![]()

Search Market Research Report

Gasoline Direct Injection (GDI) System Market Size, Share Global Analysis Report, 2026-2034

Gasoline Direct Injection (GDI) System Market Size, Share, Growth Analysis Report By Component (Fuel Injectors, Fuel Pumps, Sensors, Electronic Control Units, and Others), By Engine Type (4 Cylinder, 6 Cylinder, 8 Cylinder, and Others), By Vehicle Type (Passenger Cars and Commercial Vehicles), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

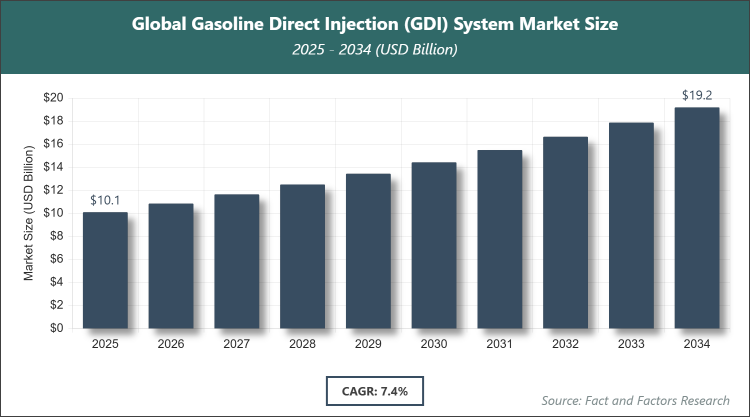

[225+ Pages Report] According to Facts & Factors, the global Gasoline Direct Injection (GDI) System market size was estimated at USD 10.1 billion in 2025 and is expected to reach USD 19.2 billion by the end of 2034. The Gasoline Direct Injection (GDI) System industry is anticipated to grow by a CAGR of 7.4% between 2026 and 2034. The Gasoline Direct Injection (GDI) System Market is driven by increasing adoption of advanced fuel injection technologies to meet emission standards and improve vehicle performance.

Market Overview

Market Overview

The Gasoline Direct Injection (GDI) System market encompasses technologies designed to inject gasoline directly into the combustion chamber of an engine, enhancing fuel efficiency, power output, and emission control compared to traditional port fuel injection systems. This market involves components and systems that enable precise fuel delivery under high pressure, catering primarily to the automotive sector where engine performance and environmental compliance are critical. GDI systems are integral to modern internal combustion engines, supporting downsizing trends and turbocharging to achieve better mileage without sacrificing power.

Key Insights

- As per the analysis shared by our research analyst, the Gasoline Direct Injection (GDI) System market is estimated to grow annually at a CAGR of around 7.4% over the forecast period (2026-2034).

- In terms of revenue, the Gasoline Direct Injection (GDI) System market size was valued at around USD 10.1 billion in 2025 and is projected to reach USD 19.2 billion by 2034.

- The Gasoline Direct Injection (GDI) System market is driven by stringent emission regulations and the demand for enhanced fuel efficiency in vehicles.

- Based on the Component, the Fuel Injectors segment dominated the market in 2025, with a market share of 35% as it plays a pivotal role in precise fuel delivery, enabling better combustion efficiency and reduced emissions.

- Based on the Engine Type, the 4 Cylinder segment dominated the market in 2025, with a market share of 50% due to its widespread adoption in compact and mid-sized vehicles for optimal balance between performance and fuel economy.

- Based on the Vehicle Type, the Passenger Cars segment dominated the market in 2025, with a market share of 80% owing to rising consumer preference for efficient and high-performance personal vehicles.

- Based on the region, the Asia Pacific region dominated the market in 2025, with a market share of 45% attributed to rapid automotive production growth and supportive government policies on emissions.

Growth Drivers

- Stringent Emission Regulations

Governments worldwide are imposing stricter emission standards to combat environmental pollution, compelling automakers to adopt GDI systems that reduce harmful exhaust gases like NOx and particulates through precise fuel injection. This regulatory push is accelerating the integration of GDI in new vehicle models, particularly in regions with ambitious carbon reduction targets.

The adoption of GDI helps manufacturers comply with norms such as Euro 7 and CAFE standards, fostering innovation in engine design and boosting market demand as legacy systems become obsolete.

- Demand for Fuel-Efficient Vehicles

Rising fuel prices and consumer awareness of sustainability are driving the need for vehicles with superior mileage, where GDI excels by optimizing fuel-air mixtures for efficient combustion. This trend is evident in the shift toward downsized engines that maintain power output while consuming less fuel.

GDI's ability to support turbocharging further enhances efficiency, making it a preferred choice for automakers aiming to meet consumer expectations for cost-effective and eco-friendly transportation options.

- Advancements in Engine Technology

Continuous innovations in high-pressure injectors and electronic controls are improving GDI performance, enabling higher injection pressures for better atomization and reduced engine knock. These advancements are expanding GDI applications to hybrid and performance vehicles.

Collaboration between tech firms and automakers is leading to smarter systems with AI integration, enhancing real-time fuel management and contributing to overall market growth through superior reliability and adaptability.

- Growth in Automotive Production

Expanding automotive manufacturing in emerging economies is increasing the demand for GDI systems as new plants prioritize advanced technologies for competitive edge. This production surge is supported by investments in supply chains and R&D.

As global vehicle output rebounds post-pandemic, GDI adoption is rising to align with export requirements and local market preferences for efficient engines.

Restraints

- High Initial Costs

The elevated expense of GDI components, such as high-pressure pumps and injectors, increases vehicle manufacturing costs, potentially deterring price-sensitive consumers in developing markets. This cost barrier limits widespread adoption in entry-level vehicles.

Maintenance and repair complexities further add to ownership costs, as specialized tools and expertise are required, impacting market penetration in regions with limited service infrastructure.

- Rise of Electric Vehicles

The accelerating shift toward battery electric vehicles (BEVs) reduces reliance on internal combustion engines, posing a threat to GDI demand as governments incentivize EV adoption through subsidies and infrastructure development. This transition is reshaping automotive investments away from traditional systems.

While hybrids may sustain some GDI use, the long-term EV dominance could cap market growth, especially in mature markets prioritizing zero-emission mobility.

- Technical Challenges like Carbon Deposits

GDI systems are prone to carbon buildup on intake valves, leading to performance degradation and higher maintenance needs, which can erode consumer confidence and increase warranty claims for manufacturers.

Addressing these issues requires ongoing R&D into mitigating technologies, but unresolved challenges may slow adoption in high-mileage applications.

Opportunities

- Integration with Hybrid Systems

GDI's compatibility with hybrid electric vehicles (HEVs) offers opportunities to enhance efficiency in combined powertrains, attracting automakers developing transitional technologies toward electrification. This integration supports smoother engine operation and reduced fuel consumption.

As hybrid adoption grows, GDI can evolve to support variable compression and other features, opening new revenue streams in the evolving automotive landscape.

- Emerging Markets in Asia

Rapid urbanization and rising disposable incomes in Asia are boosting vehicle sales, creating opportunities for GDI penetration through localized production and tailored solutions for regional needs. Government incentives for cleaner technologies further amplify this potential.

Partnerships with local suppliers can reduce costs, enabling broader market access and fostering growth in untapped segments.

- Innovations in Injection Technology

Developments in higher-pressure and performance injectors, like 350-bar systems, provide opportunities to improve GDI efficiency and expand applications to commercial and heavy-duty vehicles. These innovations address current limitations and open premium segments.

Collaboration with tech innovators can lead to smarter, adaptive systems, positioning companies for leadership in next-generation engine technologies.

Challenges

- Maintenance Issues

Frequent carbon accumulation in GDI engines necessitates regular cleaning, increasing downtime and costs for owners, which challenges market acceptance in fleet operations where reliability is paramount.

Developing user-friendly maintenance solutions is essential, but current complexities may hinder growth in cost-conscious markets.

- Supply Chain Disruptions

Global supply chain vulnerabilities, exacerbated by geopolitical tensions and material shortages, can delay GDI component availability, affecting production timelines and market stability.

Diversifying suppliers and investing in resilient logistics are critical to mitigate these risks and ensure consistent growth.

- Competition from Alternative Technologies

Advancing port fuel injection hybrids and direct alternatives like diesel systems compete for market share, challenging GDI's dominance in certain applications where cost or simplicity prevails.

Staying ahead requires continuous innovation to differentiate GDI's benefits in efficiency and performance.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 10.1 Billion |

Projected Market Size in 2034 |

USD 19.2 Billion |

CAGR Growth Rate |

7.4% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Robert Bosch GmbH, Denso Corporation, Continental AG, Delphi Technologies, Hitachi Ltd., Marelli Holdings Co., Ltd., Stanadyne LLC, Magneti Marelli, BorgWarner Inc., and Others. |

Key Segment |

By Component, By Engine Type, By Vehicle Type, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Gasoline Direct Injection (GDI) System market is segmented by Component, Engine Type, Vehicle Type, and region.

Based on Component Segment, the Gasoline Direct Injection (GDI) System market is divided into Fuel Injectors, Fuel Pumps, Sensors, Electronic Control Units, and Others. The most dominant segment is Fuel Injectors, followed by Fuel Pumps as the second most dominant. Fuel Injectors dominate due to their critical role in delivering precise fuel amounts directly into the combustion chamber, which significantly improves fuel efficiency, reduces emissions, and enhances engine power; this dominance drives the market by enabling compliance with global emission standards and supporting engine downsizing trends, while Fuel Pumps are second as they provide the necessary high pressure for effective injection, contributing to system reliability and performance in demanding applications.

Based on Engine Type Segment, the Gasoline Direct Injection (GDI) System market is divided into 4 Cylinder, 6 Cylinder, 8 Cylinder, and Others. The most dominant segment is 4 Cylinder, followed by 6 Cylinder as the second most dominant. The 4 Cylinder segment dominates because it offers an optimal balance of fuel economy, compact size, and sufficient power for most passenger vehicles, making it ideal for urban driving and cost-effective manufacturing; this drives market growth by aligning with global trends toward lighter, more efficient engines that reduce overall vehicle weight and emissions, whereas 6 Cylinder is second for its use in mid-to-premium vehicles requiring higher performance without excessive fuel consumption.

Based on Vehicle Type Segment, the Gasoline Direct Injection (GDI) System market is divided into Passenger Cars and Commercial Vehicles. The most dominant segment is Passenger Cars, followed by Commercial Vehicles as the second most dominant. Passenger Cars dominate owing to high consumer demand for personal mobility solutions with advanced features like better mileage and lower emissions, which GDI systems provide effectively; this segment propels the market through volume sales and rapid technology adoption in sedans and SUVs, while Commercial Vehicles are second as they benefit from GDI's durability and efficiency in logistics and transport, helping to lower operational costs over long hauls.

Recent Developments

- In December 2023, Stanadyne expanded its performance and specialty product portfolio with the launch of its patented Goliath 350-bar gasoline direct injection (GDI) performance fuel injector, aimed at enhancing fuel efficiency and power in high-performance engines.

- In January 2024, Standard Motor Products, Inc. launched a new GDI Fuel Injection Program, introducing advanced units designed to improve reliability and compatibility across various vehicle models.

- In November 2024, Marelli announced the launch of a new AI-based Electronic Control Unit for engine and vehicle control, supporting GDI systems in motorsport and hybrid applications to optimize performance and emissions.

- In June 2023, IAV GmbH partnered with Sonplas GmbH to develop and sell measurement devices for validating and optimizing injection systems, including GDI for alternative and traditional fuels.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region leads the Gasoline Direct Injection (GDI) System market due to booming automotive manufacturing and urbanization, with China as the dominating country owing to its massive vehicle production capacity and government mandates for cleaner engines. Rapid economic growth fuels demand for efficient vehicles, supported by investments in R&D and supply chains. Local automakers prioritize GDI for export compliance, while consumer preferences shift toward fuel-saving technologies amid rising fuel costs. Infrastructure developments and partnerships with global players further strengthen the region's position in advanced engine systems.

North America exhibits strong growth in the GDI market, with the United States dominating through its focus on innovation and regulatory compliance for emissions. Automakers integrate GDI in trucks and SUVs to meet CAFE standards, driven by consumer demand for powerful yet efficient vehicles. Technological advancements from key players enhance system adoption, while collaborations with tech firms boost hybrid applications. The region's robust aftermarket supports maintenance, ensuring sustained demand amid evolving mobility trends.

Europe maintains a prominent share in the GDI market, led by Germany as the dominating country with its engineering prowess and stringent Euro emission norms. The emphasis on sustainable mobility encourages GDI use in premium and compact cars, supported by EU incentives for low-emission technologies. Automotive giants invest in R&D for advanced injectors, while consumer awareness of environmental impacts drives adoption. Cross-border collaborations and a mature supply chain facilitate market expansion.

Latin America shows emerging potential in the GDI market, with Brazil dominating through increasing vehicle imports and local assembly of efficient models. Economic recovery boosts automotive sales, with GDI aiding compliance to regional emission rules. Growing middle-class demand for fuel-efficient cars, coupled with foreign investments, accelerates adoption. Challenges like infrastructure gaps are offset by government policies promoting cleaner fuels and technologies.

The Middle East & Africa region experiences gradual GDI growth, dominated by South Africa with its automotive export focus and adoption of global standards. Oil-rich economies prioritize efficiency to diversify from fuel dependency, while urban expansion increases vehicle demand. Partnerships with international firms introduce advanced systems, though high temperatures pose technical challenges. Regulatory harmonization with global norms supports future expansion.

Competitive Analysis

The global Gasoline Direct Injection (GDI) System market is dominated by players:

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Delphi Technologies

- Hitachi Ltd.

- Marelli Holdings Co., Ltd.

- Stanadyne LLC

- Magneti Marelli

- BorgWarner Inc.

- Others

The global Gasoline Direct Injection (GDI) System market is segmented as follows:

By Component

- Fuel Injectors

- Fuel Pumps

- Sensors

- Electronic Control Units

- Others

By Engine Type

- 4 Cylinder

- 6 Cylinder

- 8 Cylinder

- Others

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Gasoline Direct Injection (GDI) System market is dominated by players:

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Delphi Technologies

- Hitachi Ltd.

- Marelli Holdings Co., Ltd.

- Stanadyne LLC

- Magneti Marelli

- BorgWarner Inc.

- Others

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors