![]()

Search Market Research Report

Dental 3D Printer Market Size, Share Global Analysis Report, 2026-2034

Dental 3D Printer Market Size, Share, Growth Analysis Report By Application (Orthodontics, Prosthodontics, Dentures, and Implantology), By Technology (Vat Photopolymerization, Polyjet Technology, Fused Deposition Modelling, Selective Laser Sintering, and Others), By End-use (Dental Clinics, Dental Laboratories, and Academic and Research Institutes), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

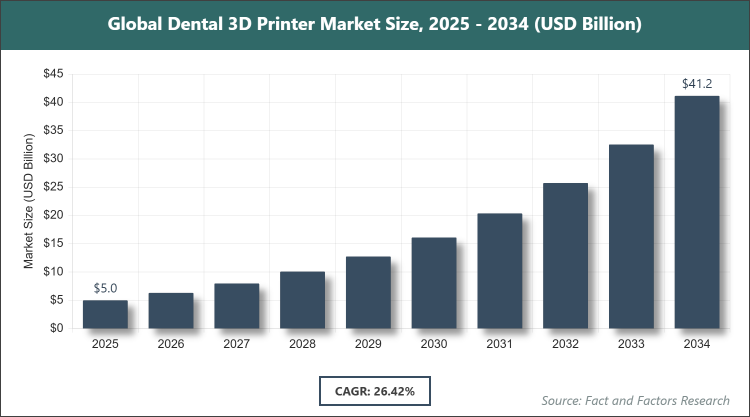

[220+ Pages Report] According to Facts & Factors, the global Dental 3D Printer market size was estimated at USD 4.99 billion in 2025 and is expected to reach USD 41.09 billion by the end of 2034. The Dental 3D Printer industry is anticipated to grow by a CAGR of 26.42% between 2026 and 2034. The Dental 3D Printer Market is driven by the quick uptake of digital dentistry and the rising need for individualized dental care.

Market Overview

Market Overview

The Dental 3D Printer market encompasses the use of additive manufacturing technologies specifically designed for producing dental appliances, models, and prosthetics. It involves specialized printers that utilize various materials to create precise, customized dental solutions such as aligners, crowns, bridges, surgical guides, and implants directly from digital scans. This market integrates digital workflows in dentistry, enabling rapid prototyping and production that enhances accuracy, reduces material waste, and improves patient outcomes through personalized treatments tailored to individual anatomical needs.

Key Insights

- As per the analysis shared by our research analyst, the global Dental 3D Printer market is estimated to grow annually at a CAGR of around 26.42% over the forecast period (2026-2034).

- In terms of revenue, the global Dental 3D Printer market size was valued at around USD 4.99 billion in 2025 and is projected to reach USD 41.09 billion, by 2034.

- The market is driven by the quick uptake of digital dentistry and the rising need for individualized dental care.

- Based on the Application, the Orthodontics segment dominated the market in 2025 with a share of 40% due to advancements in biocompatible materials enabling personalized solutions that improve functionality, aesthetics, and patient communication through graphical treatment progress displays.

- Based on the Technology, the Vat Photopolymerization segment dominated the market in 2025 due to its ability to produce high-resolution structures with precision for complex geometries, allowing on-demand production and reduced patient wait times.

- Based on the End-use, the Dental Laboratories segment dominated the market in 2025 with a share of 58% owing to innovations in personalized prostheses, scalability for high production volumes, and precise customization that is challenging with conventional methods.

- North America dominated the global Dental 3D Printer market in 2025 with 39% share because of a skilled workforce, early adoption for dental implants, crowns, bridges, dentures, and orthodontic products, along with proficient integration of cutting-edge technologies.

Growth Drivers

- Highly tailored appliances, implants, and restorations

The development of customized dental solutions through 3D printing allows for precise fits that enhance patient comfort and treatment efficacy, addressing individual variations in oral anatomy that traditional methods often overlook. This personalization reduces the need for adjustments post-production, leading to higher satisfaction rates among patients and practitioners alike.

By streamlining the design and manufacturing process, 3D printing minimizes errors associated with manual crafting, enabling faster turnaround times for dental procedures. As a result, dental professionals can handle more cases efficiently, boosting overall productivity in clinics and laboratories while meeting the growing demand for aesthetic and functional restorations.

- Ongoing developments in 3D printing technology, software, and materials

Advancements in printer hardware, such as improved resolution and speed, combined with sophisticated software for digital modeling, have expanded the capabilities of dental 3D printing to include intricate designs previously unachievable. These innovations facilitate seamless integration with CAD/CAM systems, enhancing workflow efficiency from scan to final product.

Material breakthroughs, including biocompatible resins and composites, ensure durability and safety for long-term use in the oral environment, encouraging wider adoption across various dental applications. This continuous evolution not only lowers production costs but also opens new avenues for research and application in complex cases like implantology and orthodontics.

Restraints

- Technological complexity requiring complex software

The intricate software ecosystems needed for 3D printing in dentistry often present compatibility issues between different systems, leading to potential inconsistencies in output quality and increased error rates during the design phase. This complexity demands specialized training for users, which can delay implementation and raise operational hurdles for smaller practices.

As software updates and integrations evolve rapidly, maintaining system harmony becomes a persistent challenge, potentially resulting in workflow disruptions and additional costs for troubleshooting. These factors can deter widespread adoption, particularly in regions with limited technical support infrastructure.

- Strict regulations for 3D-printed goods

Regulatory requirements for ensuring the safety and efficacy of 3D-printed dental products necessitate rigorous compliance testing, which can prolong market entry for new innovations and increase development expenses. Evolving standards require ongoing investments in quality assurance processes and documentation.

This stringent oversight, while essential for patient health, can slow down the pace of technological advancement and limit smaller manufacturers' ability to compete, as they may lack the resources to navigate complex approval pathways effectively.

Opportunities

- Development of biocompatible, highly durable materials

Innovations in materials like advanced ceramics and thermoplastics offer enhanced mechanical properties suitable for long-term dental applications, mimicking natural tooth aesthetics and strength. These materials expand the scope of 3D printing to more demanding uses, such as permanent prosthetics.

By improving material performance, opportunities arise for broader market penetration in cosmetic and restorative dentistry, attracting investment in R&D and fostering collaborations between material scientists and dental professionals to push boundaries further.

- Increasing popularity of digital dentistry

The shift toward digital workflows in dental practices creates avenues for integrating 3D printing seamlessly into daily operations, enhancing precision in diagnostics and treatment planning. This trend supports scalable production models that cater to rising patient expectations for quick, customized care.

As digital tools become more accessible, opportunities emerge for educational programs and partnerships that accelerate adoption, ultimately expanding the market reach to underserved areas and new demographic segments.

Challenges

- Navigating regulatory complexities

Maintaining compliance with varying international standards for quality and safety in 3D-printed dental devices requires constant vigilance and adaptation, which can strain resources for manufacturers. This ongoing need for regulatory alignment complicates global expansion efforts.

Challenges in standardizing testing protocols across regions may lead to delays in product launches and increased scrutiny, impacting innovation timelines and market competitiveness.

- Maintaining compliance with changing quality and safety standards

As standards evolve with technological advancements, companies must invest continually in training and equipment upgrades to meet new requirements, potentially diverting funds from core R&D activities. This dynamic environment demands agile strategies to avoid non-compliance risks.

The challenge is amplified for emerging players who may face barriers in accessing certified materials and processes, hindering their ability to scale operations effectively in a regulated industry.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 4.99 Billion |

Projected Market Size in 2034 |

USD 41.09 Billion |

CAGR Growth Rate |

26.42% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

3D Systems, Inc., Stratasys Ltd., Formlabs Inc., Renishaw plc, Prodways Group, Dentsply Sirona, SprintRay Inc., EnvisionTEC, Roland DG, Planmeca, SLM Solutions, Straumann, Carbon, DWS Systems, Align Technology, and Others. |

Key Segment |

By Application, By Technology, By End-use, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Dental 3D Printer market is segmented by Application, Technology, End-use, and region.

Based on Application Segment, the Dental 3D Printer market is divided into Orthodontics, Prosthodontics, Dentures, and Implantology. The most dominant segment is Orthodontics, which leads due to its ability to produce clear aligners and brackets customized to patient needs, driving market growth through improved treatment efficiency and patient compliance. The second most dominant is Prosthodontics, prominent because it enables rapid fabrication of crowns, bridges, and veneers with precise anatomical fits, contributing to overall market expansion by reducing production time and enhancing restorative outcomes in a single streamlined process.

Based on Technology Segment, the Dental 3D Printer market is divided into Vat Photopolymerization, Polyjet Technology, Fused Deposition Modelling, Selective Laser Sintering, and Others. The most dominant segment is Vat Photopolymerization, excelling in creating high-precision dental models and appliances that support complex geometries, propelling the market forward by enabling faster prototyping and customization. The second most dominant is Selective Laser Sintering, valued for its strength in producing durable metal frameworks for implants, aiding market growth through reliable, long-lasting solutions that meet the demands of advanced dental procedures.

Based on End-use Segment, the Dental 3D Printer market is divided into Dental Clinics, Dental Laboratories, and Academic and Research Institutes. The most dominant segment is Dental Laboratories, leading as it facilitates high-volume production of personalized prosthetics with superior accuracy, boosting the market by optimizing lab workflows and reducing costs. The second most dominant is Dental Clinics, growing rapidly due to on-site printing capabilities that allow same-day treatments, driving overall market progress by improving patient access to immediate, tailored dental care.

Recent Developments

- In September 2024, Formlabs launched three post-processing tools and two new resin materials, Clear Cast Resin and third-party Certified Material BEGO VarseoSmile TriniQ Resin, expanding its material range to over 45 for enhanced dental applications.

- In May 2024, SprintRay announced a partnership with Ivoclar, revealed the Pro 2 desktop 3D printer, and plans to validate Ivoclar resins with its ecosystem to broaden restorative material access, enabling faster patient care.

- In July 2024, Stratasys launched the DentaJet XL, a high-speed 3D printer designed to enhance dental lab productivity and significantly reduce operational costs through efficient multi-material printing.

- Align Technology acquired Austrian polymer 3D printing startup Cubicure for 79 million euros to support its strategic innovation roadmap, enhancing 3D printing capabilities for Invisalign molds and direct product printing.

Regional Analysis

- North America to dominate the global market

North America leads the Dental 3D Printer market, with the United States as the dominating country, owing to its advanced healthcare infrastructure and high concentration of skilled dental professionals who readily integrate innovative technologies. The region's emphasis on research and development fosters collaborations between universities and industry leaders, accelerating the adoption of digital workflows in dentistry. Additionally, supportive government policies and insurance frameworks encourage investment in cutting-edge equipment, making personalized dental solutions more accessible to a diverse patient base.

Asia-Pacific is experiencing rapid growth in the Dental 3D Printer market, with China and Japan as key dominating countries, driven by increasing urbanization and rising disposable incomes that boost demand for cosmetic and restorative dental procedures. The region's expanding middle class seeks aesthetic enhancements, prompting dental practices to adopt advanced printing technologies for efficient, customized treatments. Moreover, government initiatives in healthcare modernization and partnerships with global tech firms enhance local manufacturing capabilities, positioning Asia-Pacific as a hub for innovation in affordable dental solutions.

Europe holds a strong position in the Dental 3D Printer market, with Germany as the dominating country, benefiting from its robust engineering heritage and stringent quality standards that ensure high-precision dental products. The continent's aging population drives demand for reliable prosthetics and implants, supported by comprehensive healthcare systems that reimburse advanced treatments. Collaborative efforts among European nations in research consortia further advance material sciences, enabling the development of biocompatible prints that cater to diverse clinical needs across the region.

Latin America is emerging in the Dental 3D Printer market, with Brazil as the dominating country, where growing private dental clinics and rising awareness of oral health propel technology adoption. The region's focus on dental tourism attracts international patients seeking cost-effective, high-quality treatments, encouraging local practitioners to invest in 3D printing for competitive advantages. Improving economic conditions and educational programs in digital dentistry are gradually bridging the gap between traditional methods and modern innovations.

The Middle East & Africa region is gaining traction in the Dental 3D Printer market, with the United Arab Emirates as the dominating country, leveraging its status as a medical tourism destination to integrate advanced dental technologies. Investments in state-of-the-art healthcare facilities and partnerships with global suppliers enhance access to customized dental care. Rising affluence and government efforts to diversify economies beyond oil contribute to expanding dental infrastructure, fostering a market for precise, efficient printing solutions.

Competitive Analysis

The global Dental 3D Printer market is dominated by players:

- 3D Systems, Inc.

- Stratasys Ltd.

- Formlabs Inc.

- Renishaw plc

- Prodways Group

- Dentsply Sirona

- SprintRay Inc.

- EnvisionTEC

- Roland DG

- Planmeca

- SLM Solutions

- Straumann

- Carbon

- DWS Systems

- Align Technology

The global Dental 3D Printer market is segmented as follows:

By Application

- Orthodontics

- Prosthodontics

- Dentures

- Implantology

By Technology

- Vat Photopolymerization

- Polyjet Technology

- Fused Deposition Modelling

- Selective Laser Sintering

- Others

By End-use

- Dental Clinics

- Dental Laboratories

- Academic and Research Institutes

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Dental 3D Printer market is dominated by players:

- 3D Systems, Inc.

- Stratasys Ltd.

- Formlabs Inc.

- Renishaw plc

- Prodways Group

- Dentsply Sirona

- SprintRay Inc.

- EnvisionTEC

- Roland DG

- Planmeca

- SLM Solutions

- Straumann

- Carbon

- DWS Systems

- Align Technology

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors