![]()

Search Market Research Report

Copper Market Size, Share Global Analysis Report, 2026-2034

Copper Market Size, Share, Growth Analysis Report By Product Type (Primary, Secondary), By End-Use Industry (Construction, Electrical & Electronics, Automotive & Heavy Equipment, Industrial, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

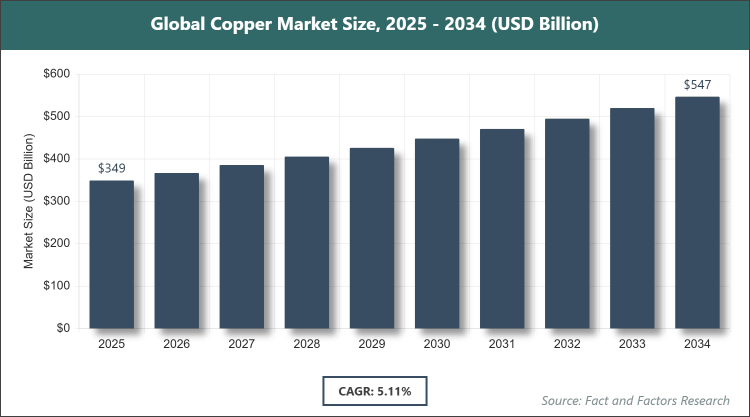

[220+ Pages Report] According to Facts & Factors, the global Copper market size was estimated at USD 349.14 billion in 2025 and is expected to reach USD 548.20 billion by the end of 2034. The Copper industry is anticipated to grow by a CAGR of 5.11% between 2026 and 2034. The Copper Market is driven by rising demand in construction and infrastructure.

Market Overview

Market Overview

The copper market encompasses the global industry involved in the mining, refining, production, and distribution of copper, a highly conductive and durable metal widely used across various sectors due to its excellent electrical and thermal properties, corrosion resistance, and malleability. It includes the supply chain from raw ore extraction to the creation of refined copper products and alloys, serving as a critical raw material in manufacturing processes.

Key Insights

- As per the analysis shared by our research analyst, the global Copper market is estimated to grow annually at a CAGR of around 5.11% over the forecast period (2026-2034).

- In terms of revenue, the global Copper market size was valued at around USD 349.14 Billion in 2025 and is projected to reach USD 548.20 Billion, by 2034.

- The market is driven by growing use of electronic devices, renewable energy systems, infrastructure projects, and rapid industrialization in emerging economies.

- Based on the product type, Primary dominated with 62% share due to its fundamental role in the copper production supply chain through mining and refining, meeting high demand in key industries like construction and electronics amid global infrastructure growth.

- Based on the end-use industry, Construction dominated with 32% share because copper is essential for electrical wiring, plumbing systems, and HVAC applications in residential, commercial, and industrial buildings, driven by worldwide urbanization and infrastructure development.

- Based on the region, Asia Pacific dominated with 39% share owing to rapid industrialization, urbanization, and high demand in construction, automotive, and electronics sectors, supported by major producers like China.

Growth Drivers

- Rising Demand in Renewable Energy and Electronics

The increasing adoption of renewable energy sources such as solar and wind power has significantly boosted the demand for copper, which is integral to electrical components, wiring, and grid infrastructure. This shift towards sustainable energy solutions, coupled with government incentives and global climate goals, is propelling market growth by creating new applications for copper in efficient energy transmission and storage systems.

Additionally, the proliferation of electronic devices, including smartphones, tablets, and advanced telecommunications networks like 5G, relies heavily on copper for printed circuit boards and data transmission. Technological advancements in automation and smart devices further amplify this demand, as copper's superior conductivity ensures reliable performance in high-tech environments, driving sustained expansion in the market.

Restraints

- Environmental Concerns from Mining Activities

Copper mining and production processes raise significant environmental issues, including habitat disruption, water contamination, and high greenhouse gas emissions, leading to stricter regulatory scrutiny and increased operational costs for companies. These concerns are prompting shifts towards sustainable practices and recycling, which can limit primary production growth and create supply chain uncertainties.

Public and investor pressure for eco-friendly operations is intensifying, with regulations in many regions mandating reduced environmental footprints. This not only elevates compliance expenses but also diverts investment towards alternative materials or recycled copper, potentially restraining the overall market expansion as primary sources face heightened challenges in maintaining profitability and social license to operate.

Opportunities

- Expansion in Electric Vehicles Sector

The surge in electric vehicle (EV) production presents substantial opportunities for the copper market, as EVs require significantly more copper for motors, batteries, wiring, and charging infrastructure compared to traditional vehicles. Government mandates for cleaner transportation and consumer preferences for sustainable mobility are accelerating this trend, fostering innovation in copper-intensive EV technologies.

Advancements in battery designs and fast-charging networks further enhance copper's role, aligning with global efforts to combat climate change. This creates avenues for market players to invest in specialized copper products, partnerships with automakers, and supply chain optimizations, positioning the industry for long-term growth amid the transition to electrified transportation systems.

Challenges

- Balancing Sustainability with Supply Demands

Achieving sustainable mining practices while meeting escalating global copper demand poses a major challenge, as environmental regulations and community opposition can delay projects and increase costs. The industry must navigate these pressures by investing in green technologies and ethical sourcing, which requires significant capital and innovation.

Competition from recycled copper and alternative materials adds complexity, as recycling reduces reliance on primary mining but may not fully satisfy demand surges. Investor preferences for environmentally responsible companies further complicate operations, demanding a strategic balance between profitability, regulatory compliance, and long-term resource management to sustain market growth without exacerbating ecological impacts.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 349.14 Billion |

Projected Market Size in 2034 |

USD 548.20 Billion |

CAGR Growth Rate |

5.11% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Codelco, BHP Group, Glencore, Freeport-McMoRan, Southern Copper Corporation, Rio Tinto, Anglo American, Jiangxi Copper Corporation, First Quantum Minerals, Lundin Mining, Antofagasta, KGHM Polska Miedz, Teck Resources, Hudbay Minerals, OZ Minerals, and Others. |

Key Segment |

By Product Type, By End-Use Industry, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Copper market is segmented by product type, end-use industry, and region.

Based on Product Type Segment, the Copper market is divided into Primary, Secondary, and others.

The most dominant segment is Primary, which holds the largest share due to its direct extraction from ores providing high-purity copper essential for critical applications in electrical and construction industries; it drives the market by ensuring a stable supply chain for high-volume demands in infrastructure and electronics, supported by ongoing mining investments in resource-rich regions. The second most dominant is Secondary, derived from recycling, which gains traction for its sustainability benefits reducing environmental impact and costs; it contributes to market growth by supplementing primary supplies during shortages and aligning with global circular economy initiatives, particularly in mature economies focused on waste reduction.

Based on End-Use Industry Segment, the Copper market is divided into Construction, Electrical & Electronics, Automotive & Heavy Equipment, Industrial, Others, and others.

The most dominant segment is Construction, capturing a significant portion as copper's durability and conductivity make it indispensable for wiring, plumbing, and roofing in buildings; it propels market expansion through urbanization and infrastructure projects worldwide, where reliable materials are needed for long-term structural integrity. The second most dominant is Electrical & Electronics, driven by copper's superior electrical properties in circuits, transformers, and devices; this segment boosts the market by supporting the growth of consumer electronics, renewable energy systems, and telecommunications, where efficient power transmission is crucial for technological advancements.

Recent Developments

- In February 2025, former executives from Glencore and Lundin Gold launched Moranda Metals, a private mining shell company aimed at acquiring gold, silver, and copper assets in the Americas, capitalizing on high commodity prices despite limited investor interest in public mining firms.

- In April 2025, Adani Enterprises Ltd announced preparations to commence operations at a major copper smelter, positioned as the world's largest metallurgical complex for copper and other metals, enhancing global production capacity.

- In September 2024, Electroninks introduced an advanced conductive copper ink line for applications such as seed layer printing, fine-line metallization, and RDL formation, improving manufacturing efficiency and reducing costs in electronics production.

- In October 2023, Livpure released a new copper water purifier featuring an 8.5-liter storage capacity and a copper-made insect-proof tank, targeting health-conscious consumers with enhanced water purification technology.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region stands out due to its rapid economic expansion and massive infrastructure investments, where countries like China lead in copper consumption for manufacturing and urban development. This area's dominance stems from a robust industrial base that integrates copper into everything from high-speed rail to smart cities, fostering innovation in material usage. China's position as a top producer and consumer ensures supply stability, while emerging markets like India contribute through government-led projects in housing and transportation. The region's focus on export-oriented industries further solidifies its role, creating a dynamic ecosystem that attracts global investments and technological collaborations.

North America exhibits strong growth potential, particularly in the United States and Canada, where advanced manufacturing and renewable energy initiatives drive copper demand. The U.S. benefits from a mature automotive sector transitioning to electric vehicles, alongside investments in grid modernization. Canada's mining heritage provides a reliable domestic supply, supporting industries like electronics and construction. Emphasis on sustainable practices and innovation in alloy development enhances competitiveness, while trade agreements facilitate access to international markets. This region's blend of technological prowess and resource availability positions it as a key player in high-value copper applications.

Europe maintains a significant presence, with Germany as a leading force in engineering and automotive sectors that heavily rely on copper for precision components. The continent's commitment to the European Green Deal promotes copper use in renewable energy and energy-efficient buildings. Countries like the UK and France invest in infrastructure upgrades, integrating copper for its longevity in electrical systems. Italy's focus on design and manufacturing adds value through specialized products. Overall, Europe's regulatory environment encourages recycling and innovation, creating a balanced market that prioritizes quality and environmental standards in copper utilization.

Latin America contributes notably, with Chile dominating as the world's largest copper producer through extensive mining operations. The region's rich mineral deposits support export-driven economies, feeding global supply chains. Brazil's industrial growth in construction and transportation amplifies demand, while Peru's expanding mines add to production capacity. Political stability in key countries enables foreign investments, enhancing extraction technologies. This area's strategic location facilitates trade with Asia and North America, positioning it as a vital supplier in the global copper landscape.

The Middle East & Africa region shows emerging potential, with South Africa leading in mining and refining capabilities. Growing urbanization in countries like the UAE drives construction-related copper use in skyscrapers and infrastructure. Saudi Arabia's Vision 2030 initiative boosts demand through diversification into non-oil sectors, including electronics. Africa's vast untapped reserves attract international partnerships for exploration. Challenges like infrastructure deficits are offset by increasing foreign aid and investments, gradually integrating the region into global copper value chains.

Competitive Analysis

The global Copper market is dominated by players:

- Codelco

- BHP Group

- Glencore

- Freeport-McMoRan

- Southern Copper Corporation

- Rio Tinto

- Anglo American

- Jiangxi Copper Corporation

- First Quantum Minerals

- Lundin Mining

- Antofagasta

- KGHM Polska Miedz

- Teck Resources

- Hudbay Minerals

- OZ Minerals

The global Copper market is segmented as follows:

By Product Type

- Primary

- Secondary

By End-Use Industry

- Construction

- Electrical & Electronics

- Automotive & Heavy Equipment

- Industrial

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors