![]()

Search Market Research Report

Aircraft Turbine Engine Flowmeter And Pressure Sensors Market Size, Share Global Analysis Report, 2026-2034

Aircraft Turbine Engine Flowmeter And Pressure Sensors Market Size, Share, Growth Analysis Report By Type (Turboshaft Engine, Turboprop Engine, Turbofan Engine, and Others), By Application (Helicopter, Business Jet Engine, Wide-Body Aircraft Engine, Narrow-Body Aircraft Engine, Military Engine, Regional Jet Engine, and Others), By Component (Hardware, Software, Services), By Technology (Analog, Digital), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

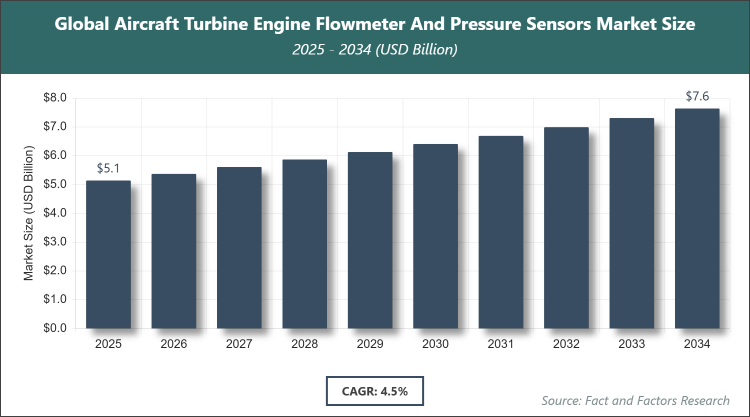

[222+ Pages Report] According to Facts & Factors, the global Aircraft Turbine Engine Flowmeter and Pressure Sensors market size was estimated at USD 5.14 billion in 2025 and is expected to reach USD 7.87 billion by the end of 2034. The Aircraft Turbine Engine Flowmeter and Pressure Sensors industry is anticipated to grow by a CAGR of 4.5% between 2026 and 2034. The Aircraft Turbine Engine Flowmeter and Pressure Sensors Market is driven by increasing investments in advanced aircraft turbine engines for enhanced fuel efficiency and performance in commercial and military sectors.

Market Overview

Market Overview

The aircraft turbine engine flowmeter and pressure sensors market involves the development, manufacturing, and integration of specialized devices that monitor fuel flow rates and pressure levels within turbine engines, ensuring optimal performance, safety, and efficiency in aviation applications. These sensors provide real-time data critical for engine management systems, helping to prevent failures, optimize combustion, and comply with stringent aviation regulations. The market encompasses technologies that withstand extreme conditions like high temperatures and vibrations, serving both commercial and military aircraft, where precision measurement is essential for operational reliability and fuel economy.

Key Insights

- As per the analysis shared by our research analyst, the global Aircraft Turbine Engine Flowmeter and Pressure Sensors market is estimated to grow annually at a CAGR of around 4.5% over the forecast period (2026-2034).

- In terms of revenue, the global Aircraft Turbine Engine Flowmeter and Pressure Sensors market size was valued at around USD 5.14 billion in 2025 and is projected to reach USD 7.87 billion by 2034.

- The Aircraft Turbine Engine Flowmeter and Pressure Sensors market is projected to witness significant growth due to rising demand for fuel-efficient aircraft and advancements in sensor technologies.

- Based on the Type, the Turboshaft Engine segment accounted for the largest market share of 42% due to its widespread use in helicopters and military applications requiring high reliability.

- Based on the Application, the Helicopter segment accounted for the largest market share of 28% due to increasing demand for rotary-wing aircraft in defense and emergency services.

- Based on the Component, the Hardware segment accounted for the largest market share of 55% due to the essential role of physical sensors in engine monitoring.

- Based on the Technology, the Digital segment accounted for the largest market share of 62% due to its superior accuracy and integration with modern avionics systems.

- Based on the region, the North America region captured around 38% market share, driven by the presence of major aerospace manufacturers and high defense spending.

Growth Drivers

- Increasing Investments in Advanced Aircraft Engines

Governments and private sectors are channeling substantial funds into developing next-generation turbine engines that prioritize fuel efficiency, reduced emissions, and enhanced performance, directly boosting the demand for sophisticated flowmeters and pressure sensors. These investments are spurred by global aviation growth and the need for sustainable technologies, such as hybrid-electric propulsion systems, where precise sensor data is vital for optimization. Innovations like MEMS-based sensors further enable lighter, more accurate monitoring, supporting the transition to greener aviation practices.

Additionally, collaborations between engine manufacturers and sensor providers accelerate product development, ensuring compatibility with evolving engine designs. This dynamic fosters market expansion by addressing regulatory pressures for lower carbon footprints and improving overall aircraft reliability, ultimately driving adoption across commercial, military, and business aviation segments.

Restraints

- High Manufacturing and Development Costs

The capital-intensive nature of producing aviation-grade sensors, which must meet rigorous quality and performance standards, acts as a barrier to entry for new players and increases overall market costs. Strict certification processes from bodies like the FAA and EASA add to development expenses, potentially delaying product launches and limiting scalability. Volatility in raw material prices, such as specialized alloys, further exacerbates financial pressures.

Moreover, the need for extensive testing in extreme environments strains resources, particularly for smaller firms. These factors can slow innovation and market growth, especially in emerging regions with limited funding, necessitating cost-sharing strategies and technological efficiencies to alleviate constraints.

Opportunities

- Advancements in Digital and AI-Integrated Sensors

The integration of AI and machine learning into sensor systems offers predictive maintenance capabilities, enabling real-time data analysis for fault detection and efficiency gains. This trend aligns with the industry's shift toward smart aviation, creating opportunities for sensor upgrades in existing fleets. Research into miniaturized, wireless sensors enhances installation flexibility and reduces weight, appealing to next-gen aircraft designs.

Furthermore, partnerships in R&D can lead to breakthrough products, such as customizable pressure sensors for specific engine types. This opportunity not only expands application scopes but also supports sustainability goals, positioning the market for growth in retrofit programs and new aircraft programs.

Challenges

- Volatility in the Aircraft Industry

Fluctuations in global aviation demand, influenced by economic downturns, geopolitical tensions, and airline bankruptcies, pose risks to sensor suppliers dependent on steady orders. Changing trade policies and supply chain disruptions can delay projects and increase costs. Additionally, the slow recovery in some regions post-pandemic affects fleet expansions.

In addition, adapting to rapidly evolving regulations on emissions and safety requires continuous innovation, straining operational capacities. These challenges demand agile supply chains and diversified portfolios to maintain stability and capitalize on recovery trends.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 5.14 Billion |

Projected Market Size in 2034 |

USD 7.87 Billion |

CAGR Growth Rate |

4.5% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Honeywell International Inc., Rockwell Collins, United Technologies Corporation, Ametek Inc., General Electric Company, Endress+Hauser Group, Siemens AG, BAE Systems plc, Meggitt PLC, Lord Corporation, Teledyne Technologies Incorporated, TDK Corporation, and Others. |

Key Segment |

By Type, By Application, By Component, By Technology, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Aircraft Turbine Engine Flowmeter And Pressure Sensors market is segmented by type, application, component, technology, and region.

Based on Type Segment, The Aircraft Turbine Engine Flowmeter And Pressure Sensors market is divided into Turboshaft Engine, Turboprop Engine, Turbofan Engine, and others. The most dominant segment is Turboshaft Engine, which holds the largest share due to its critical application in helicopters and military vehicles where reliable torque measurement is essential, driving the market by enhancing operational safety and efficiency in demanding environments; the second most dominant is Turbofan Engine, favored for commercial aviation's fuel-efficient designs, contributing to market growth through widespread adoption in narrow-body and wide-body aircraft for optimized performance.

Based on Application Segment, The Aircraft Turbine Engine Flowmeter And Pressure Sensors market is divided into Helicopter, Business Jet Engine, Wide-Body Aircraft Engine, Narrow-Body Aircraft Engine, Military Engine, Regional Jet Engine, and others. The most dominant segment is Helicopter, commanding the highest share because of rising demand in defense, search and rescue, and medical evacuation operations requiring precise engine monitoring, which drives the market by supporting global security and emergency response initiatives; the second most dominant is Wide-Body Aircraft Engine, utilized in long-haul commercial flights for better fuel management, propelling market expansion amid increasing international travel.

Based on Component Segment, The Aircraft Turbine Engine Flowmeter And Pressure Sensors market is divided into Hardware, Software, Services. The most dominant segment is Hardware, holding the biggest share due to the foundational need for physical sensors in engine systems, driving the market by ensuring accurate data collection for safety compliance; the second most dominant is Services, encompassing maintenance and calibration, contributing to market growth through aftermarket support and lifecycle management.

Based on Technology Segment, The Aircraft Turbine Engine Flowmeter And Pressure Sensors market is divided into Analog, Digital. The most dominant segment is Digital, with the largest share attributed to its advanced data processing and integration with digital cockpits, driving the market by enabling predictive analytics and reduced downtime; the second most dominant is Analog, still relevant in legacy systems, helping sustain market stability during transitions.

Recent Developments

- In September 2023, Rolls-Royce successfully conducted a fuel burn run for its hybrid-electric engine, advancing sensor integration for hybrid propulsion systems.

- In June 2023, General Electric announced manufacturing jet engines for Indian Military aircraft, incorporating advanced flowmeters and pressure sensors.

- In June 2023, Baker Hughes launched the Druck NG3000 Pressure Sensors, offering customizable features for aerospace applications.

- In June 2021, GE and Safran formed a joint venture for sustainable aviation solutions, focusing on sensor technologies for reduced emissions.

- In February 2023, Lockheed Martin explored partnerships in emerging markets like India, emphasizing sensor advancements for local production.

Regional Analysis

- North America to dominate the global market

North America commands the aircraft turbine engine flowmeter and pressure sensors market, with the United States as the dominant country owing to its robust aerospace industry featuring leaders like Lockheed Martin and substantial investments in military and commercial aviation technologies. The region's emphasis on innovation through agencies such as NASA and the Department of Defense drives sensor advancements for superior engine performance. High defense budgets facilitate extensive R&D in digital sensors, while a mature supply chain ensures efficient production. The U.S. benefits from strategic exports and partnerships, solidifying its lead in global aviation standards.

Europe exhibits strong growth through collaborative aerospace projects and a focus on sustainable technologies, led by France as the dominant country with companies like Safran pioneering engine sensor integrations. The region's commitment to emission reductions under EU policies promotes AI-enhanced sensors for fuel optimization. Cross-border initiatives like Airbus foster technological exchanges, enhancing sensor reliability. France's dominance arises from its export-oriented industry and investments in hybrid engines, supporting market resilience.

Asia Pacific accelerates with expanding aviation infrastructure and military modernizations, dominated by China through rapid domestic production and investments in indigenous sensor technologies. The region's booming air travel demand spurs sensor adoption in new fleets, while government policies emphasize self-reliance in aerospace. China's lead stems from state-backed R&D and partnerships, enabling cost-effective solutions for regional growth.

Latin America progresses with increasing regional jet demands and defense upgrades, led by Brazil via Embraer and local sensor manufacturing initiatives. Infrastructure developments in aviation hubs drive sensor integration for efficiency. Brazil's position strengthens from export focus and collaborations, aiding market penetration.

The Middle East & Africa advances through oil-funded aviation expansions and security needs, with Saudi Arabia dominating via Vision 2030's aerospace localization efforts. Investments in military aircraft enhance sensor demand for performance monitoring. Saudi Arabia's leadership comes from strategic alliances and diversification, fostering industry growth.

Competitive Analysis

The global Aircraft Turbine Engine Flowmeter And Pressure Sensors market is dominated by players:

- Honeywell International Inc.

- Rockwell Collins

- United Technologies Corporation

- Ametek Inc.

- General Electric Company

- Endress+Hauser Group

- Siemens AG

- BAE Systems plc

- Meggitt PLC

- Lord Corporation

- Teledyne Technologies Incorporated

- TDK Corporation

The global Aircraft Turbine Engine Flowmeter And Pressure Sensors market is segmented as follows:

By Type

- Turboshaft Engine

- Turboprop Engine

- Turbofan Engine

- Others

By Application

- Helicopter

- Business Jet Engine

- Wide-Body Aircraft Engine

- Narrow-Body Aircraft Engine

- Military Engine

- Regional Jet Engine

- Others

By Component

- Hardware

- Software

- Services

By Technology

- Analog

- Digital

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Honeywell International Inc.

- Rockwell Collins

- United Technologies Corporation

- Ametek Inc.

- General Electric Company

- Endress+Hauser Group

- Siemens AG

- BAE Systems plc

- Meggitt PLC

- Lord Corporation

- Teledyne Technologies Incorporated

- TDK Corporation

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors