing fleets to meet future demand.

These investments directly translate into higher procurement of test equipment for production lines, qualification testing, and ongoing operational support, creating a sustained growth momentum for the market.

Restraints

- High Initial Investment and Maintenance Costs

Advanced aviation test equipment often involves substantial capital expenditure, which can be prohibitive for smaller MRO providers and general aviation operators. The specialized nature of these systems also requires ongoing calibration, software updates, and skilled personnel to operate effectively.

Economic uncertainties and fluctuating global supply chain disruptions further exacerbate the challenge, leading some stakeholders to delay equipment upgrades in favor of legacy solutions.

Opportunities

- Integration of Digital Twin and IoT Technologies

The adoption of digital twin technology and Internet of Things (IoT) connectivity is opening new avenues for remote monitoring and cloud-based testing solutions. These innovations allow for predictive maintenance, reduced downtime, and more efficient resource allocation across global fleets.

Companies that develop modular, scalable test platforms capable of supporting multiple aircraft types and configurations are well-positioned to capture significant market share in the coming years.

Challenges

- Rapid Technological Obsolescence

The fast pace of innovation in avionics, propulsion, and materials science means that test equipment can quickly become outdated, requiring frequent upgrades or replacements. This creates a continuous cycle of investment and R&D pressure for both manufacturers and end-users.

Additionally, the lack of standardized testing protocols across different regions and regulatory bodies complicates global deployment and increases compliance costs.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 9.11 Billion |

Projected Market Size in 2034 |

USD 14.87 Billion |

CAGR Growth Rate |

5.66% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Honeywell International Inc., The Boeing Company, Airbus SE, Rolls-Royce Holdings plc, General Electric Company, Teradyne Inc., and Others. |

Key Segment |

By Equipment Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Aviation Test Equipment market is segmented by equipment type, application, end-user, and region.

Based on Equipment Type Segment, the Aviation Test Equipment market is divided into Electrical Aviation Test Equipment, Hydraulic Aviation Test Equipment, Pneumatic Aviation Test Equipment, Avionics Test Equipment, and others. Electrical aviation test equipment remains the most dominant segment because of the proliferation of electronic systems in aircraft, including flight management computers, power distribution units, and in-flight entertainment. This segment drives market growth by enabling comprehensive validation of safety-critical electrical architectures that are central to modern fly-by-wire and more-electric designs. Avionics test equipment ranks as the second most dominant segment, propelled by the increasing adoption of glass cockpits, satellite communications, and autonomous navigation systems that demand highly specialized diagnostic tools for signal integrity and software verification.

Based on Application Segment, the Aviation Test Equipment market is divided into Commercial Aviation and Military Aviation. Commercial aviation holds the leading position due to the sheer volume of passenger and cargo aircraft in operation worldwide, coupled with the need for frequent, rigorous testing to maintain high dispatch reliability and comply with civil aviation authorities. This segment fuels overall market expansion by supporting the high-utilization business models of low-cost carriers and major airlines. Military aviation follows closely as the second most dominant segment, benefiting from defense modernization initiatives that prioritize advanced weapons systems, stealth technologies, and unmanned platforms requiring mission-critical testing capabilities.

Based on End-User Segment, the Aviation Test Equipment market is divided into Original Equipment Manufacturers, Maintenance Repair and Overhaul, Airlines and Operators, and others. Maintenance repair and overhaul providers represent the dominant end-user category, as they handle the bulk of testing activities for both scheduled and unscheduled maintenance across global fleets. Their dominance stems from the ability to leverage shared test resources and expertise, thereby lowering costs for airlines while ensuring regulatory compliance. Original equipment manufacturers rank as the second most dominant end-user, driving market growth through their role in production testing, type certification, and the integration of new technologies during aircraft assembly.

Recent Developments

- In late 2025, Honeywell International Inc. introduced a new portable avionics test set featuring AI-driven fault prediction, significantly reducing diagnostic time for commercial operators by up to 40%.

- Teradyne Inc. expanded its partnership with Airbus in early 2026 to develop automated test solutions for next-generation A320neo family aircraft, focusing on electrical system integration testing.

- Rolls-Royce Holdings plc launched a cloud-based engine test platform in mid-2025 that allows real-time remote monitoring of Trent engine performance during MRO activities.

- In 2026, SPHEREA Test & Services announced the acquisition of a European test equipment startup to strengthen its capabilities in unmanned aerial vehicle diagnostics.

- Boeing and Collins Aerospace jointly unveiled an integrated test bench for electric vertical takeoff and landing (eVTOL) vehicles, targeting the emerging urban air mobility sector.

Regional Analysis

- North America to dominate the global market

North America leads the global aviation test equipment market with its robust aerospace manufacturing base and high concentration of major aircraft OEMs and defense contractors. The United States serves as the primary growth engine, supported by substantial federal investments in military modernization and the presence of leading test solution providers. Stringent FAA regulations drive continuous demand for advanced testing systems, while the region's focus on innovation in electric and autonomous aviation further accelerates adoption of cutting-edge equipment. Major hubs like Seattle, Wichita, and Los Angeles foster a collaborative ecosystem that integrates testing into the full aircraft lifecycle.

Europe maintains a strong position through its advanced regulatory framework and leadership in sustainable aviation technologies. Countries such as Germany, France, and the United Kingdom host key players like Airbus and Rolls-Royce, which prioritize high-precision test equipment for both commercial and military programs. The region's emphasis on environmental compliance and hydrogen-powered aircraft development creates unique testing requirements that spur specialized solution development. Collaborative projects under the European Union’s Clean Aviation initiative further enhance regional capabilities in structural and propulsion system validation.

Asia Pacific is emerging as the fastest-growing region, fueled by rapid fleet expansion in China, India, and Southeast Asia. China dominates within the region through massive investments in domestic aircraft programs and military modernization, creating significant demand for localized test equipment manufacturing. India’s growing civil aviation sector and defense indigenization efforts are also contributing to market momentum. Government-backed infrastructure projects and the rise of low-cost carriers are prompting airlines to upgrade MRO facilities with state-of-the-art testing solutions.

Latin America exhibits steady growth, primarily driven by Brazil’s Embraer and the region’s expanding commercial aviation network. Mexico and Chile are becoming important MRO destinations, attracting investment in test equipment to support regional aircraft maintenance. The market benefits from increasing air connectivity and tourism, though economic volatility occasionally tempers capital spending on advanced systems.

The Middle East and Africa are witnessing accelerated development, led by the United Arab Emirates and Saudi Arabia’s ambitious aviation hubs. These nations are investing heavily in world-class MRO centers equipped with the latest test technologies to service both commercial and military fleets. Israel’s defense sector continues to drive innovation in specialized test solutions, while South Africa serves as a key hub for African aviation maintenance activities.

Competitive Analysis

The global Aviation Test Equipment market is dominated by players:

- Honeywell International Inc.

- The Boeing Company

- Airbus SE

- Rolls-Royce Holdings plc

- General Electric Company

- Teradyne Inc.

- Collins Aerospace (RTX Corporation)

- SPHEREA Test & Services

- Moog Inc.

- Avtron Aerospace Inc.

The global Aviation Test Equipment market is segmented as follows:

By Equipment Type

- Electrical Aviation Test Equipment

- Hydraulic Aviation Test Equipment

- Pneumatic Aviation Test Equipment

- Avionics Test Equipment

- Others

By Application

- Commercial Aviation

- Military Aviation

By End-User

- Original Equipment Manufacturers

- Maintenance Repair and Overhaul

- Airlines and Operators

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Aviation Test Equipment market is dominated by players:

- Honeywell International Inc.

- The Boeing Company

- Airbus SE

- Rolls-Royce Holdings plc

- General Electric Company

- Teradyne Inc.

- Collins Aerospace (RTX Corporation)

- SPHEREA Test & Services

- Moog Inc.

- Avtron Aerospace Inc.

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors