![]()

Search Market Research Report

Additive Manufacturing Market Size, Share Global Analysis Report, 2022 – 2028

Additive Manufacturing Market Size, Share, Growth Analysis Report By Component (Hardware, Software, Services), By Printer Type (Desktop 3D Printer, Industrial 3D Printer), By Technology (Stereolithography, Fuse Deposition Modeling, Selective Laser Sintering, Direct Metal Laser Sintering, Polyjet Printing, Inkjet Printing, Electron Beam Melting, Laser Metal Deposition, Digital Light Processing, Laminated Object Manufacturing, Others), By Software (Design Software, Inspection Software, Printer Software, Scanning Software), By Application (Prototyping, Tooling, Functional Parts), and By Region - Global and Regional Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2022 – 2028

Industry Insights

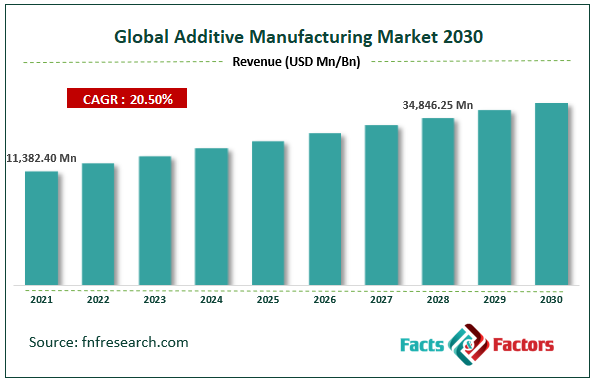

[235+ Pages Report] According to Facts and Factors, the global additive manufacturing market size was worth USD 11,382.40 million in 2021 and is estimated to grow to USD 34,846.25 million by 2028, with a compound annual growth rate (CAGR) of approximately 20.50% over the forecast period. The report analyzes the additive manufacturing market's drivers, restraints/challenges, and their effect on the demands during the projection period. In addition, the report explores emerging opportunities in the additive manufacturing market.

Market Overview

Market Overview

Producing products from a collection of 3D models using additive materials is known as additive manufacturing. This stands for all additive processes, frameworks, tools, and applications. The market for additive manufacturing includes, among other things, 3D printers, service providers, and printing supplies. Quick manufacturing and rapid prototyping are two common market applications. The evolution of the technologies and materials utilized in the industry is projected to impact the worldwide market for additive manufacturing. Several corporations, research institutions, and governmental authorities are introducing new technologies to the global additive manufacturing market. Technological advancements aid in increasing capacity overall. Titanium, aluminum, and stainless steel are the three main metals utilized in the global market for additive manufacturing. Increased interest in lightweight materials is anticipated to have a beneficial effect on the global market. The production of unique items is made simple by new and better technologies, which drive the global additive manufacturing market. The simplicity of creating customized items and government funding for additive manufacturing are two of the main factors driving this sector.

Additionally, quick and inexpensive product creation is the main driver of increased demand for additive manufacturing. The global market is expected to be constrained by several limitations despite the potential economic benefits of additive manufacturing. For instance, additive manufacturing is costly and cumbersome compared to the standard method of producing items. It is therefore unlikely to replace the primary process entirely.

Covid-19 Impact:

The COVID-19 epidemic is hampering the desire for additive manufacturing in several applications. Governments have implemented lockdown measures in many different nations worldwide to stop the spread of the disease. As a result, supply and transportation constraints, a delay in infrastructure development, and a slowdown in manufacturing operations have all occurred. As a result, additive manufacturing is becoming less popular worldwide. Tier I and tier II manufacturers and suppliers are the main participants in the market for additive manufacturing. These firms' manufacturing and supply chain facilities are dispersed throughout several nations in Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

Key Insights

- As per the analysis shared by our research analyst, the global additive manufacturing market value is expected to grow at a CAGR of 20.50% over the forecast period.

- In terms of revenue, the global additive manufacturing market size was valued at around USD 11,382.40 million in 2021 and is projected to reach USD 34846.25 million by 2028.

- A few key factors anticipated to contribute to the market revenue growth include the simplicity of manufacturing complex designs, developing new, improved technologies and materials, increased government funding to support additive manufacturing, and relatively low production costs for rapid manufacturing.

- By component segment, the hardware category dominated the market in 2021.

- By printer type, the industrial 3D printer category dominated the market in 2021.

- North America dominated the global additive manufacturing market in 2021.

Growth Driver

- Comparatively less expensive manufacturing for quick manufacturing drives the market growth

Due to significantly reduced production costs compared to traditional manufacturing techniques, additive technologies in production can be cost-effective. Fixed costs in traditional manufacturing methods are exclusively allotted to a particular component design. For instance, a die may only be used in die casting to create a particular product for which it was designed. Therefore, the mold cost must be justified by the volume of components produced. The number of pieces produced in the manufacturing batch up to the next must be divided by the price of setting up a machine tool or changing tools on an injection molding machine. Therefore, if only a few pieces or small series are manufactured every batch, the fixed cost may surpass the variable cost. While certain fixed costs are associated with additive manufacturing, these can be more easily compensated by the variety of items created in a single batch. Due to this, additive production is more affordable than production using traditional manufacturing procedures, which is one of the key reasons influencing the growth of the market's revenue.

Restraints

- Software efficiency issues may hinder the market growth

The majority of customer-specific additive manufacturing is done manually, and in some early use cases of additive manufacturing, this manual labor is somewhat justified (AM). It was not essential to tightly integrate the 3D printer with supporting software solutions for the prototype because only a small number of components were generated, and there was not much of a requirement for substantial data collecting. However, as mass manufacturing becomes more prevalent in applications, it is crucial to integrate systems to drive costs for things like human labor. Although some suppliers are beginning to offer 3D printer APIs, they are still mainly unstandardized and underutilized, making integration difficult and expensive.

Segmentation Analysis

The global additive manufacturing market is segregated based on component, printer type, technology, software, and application.

The market is classified into hardware, software, and services based on components. In 2021, the hardware sector dominated the market. The hardware sector dominated the market because of the ongoing emphasis that manufacturing companies placed on developing improved production techniques and quick prototyping. Due to several factors, including rapid industrialization, the rising demand for consumer electronics products, the ongoing development of civil infrastructure, rapid urbanization, and reduced labor costs, the hardware segment is expected to experience significant growth throughout the forecast period.

Based on printer type, the market is classified into desktop 3D printers and industrial 3D printers. In 2021, the industrial 3D printer market had a monopoly. For some popular applications, such as prototyping, designing, and tooling, industrial 3D printers are widely embraced across various sectors and industry verticals, including automotive, electronics, aerospace & military, and healthcare. The industrial 3D printer market segment is anticipated to continue leading the market throughout the projected period due to the widespread usage of additive manufacturing for prototyping, designing, and tooling.

Based on technology, the market is segmented into stereolithography, fuse deposition modeling, selective laser sintering, direct metal laser sintering, polyjet printing, inkjet printing, electron beam melting, laser metal deposition, and digital light processing, laminated object manufacturing, and others. In 2021, the market was dominated by the stereolithography category. One of the earliest and most widely used printing techniques is stereolithography. In addition to its simplicity of use, stereolithography has several other benefits promoting its uptake. However, technological advancements and the intensive R&D initiatives undertaken by researchers and industry professionals create prospects for several additional effective and dependable solutions.

Based on software, the market is classified into the design, inspection, printer, and scanning software. In 2021, the market was dominated by design software. Throughout the projection period, the category is anticipated to maintain its market dominance. Particularly in the automotive, aerospace & military, and construction & engineering industries, design software is used to create the designs of the objects to be printed. The use of design software has several benefits. One benefit is that design software may act as a conduit between the target item and the printer's hardware.

The application market is segmented into prototyping, tooling, and functional parts. The prototyping segment dominates the market in 2021. In 2021, the prototyping sector dominated the market. The prototype technique is widely employed in various business sectors and industries. Prototyping is a common technique used by automotive, aerospace, and military companies to manufacture exact parts, components, and intricate systems. Manufacturers may build trustworthy final goods and attain improved precision through prototyping. As a result, it is anticipated that the prototyping segment will continue to rule the market over the projection period.

Recent Development:

- November 2021: The Danish shoe manufacturer ECCO is using Stratasys Origin one 3D printing technology to speed up product development by enabling conceptual footwear samples to be evaluated early in the development cycle using the 3D printed mold and lasts made of resin materials from Henkel Loctite, according to Stratasys Ltd., a leader in polymer 3D printing solutions.

Report Scope

Report Attribute |

Details |

Market Size in 2021 |

USD 11,382.40 Million |

Projected Market Size in 2028 |

USD 34,846.25 Million |

CAGR Growth Rate |

20.50% CAGR |

Base Year |

2021 |

Forecast Years |

2022-2028 |

Key Market Players |

Stratasys Ltd., Materialise NV, EnvisionTec Inc., 3D Systems Inc., GE Additive, Autodesk Inc., Made In Space, Canon Inc., Voxeljet AG, Optomec Inc., and Others |

Key Segment |

By Component, Printer Type, Technology, Software, Application, and Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Regional Landscape

- North America dominates the additive manufacturing market in 2021

The market for additive manufacturing in North America accounted for the largest revenue share in 2021. This is because there are significant market players in the region, which has encouraged the development of the technology and increased the number of patents. Additionally, it is predicted that technological advancements, the effective utilization of R&D resources, and cutting-edge methodologies like artificial intelligence and machine learning in every industry would support market progress throughout the projected time. Governments in the region are anticipated to support the widespread adoption of additive manufacturing technology to develop modern infrastructure, foster sustainable growth, and bring down input costs. North American market revenue growth is anticipated to be fueled by this.

Competitive Landscape

- Stratasys Ltd.

- Materialise NV

- EnvisionTec Inc.

- 3D Systems Inc.

- GE Additive

- Autodesk Inc.

- Made In Space

- Canon Inc.

- Voxeljet AG

- Optomec Inc

Global Additive Manufacturing Market is segmented as follows:

By Component

- Hardware

- Software

- Services

By Printer Type

- Desktop 3D Printer

- Industrial 3D Printer

By Technology

- Stereolithography

- Fused Deposition Modeling

- Selective Laser Sintering

- Direct Metal Laser Sintering

- Polyjet Printing

- Inkjet Printing

- Electron Beam Melting

- Laser Metal Deposition

- Digital Light Processing

- Laminated Object Manufacturing

- Others

By Software

- Design Software

- Inspection Software

- Printer Software

- Scanning Software

By Application

- Prototyping

- Tooling

- Functional Parts

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Nordic Countries

- Denmark

- Sweden

- Norway

- Benelux Union

- Belgium

- The Netherlands

- Luxembourg

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Southeast Asia

- Indonesia

- Thailand

- Malaysia

- Singapore

- Rest of Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Stratasys Ltd.

- Materialise NV

- EnvisionTec Inc.

- 3D Systems Inc.

- GE Additive

- Autodesk Inc.

- Made In Space

- Canon Inc.

- Voxeljet AG

- Optomec Inc

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors