![]()

Search Market Research Report

Defoamers Market Size, Share Global Analysis Report, 2026-2034

Defoamers Market Size, Share, Growth Analysis Report By Product Type (Silicone-based, Oil-based, Water-based, Powder-based, EO/PO-based, and Others), By Application (Pulp & Paper, Water Treatment, Paints & Coatings, Food & Beverages, Pharmaceuticals, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

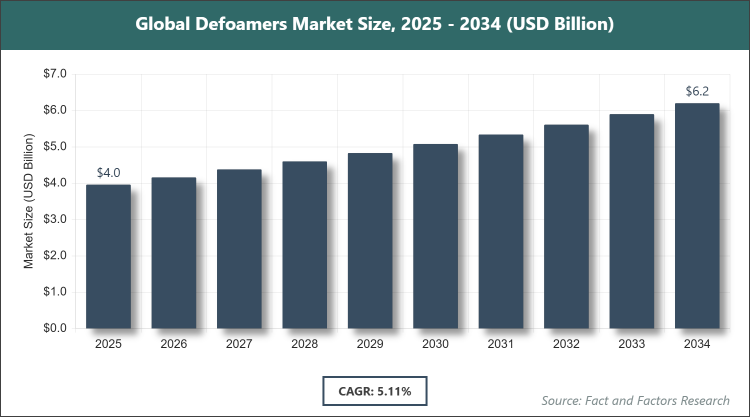

[220 Pages Report] According to Facts & Factors, the global Defoamers market size was estimated at USD 3.96 billion in 2025 and is expected to reach USD 6.20 billion by the end of 2034. The Defoamers industry is anticipated to grow by a CAGR of 5.11% between 2026 and 2034. The Defoamers Market is driven by increasing industrial expansion and stringent environmental regulations.

Market Overview

Market Overview

Defoamers, also known as anti-foaming agents, are chemical additives designed to reduce or eliminate foam formation in industrial processes. These agents work by destabilizing foam bubbles, preventing overflow, equipment damage, and process inefficiencies across various industries such as manufacturing, wastewater treatment, and food processing. Defoamers are essential in maintaining operational efficiency and product quality without interfering with the primary process.

Key Insights

- As per the analysis shared by our research analyst, the global Defoamers market is estimated to grow annually at a CAGR of around 5.11% over the forecast period (2026-2034).

- In terms of revenue, the global Defoamers market size was valued at around USD 3.96 billion in 2025 and is projected to reach USD 6.20 billion by 2034.

- The market is driven by stringent environmental regulations, sustainability targets, technological advancements, and rapid industrial expansion in emerging economies.

- Based on the Product Type, the Silicone-based segment dominated the market with a share of 36% due to its high efficiency, versatility, and compatibility with a wide range of industrial processes, making it ideal for applications requiring robust foam control.

- Based on the Application, the Pulp & Paper segment dominated with a share of 25% owing to the intensive foam generation during papermaking processes, where defoamers ensure smooth operations, improved productivity, and reduced downtime.

- Based on region, Asia Pacific dominated with a share of 39% because of rapid industrialization, infrastructure development, and increasing demand from key sectors like paints, coatings, and wastewater treatment in countries such as China and India.

Growth Drivers

- Industrial Expansion and Urbanization

The global Defoamers market is experiencing significant growth due to rapid industrialization and urbanization, particularly in emerging economies. This expansion has led to increased demand in sectors like construction, paints, textiles, and coatings, where foam control is critical for efficient operations. Technological advancements in defoamer formulations, such as bio-based and low-VOC options, further support market growth by aligning with sustainability goals and regulatory requirements.

Additionally, the shift towards clean water practices and advanced wastewater treatment systems has boosted the adoption of defoamers in aeration tanks and membrane bioreactors, enhancing process efficiency and reducing environmental impact.

Restraints

- High R&D Costs and Raw Material Volatility

The development of advanced, sustainable defoamers involves substantial research and development costs, which can hinder market growth for smaller players. Stringent regulations require continuous innovation to meet eco-friendly standards, increasing financial burdens. Moreover, fluctuations in petroleum-based raw material prices add uncertainty, affecting production costs and profitability.

These factors may slow down the adoption of new technologies and limit market expansion in price-sensitive regions, potentially leading to supply chain disruptions and higher end-product prices.

Opportunities

- Development of Nanoparticle-Based Defoamers

Innovations in nanoparticle-based defoamers, including nano-emulsions and anti-foam agents, present significant opportunities for enhanced efficiency and reduced chemical usage. These advanced formulations align with green chemistry principles, lowering chemical oxygen demand in wastewater and supporting sustainability initiatives.

The growing demand for eco-friendly solutions in industries like semiconductors and bio-pharmaceuticals opens new avenues for market players to introduce specialized products, potentially capturing untapped segments and driving long-term growth.

Challenges

- Regulatory Compliance and Sustainability Pressures

Meeting diverse global environmental regulations poses a challenge, as defoamer formulations must comply with varying standards on VOC emissions and biodegradability. This complexity can delay product launches and increase compliance costs.

Furthermore, the push for sustainable, non-silicone alternatives requires ongoing innovation, but limited access to bio-based raw materials and technical expertise may impede progress, affecting competitiveness in a rapidly evolving market.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 3.96 Billion |

Projected Market Size in 2034 |

USD 6.20 Billion |

CAGR Growth Rate |

5.11% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

BASF SE, Evonik Industries AG, Dow Inc., Kemira Oyj, Shin-Etsu Chemical Co., Ltd., Air Products and Chemicals, Inc., Ashland Global Holdings Inc., Clariant AG, Wacker Chemie AG, Huntsman Corporation, Momentive Performance Materials Inc., Elkem ASA, Solvay S.A., Elementis PLC, BYK-Chemie GmbH (ALTANA Group), Munzing Chemie GmbH, SAGITTA (KCC Corporation), Kao Corporation, Resil Chemicals Pvt. Ltd., King Industries, Inc., and Others. |

Key Segment |

By Product Type, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Defoamers market is segmented by product type, application, and region.

Based on Product Type Segment, the Defoamers market is divided into Silicone-based, Oil-based, Water-based, Powder-based, EO/PO-based, and Others.

The most dominant segment is Silicone-based, holding a significant market share due to its superior performance in high-temperature and harsh environments, which enhances foam control efficiency and process stability. The second most dominant is Water-based, favored for its eco-friendly properties and compatibility with aqueous systems, driving market growth by meeting regulatory demands for low-VOC products and supporting sustainable industrial practices in sectors like food processing and wastewater treatment.

Based on Application Segment, the Defoamers market is divided into Pulp & Paper, Water Treatment, Paints & Coatings, Food & Beverages, Pharmaceuticals, and Others.

The most dominant segment is Pulp & Paper, capturing a substantial portion owing to the high foam generation in pulping and papermaking, where defoamers prevent overflows and improve machine runnability, ultimately boosting productivity and reducing operational costs. The second most dominant is Paints & Coatings, driven by the need for foam-free formulations in waterborne systems, which helps achieve smooth finishes, better adhesion, and compliance with environmental standards, thereby accelerating market expansion through innovation in green chemistry.

Recent Developments

- In November 2024, Evonik launched TEGO Foamex 16 and TEGO Foamex 11, sustainable waterborne defoamers for architectural coatings, emphasizing bio-based components to reduce environmental impact.

- In November 2023, BASF expanded its production capacity at the Dilovasi plant in Turkey for Foamaster and Foamstar defoamer brands, aiming to meet growing demand in the EMEA region.

- In April 2024, Evonik introduced sustainable TEGO Foamex 16 and 11 for architectural coatings, focusing on low-VOC and high-efficiency foam control.

- Arkema acquired Ashland’s defoamer technologies in 2024 to strengthen its portfolio in specialty chemicals for industrial applications.

- Clariant acquired a specialty startup in late 2024 for biodegradable defoaming agents, enhancing its sustainable product offerings.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region dominates the Defoamers market, driven by rapid industrialization and infrastructure development in countries like China, India, and Japan. China stands out as the dominating country, with expansive manufacturing sectors in paints, coatings, and textiles requiring effective foam control solutions. The region's focus on sustainable practices and technological innovations further bolsters demand, as industries adopt eco-friendly defoamers to comply with environmental norms. Growing urbanization and investments in wastewater treatment facilities contribute to market leadership, fostering a competitive landscape with local and international players. This dominance is expected to continue as economic growth accelerates process efficiencies across diverse applications.

North America holds a significant position in the Defoamers market, led by the United States as the dominating country due to advanced technological infrastructure and stringent regulatory frameworks. The region's emphasis on bio-based and low-emission defoamers in pharmaceuticals, food processing, and water treatment drives innovation and adoption. High investments in R&D for sustainable solutions enhance market dynamics, while the shift towards green chemistry in industrial processes supports growth. Collaborative efforts between key players and regulatory bodies ensure compliance, positioning North America as a hub for high-performance defoamers and contributing to global market trends.

Europe exhibits strong growth in the Defoamers market, with Germany as the dominating country owing to its robust chemical industry and commitment to environmental sustainability. The region's strict regulations on VOC emissions and waste management propel the demand for innovative, biodegradable defoamers in sectors like automotive coatings and pulp processing. Emphasis on circular economy principles encourages the development of eco-friendly formulations, attracting investments in advanced technologies. Collaborative research initiatives and partnerships among leading firms foster market expansion, ensuring Europe remains a key contributor to global advancements in foam control solutions.

Latin America is emerging in the Defoamers market, with Brazil as the dominating country fueled by expanding agricultural and industrial sectors. The region's focus on agrochemicals and food processing necessitates effective defoamers to enhance productivity and quality. Growing awareness of environmental impacts drives the adoption of water-based and bio-derived products, supported by government initiatives for sustainable development. Investments in infrastructure and manufacturing further stimulate demand, positioning Latin America for steady growth through regional collaborations and technological integrations.

The Middle East & Africa region shows potential in the Defoamers market, dominated by Saudi Arabia due to its thriving oil & gas and construction industries. The need for efficient foam control in water treatment and petrochemical processes drives market uptake. Increasing investments in desalination and wastewater management align with sustainability goals, promoting the use of specialized defoamers. Regional economic diversification efforts and partnerships with global players enhance technological capabilities, paving the way for market expansion amid evolving industrial landscapes.

Competitive Analysis

The global Defoamers market is dominated by players:

- BASF SE

- Evonik Industries AG

- Dow Inc.

- Kemira Oyj

- Shin-Etsu Chemical Co., Ltd.

- Air Products and Chemicals, Inc.

- Ashland Global Holdings Inc.

- Clariant AG

- Wacker Chemie AG

- Huntsman Corporation

- Momentive Performance Materials Inc.

- Elkem ASA

- Solvay S.A.

- Elementis PLC

- BYK-Chemie GmbH (ALTANA Group)

- Munzing Chemie GmbH

- SAGITTA (KCC Corporation)

- Kao Corporation

- Resil Chemicals Pvt. Ltd.

- King Industries, Inc.

The global Defoamers market is segmented as follows:

By Product Type

- Silicone-based

- Oil-based

- Water-based

- Powder-based

- EO/PO-based

- Others

By Application

- Pulp & Paper

- Water Treatment

- Paints & Coatings

- Food & Beverages

- Pharmaceuticals

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Defoamers market is dominated by players:

- BASF SE

- Evonik Industries AG

- Dow Inc.

- Kemira Oyj

- Shin-Etsu Chemical Co., Ltd.

- Air Products and Chemicals, Inc.

- Ashland Global Holdings Inc.

- Clariant AG

- Wacker Chemie AG

- Huntsman Corporation

- Momentive Performance Materials Inc.

- Elkem ASA

- Solvay S.A.

- Elementis PLC

- BYK-Chemie GmbH (ALTANA Group)

- Munzing Chemie GmbH

- SAGITTA (KCC Corporation)

- Kao Corporation

- Resil Chemicals Pvt. Ltd.

- King Industries, Inc.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors