![]()

Search Market Research Report

Dry Mortar Market Size, Share Global Analysis Report, 2026-2034

Dry Mortar Market Size, Share, Growth Analysis Report By Type (Thin Bed Mortar, Tile Adhesive Mortar, Repair Mortar, Masonry Mortar, Waterproofing Mortar, and Others), By Application (Plastering, Tiling, Flooring, Insulation Systems, and Others), By End-User (Residential, Commercial, Industrial, Infrastructure), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

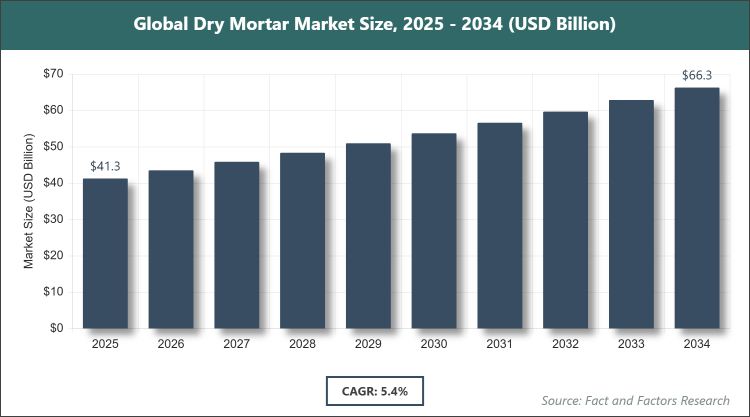

[225 Pages Report] According to Facts & Factors, the global Dry Mortar market size was estimated at USD 41.30 billion in 2025 and is expected to reach USD 68.91 billion by the end of 2034. The Dry Mortar industry is anticipated to grow by a CAGR of 5.4% between 2026 and 2034. The Dry Mortar Market is driven by rapid growth in the construction industry and increasing demand for ready-mix, high-performance building materials.

Market Overview

Market Overview

Dry mortar refers to a pre-blended mixture of cement, sand, and various additives designed for use in construction activities such as bonding bricks, plastering walls, and applying finishes. This material is produced in controlled factory environments to ensure uniformity and quality, making it a preferred choice over traditional on-site mixing methods that can vary in composition and performance. It is versatile, applicable in both interior and exterior settings, and enhances construction efficiency by reducing waste and labor time while providing superior adhesion and durability to structures.

Key Insights

- As per the analysis shared by our research analyst, the global Dry Mortar market is estimated to grow annually at a CAGR of around 5.4% over the forecast period (2026-2034).

- In terms of revenue, the global Dry Mortar market size was valued at around USD 41.30 Billion in 2025 and is projected to reach USD 68.91 Billion, by 2034.

- The Dry Mortar market is driven by growth in the construction industry and demand for ready-mix, high-performance building materials.

- Based on the Type, the Thin Bed Mortar segment dominated the market in 2025 with a revenue share of 28%.

- The dominance is attributed to its efficiency in modern construction techniques requiring thin layers for better adhesion and reduced material usage.

- Based on the Application, the Plastering segment dominated the market in 2025 with a revenue share of 33%.

- The dominance is attributed to its widespread use in structural and finishing layers across residential and commercial projects for smooth surfaces and durability.

- Based on the End-User, the Residential segment dominated the market in 2025 with a revenue share of 56%.

- The dominance is attributed to increasing urban household formation, renovations, and the need for consistent quality in home building.

- Asia Pacific dominated the global market with a share of 47% in 2025 due to rapid urbanization and massive infrastructure projects in countries like China and India.

Market Dynamics

Growth Drivers

- Rising Infrastructure Development Projects

The surge in global infrastructure initiatives, including roads, railways, airports, and commercial facilities, significantly boosts the demand for dry mortar due to its reliability and quick application properties. Governments worldwide are investing heavily in such projects to support economic growth and urbanization, creating a steady need for high-quality construction materials that ensure long-lasting structures. This driver is particularly evident in emerging economies where modernization efforts are accelerating, leading to expanded use of dry mortar in large-scale developments.

Furthermore, advancements in construction technologies complement this growth by enabling faster project completion times, where dry mortar's pre-mixed nature reduces on-site preparation and minimizes errors. As a result, contractors prefer it for its consistency, which helps meet stringent project deadlines and quality standards, ultimately contributing to cost savings and enhanced safety in infrastructure builds.

- Increasing Demand in the Hospitality Sector

The revival of global tourism post-pandemic has spurred investments in hotels, restaurants, and leisure facilities, driving the adoption of dry mortar for its aesthetic and functional benefits in interior and exterior applications. This sector requires materials that offer durability against high foot traffic and environmental factors, making dry mortar an ideal choice for efficient and visually appealing constructions.

In addition, the focus on sustainable and energy-efficient building practices in hospitality projects further amplifies this driver, as dry mortar formulations can incorporate eco-friendly additives. This alignment with green building trends not only meets regulatory requirements but also appeals to environmentally conscious consumers, fostering broader market penetration.

Restraints

- Health Concerns Related to Inhalation and Exposure

Prolonged exposure to dry mortar dust can cause respiratory issues, skin irritation, and other health problems, limiting its adoption in regions with strict occupational safety regulations. Workers often face risks during handling and mixing, prompting the need for protective equipment and better ventilation, which increases operational costs for construction firms.

Moreover, public awareness of these health risks has led to hesitancy among smaller contractors, potentially slowing market growth in less-regulated areas. Efforts to mitigate this through improved product formulations and safety guidelines are ongoing, but the restraint persists as a barrier to widespread acceptance.

- Volatile Raw Material Prices

Fluctuations in the costs of key ingredients like cement and additives disrupt supply chains and profit margins, making it challenging for manufacturers to maintain competitive pricing. This volatility is often influenced by global economic factors, energy prices, and geopolitical events, leading to unpredictable budgeting for end-users.

Additionally, such price instability can delay projects and encourage shifts to alternative materials, hindering overall market expansion. Strategies like long-term supplier contracts and diversification of sources are being employed to address this, yet it remains a significant restraint.

Opportunities

- Strategic Partnerships and New Product Launches

Collaborations between manufacturers and suppliers are fostering innovation in safer, more efficient dry mortar solutions, such as water-soluble packaging, opening new avenues for market growth. These partnerships enable the development of customized products tailored to specific applications, enhancing user convenience and reducing environmental impact.

Beyond that, the introduction of novel formulations for residential and commercial use expands accessibility, attracting a broader customer base. This opportunity is amplified by rising consumer preferences for sustainable materials, positioning companies to capture emerging segments through targeted R&D investments.

- Growth in Tile-Based Construction Projects

The increasing popularity of tiles in emerging markets due to their cost-effectiveness and aesthetic appeal creates demand for specialized dry mortars like tile adhesives. Urbanization drives this trend, with tiles being favored for flooring and walls in modern buildings for their durability and ease of maintenance.

Furthermore, this opportunity is supported by infrastructure policies promoting efficient building practices, allowing for greater integration of dry mortar in tile installations. As a result, manufacturers can capitalize on this by expanding production capacities in high-growth regions.

Challenges

- Quality Management and Lack of Standardization

Variations in product quality across brands due to inconsistent global standards lead to reliability issues and customer dissatisfaction, challenging market trust. Without uniform regulations, manufacturers struggle to ensure consistent performance, which can result in project failures and increased scrutiny.

In addition, this challenge is compounded by regional differences in raw material availability, affecting formulation consistency. Addressing it requires industry-wide initiatives for standardization, but progress is slow, impacting overall adoption rates.

- Environmental Concerns and Emission Regulations

The production and use of dry mortar contribute to greenhouse gas emissions, facing pushback from stringent environmental policies aimed at reducing carbon footprints. This pressures manufacturers to adopt cleaner processes, which can be costly and technologically demanding.

Moreover, growing emphasis on sustainable construction practices demands low-emission alternatives, posing a hurdle for traditional formulations. Navigating these regulations while maintaining affordability remains a key challenge for sustained market growth.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 41.30 Billion |

Projected Market Size in 2034 |

USD 68.91 Billion |

CAGR Growth Rate |

5.4% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Sika AG, Saint-Gobain Weber, Ardex Group, CEMEX S.A.B. de C.V., LafargeHolcim, Mapei SpA, BASF SE, Knauf, Dow, Parex Group, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Dry Mortar market is segmented by type, application, end-user, and region.

Based on Type Segment, the Dry Mortar market is divided into Thin Bed Mortar, Tile Adhesive Mortar, Repair Mortar, Masonry Mortar, Waterproofing Mortar, and others.

The most dominant segment is Thin Bed Mortar, while the second most dominant is Tile Adhesive Mortar. Thin Bed Mortar leads due to its suitability for precise, thin-layer applications in modern construction, offering reduced material consumption, faster setting times, and improved thermal efficiency, which drives market growth by enabling cost-effective and energy-saving building practices; Tile Adhesive Mortar follows closely, propelled by the rising demand for ceramic and large-format tiles in residential and commercial spaces, providing strong bonding, flexibility, and resistance to moisture, thereby supporting the overall expansion through enhanced durability in high-traffic areas.

Based on Application Segment, the Dry Mortar market is divided into Plastering, Tiling, Flooring, Insulation Systems, and others.

The most dominant segment is Plastering, while the second most dominant is Tiling. Plastering dominates as it is essential for creating smooth, protective surfaces on walls and ceilings, offering excellent workability, crack resistance, and aesthetic finishes that are critical in both new constructions and renovations, driving the market by ensuring structural integrity and visual appeal; Tiling ranks second, fueled by its role in secure tile fixation with anti-slip and waterproof properties, which is vital for bathrooms, kitchens, and floors, contributing to market growth through improved hygiene and longevity in diverse applications.

Based on End-User Segment, the Dry Mortar market is divided into Residential, Commercial, Industrial, Infrastructure.

The most dominant segment is Residential, while the second most dominant is Commercial. Residential leads owing to the booming housing sector driven by urbanization and population growth, where dry mortar provides consistent quality for home building and repairs, enhancing comfort and value, thus propelling the market forward with its adaptability to various home improvement needs; Commercial follows, supported by the expansion of offices, retail spaces, and hospitality venues requiring durable, quick-to-apply materials for efficient project timelines, aiding market development by meeting demands for high-performance finishes in professional environments.

Recent Developments

- In June 2023, Baumit and Mondi announced a strategic collaboration to develop water-soluble bags for dry mix mortar, aiming to improve handling safety and reduce plastic waste in construction sites. This innovation allows the entire bag to dissolve in the mixer, eliminating the need for disposal and minimizing environmental impact while enhancing user convenience.

- In January 2025, Sika AG inaugurated a new mortar production facility in Singapore to boost supply chain efficiency and meet rising demand in the Asia-Pacific region. The plant focuses on sustainable manufacturing practices, incorporating advanced automation to produce high-quality dry mortars for various applications, supporting regional infrastructure growth.

- In August 2024, Sika AG expanded its production capacity at the Bekasi plant in Indonesia, specializing in advanced mortar mixes. This upgrade includes new lines for tile adhesives and waterproofing products, addressing local market needs for durable construction materials amid rapid urbanization and building projects.

- In January 2020, Ambuja Cement launched four new ranges of novel dry mortar solutions tailored for residential buildings. These products emphasize ease of use, superior adhesion, and eco-friendly compositions, catering to the growing preference for ready-to-mix options in home construction and renovation.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific stands out as the leading region in the dry mortar market, primarily driven by extensive construction activities in countries like China and India. The area's rapid urbanization has led to a surge in residential and commercial projects, where dry mortar is favored for its consistency and efficiency in large-scale developments. Governments here are heavily investing in infrastructure, such as high-speed railways and smart cities, which further amplifies demand. Additionally, the availability of abundant raw materials and a robust manufacturing base supports cost-effective production, making the region attractive for both local and international players. Cultural shifts toward modern building techniques also play a role, as traditional methods give way to pre-mixed solutions that save time and labor.

North America exhibits steady growth in the dry mortar market, with the United States as the dominant country due to its focus on infrastructure renewal and sustainable building practices. The region benefits from advanced construction technologies and stringent regulations that promote high-quality materials. Investments in commercial real estate and residential renovations drive adoption, particularly in urban centers. Innovation in product formulations, such as those with enhanced environmental profiles, aligns with consumer preferences for green construction. Moreover, the presence of established manufacturers fosters competition and product diversity, ensuring the market remains dynamic and responsive to evolving needs.

Europe maintains a strong position in the dry mortar market, led by Germany with its emphasis on energy-efficient and heritage-preserving constructions. The region's commitment to sustainability through policies like the EU Green Deal encourages the use of low-emission mortars. Refurbishment of aging infrastructure and a thriving hospitality sector contribute to demand. Countries here prioritize quality and durability, leading to widespread adoption in both new builds and restorations. Collaborative efforts among industry stakeholders enhance innovation, while a skilled workforce supports precise application, solidifying Europe's role in advancing market standards.

Latin America is emerging in the dry mortar market, with Brazil as the key dominating country fueled by urban expansion and government housing programs. The region sees increasing use in affordable housing and infrastructure projects like roads and bridges. Local manufacturers are adapting to economic fluctuations by offering cost-effective solutions. Growing awareness of construction efficiency drives shifts from traditional mixing to pre-blended products. Additionally, foreign investments in real estate bolster the market, creating opportunities for growth amid challenges like supply chain variability.

The Middle East & Africa region shows promising potential in the dry mortar market, dominated by the United Arab Emirates through ambitious projects in tourism and urban development. Iconic structures and smart city initiatives demand reliable materials for durability in harsh climates. Oil-rich economies invest in diversification, leading to commercial and residential booms. The focus on water conservation influences product choices, favoring efficient mortars. Regional partnerships with global firms introduce advanced technologies, enhancing local capabilities and market expansion.

Competitive Analysis

The global Dry Mortar market is dominated by players:

- Sika AG

- Saint-Gobain Weber

- Ardex Group

- CEMEX S.A.B. de C.V.

- LafargeHolcim

- Mapei SpA

- BASF SE

- Knauf

- Dow

- Parex Group

The global Dry Mortar market is segmented as follows:

By Type

- Thin Bed Mortar

- Tile Adhesive Mortar

- Repair Mortar

- Masonry Mortar

- Waterproofing Mortar

- Others

By Application

- Plastering

- Tiling

- Flooring

- Insulation Systems

- Others

By End-User

- Residential

- Commercial

- Industrial

- Infrastructure

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Dry Mortar market is dominated by players:

- Sika AG

- Saint-Gobain Weber

- Ardex Group

- CEMEX S.A.B. de C.V.

- LafargeHolcim

- Mapei SpA

- BASF SE

- Knauf

- Dow

- Parex Group

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors