![]()

Search Market Research Report

Building Information Modeling (BIM) Market Size, Share Global Analysis Report, 2026-2034

Building Information Modeling (BIM) Market Size, Share, Growth Analysis Report By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Project Lifecycle (Pre-Construction, Construction, Operation), By Application (Commercial, Residential, Industrial), By End-User (Architects/Engineers, Contractors, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

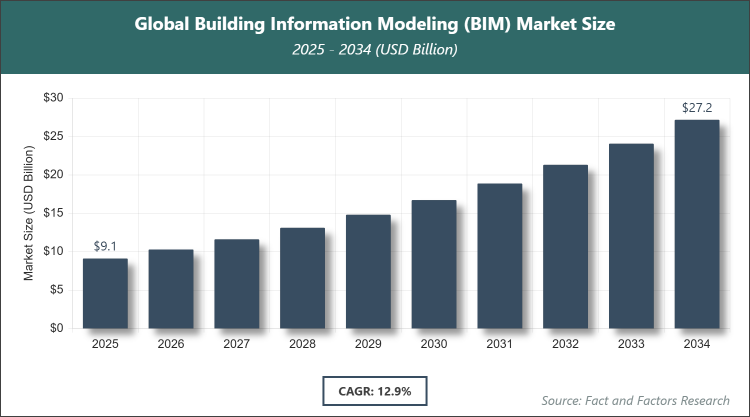

[250 Pages Report] According to Facts & Factors, the global Building Information Modeling (BIM) market size was estimated at USD 9.12 billion in 2025 and is expected to reach USD 27.12 billion by 2034, growing at a CAGR of 12.9% from 2026 to 2034. Building Information Modeling (BIM) Market is driven by increasing government mandates and adoption of digital technologies for enhanced construction efficiency.

Market Overview

Market Overview

Building Information Modeling (BIM) refers to a collaborative process that utilizes digital representations of physical and functional characteristics of places, enabling architects, engineers, and construction professionals to plan, design, construct, and manage buildings and infrastructure more effectively. It integrates multi-disciplinary data to create detailed digital models managed in an open cloud platform for real-time collaboration throughout the project lifecycle.

Key Insights

- The global BIM market size was valued at USD 9.12 Billion in 2025 and is projected to reach USD 27.12 Billion by 2034.

- The market is expected to grow at a CAGR of 12.9% during the forecast period.

- The market is driven by government mandates for BIM adoption in public projects, rapid urbanization, and integration with advanced technologies like AI and IoT.

- Based on the Component segment, the Software subsegment dominated with 65% share due to its essential role in core modeling, simulation, and data integration functions.

- Based on the Deployment Mode segment, the Cloud subsegment dominated with 55% share owing to its scalability, remote collaboration features, and lower upfront costs for SMEs.

- Based on the Project Lifecycle segment, the Pre-Construction subsegment dominated with 45% share as it enables early planning, design optimization, and risk mitigation before physical work begins.

- Based on the Application segment, the Commercial subsegment dominated with 40% share driven by high demand in retail, office, and hospitality projects for efficient space utilization and sustainability.

- Based on the End-User segment, the Architects/Engineers subsegment dominated with 50% share because BIM tools are fundamental for design accuracy and interdisciplinary coordination.

- North America dominated the global market with 40% share attributed to early technology adoption, strong government support, and advanced infrastructure development.

Market Dynamics

Growth Drivers

- Government Mandates and Regulations

Government initiatives worldwide are pushing for mandatory BIM adoption in public infrastructure projects to enhance transparency, reduce costs, and improve project outcomes. For instance, policies in the UK, US, and Singapore require BIM for large-scale developments, fostering standardized practices and encouraging private sector alignment.

This regulatory push not only streamlines approval processes but also minimizes rework and delays, leading to significant time and cost savings across the construction value chain. As more countries implement similar mandates, the demand for BIM solutions surges, particularly in emerging economies investing in smart cities and sustainable infrastructure.

- Technological Advancements and Integration

The integration of BIM with emerging technologies like AI, IoT, AR/VR, and cloud computing is revolutionizing construction workflows by enabling predictive analytics, real-time monitoring, and immersive visualizations. These enhancements allow for better decision-making and error reduction during design and execution phases.

Furthermore, AI-driven BIM tools automate clash detection and optimize resource allocation, while IoT enables data collection from on-site sensors for ongoing performance tracking. This convergence of technologies is attracting investments from construction firms seeking competitive edges in efficiency and innovation.

- Rising Focus on Sustainability and Energy Efficiency

With global emphasis on green building practices, BIM facilitates energy modeling, material optimization, and lifecycle assessments to meet environmental standards like LEED and BREEAM. It helps simulate building performance to minimize carbon footprints and operational costs over time.

This driver is particularly relevant amid climate change concerns, where stakeholders prioritize eco-friendly designs. BIM's ability to integrate sustainability metrics early in projects reduces waste and supports compliance with stringent environmental regulations, driving adoption in residential and commercial sectors.

Restraints

- High Initial Implementation Costs

The upfront expenses for BIM software, hardware, training, and integration can be prohibitive, especially for small and medium-sized enterprises (SMEs) in the construction industry. These costs include licensing fees, specialized equipment, and workflow reconfiguration, often deterring widespread adoption.

Additionally, the return on investment may not be immediate, leading to hesitation among cost-sensitive firms. In developing regions, limited access to affordable technology further exacerbates this barrier, slowing market penetration despite long-term benefits.

- Lack of Skilled Professionals

There is a significant shortage of trained personnel proficient in BIM tools and processes, which hampers effective implementation and utilization. Many traditional construction workers and firms lack the digital skills required, resulting in underutilization of BIM capabilities.

This skills gap necessitates extensive training programs, which add to operational disruptions and costs. As the industry transitions to digital practices, addressing this restraint through education and certification is crucial, but current deficiencies continue to limit growth potential.

Opportunities

- Expansion in Emerging Markets

Rapid urbanization in Asia-Pacific and Latin America presents opportunities for BIM adoption in large-scale infrastructure projects like smart cities and transportation networks. Governments in these regions are increasingly investing in digital construction to support economic growth.

This creates demand for tailored BIM solutions that address local challenges, such as resource constraints and regulatory variations. Partnerships with local firms can facilitate market entry, unlocking new revenue streams for global players.

- Integration with Digital Twins and Smart Cities

The rise of digital twins—virtual replicas of physical assets—offers opportunities for BIM to extend into operations and maintenance phases, enabling predictive maintenance and real-time optimization. This is particularly valuable for smart city initiatives focusing on interconnected urban systems.

By leveraging BIM data for digital twins, stakeholders can enhance asset longevity and urban planning. This trend aligns with global smart city investments, providing avenues for innovation and expanded service offerings.

Challenges

- Interoperability and Data Security Issues

Incompatibility between different BIM software platforms leads to data silos and collaboration challenges among project stakeholders using varied tools. Standardizing formats like IFC helps, but inconsistencies persist, affecting project efficiency.

Moreover, as BIM involves sharing sensitive data in cloud environments, cybersecurity risks such as data breaches and intellectual property theft are heightened. Ensuring robust encryption and compliance with data protection regulations is essential but complex in multi-vendor ecosystems.

- Resistance to Change in Traditional Practices

The construction industry's reliance on conventional methods creates cultural resistance to adopting BIM, with stakeholders viewing it as disruptive to established workflows. This inertia is more pronounced in smaller firms or regions with limited digital infrastructure.

Overcoming this requires demonstrating tangible benefits through case studies and pilot projects, but slow cultural shifts can delay market growth. Education and incentives are key to addressing this challenge over time.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 9.12 Billion |

Projected Market Size in 2034 |

USD 27.12 Billion |

CAGR Growth Rate |

12.9% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Autodesk Inc., Bentley Systems, Inc., Trimble Inc., Nemetschek Group, Dassault Systèmes, and Others. |

Key Segment |

By Component, By Deployment Mode, By Project Lifecycle, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The BIM market is segmented by component, deployment mode, project lifecycle, application, end-user, and region.

Based on Component Segment, the BIM market is divided into Software and Services.the dominant subsegment is Software, holding 65% share, as it forms the core of BIM processes, enabling 3D modeling, simulation, and data management that drive project accuracy and efficiency. The second dominant is Services, which supports implementation, training, and customization, helping firms maximize software value and integrate BIM into workflows, thus accelerating market growth through expert guidance.

Based on Deployment Mode Segment, the BIM market is divided into On-Premises and Cloud.The dominant subsegment is Cloud, with 55% share, due to its flexibility, cost-effectiveness, and ability to facilitate real-time collaboration across global teams, reducing the need for heavy infrastructure investments. The second dominant is On-Premises, preferred for data-sensitive projects requiring high control and security, contributing to market expansion by catering to enterprises with strict compliance needs.

Based on Project Lifecycle Segment, the BIM market is divided into Pre-Construction, Construction, and Operation.The dominant subsegment is Pre-Construction, capturing 45% share, as it allows for detailed planning, risk assessment, and design optimization early on, minimizing costly changes later and boosting overall project success rates. The second dominant is Construction, which uses BIM for on-site coordination and progress tracking, driving market growth by improving execution efficiency and reducing delays.

Based on Application Segment, the BIM market is divided into Commercial, Residential, and Industrial.The dominant subsegment is Commercial, with 40% share, driven by complex requirements in offices, retail, and hospitality for space efficiency, sustainability, and regulatory compliance, where BIM enhances design and operations. The second dominant is Industrial, supporting large-scale facilities with intricate systems, contributing to market advancement through better asset management and safety.

Based on End-User Segment, the BIM market is divided into Architects/Engineers, Contractors, and Others.The dominant subsegment is Architects/Engineers, holding 50% share, as BIM is integral for precise design, collaboration, and simulation, enabling innovative and error-free outputs that propel industry standards. The second dominant is Contractors, who leverage BIM for construction planning and resource optimization, fostering market growth by streamlining on-site activities and cost control.

Recent Developments

In February 2026, the National Standards Authority of Ireland (NSAI) launched 'BIM Essentials' and 'BIM Advanced' standards collections, aimed at aligning with international best practices and supporting the government's Housing for All initiative to improve project coordination, sustainability, and cost reduction in construction.

In January 2026, Esri AEC highlighted the integration of BIM with mapping and analytics in Construction Executive Magazine, emphasizing how forward-thinking firms use these tools for informed decision-making, design simulation, and outcome prediction to enhance project efficiency.

In February 2026, discussions in industry forums noted the revolutionary impact of BIM combined with AI in 2026, including AI integration for design, cost estimation, and predictive conflict detection, alongside growing demands for specialists and governmental mandates for BIM in construction projects.

Regional Analysis

- North America to dominate the global market

North America holds the largest share in the BIM market, driven by advanced technological infrastructure, early adoption of digital construction tools, and strong government support through mandates like those from the U.S. General Services Administration requiring BIM for public projects. The region benefits from a mature construction sector focused on sustainability and efficiency, with investments in smart cities and infrastructure upgrades further accelerating BIM usage. Dominating country: The United States, accounting for over 65% of the regional market, leads due to its robust ecosystem of tech innovators, extensive R&D, and federal funding for digital transformation in sectors like transportation and healthcare, where BIM reduces project timelines by up to 20% and enhances collaboration among stakeholders.

Europe is a key player in the BIM market, supported by stringent environmental regulations and a focus on heritage preservation alongside modern infrastructure development. Countries like the UK have pioneered BIM mandates since 2016, extending to Level 3 for advanced data exchanges, while EU-wide initiatives promote standardization via ISO 19650. This fosters innovation in green building practices and cross-border projects. Dominating country: The United Kingdom, with around 25% regional share, excels through its National Digital Twin program and investments in sustainable construction, enabling cost savings of 15-25% on projects and positioning it as a hub for BIM expertise and software development.

Asia Pacific is the fastest-growing region for BIM, fueled by rapid urbanization, massive infrastructure investments, and government pushes for digitalization in construction. Initiatives like China's "Made in China 2025" integrate BIM with smart manufacturing, while India's Smart Cities Mission mandates BIM for urban planning. The region sees high adoption in high-rise and transportation projects to manage complexity and resources efficiently. Dominating country: China, capturing over 30% of the regional market, dominates through state-backed infrastructure megaprojects like the Belt and Road Initiative, where BIM optimizes design and execution, reducing waste and supporting a 15% annual growth in construction output.

Latin America is emerging in the BIM market, driven by increasing foreign investments in infrastructure and efforts to modernize construction practices amid economic recovery. Governments are adopting BIM to improve project transparency and efficiency, with Brazil leading in public-private partnerships for urban development. Challenges like skill gaps are being addressed through training programs. Dominating country: Brazil, with about 40% regional share, leads via mandates for BIM in federal projects, enhancing coordination in sectors like energy and transportation, and achieving up to 10% cost reductions while attracting international collaborations.

The Middle East & Africa region is witnessing steady BIM growth, supported by oil-funded diversification into non-energy sectors and smart city developments like NEOM in Saudi Arabia. BIM aids in managing extreme climates and large-scale projects, with UAE's mandates accelerating adoption. Africa focuses on affordable housing and infrastructure. Dominating country: Saudi Arabia, holding around 35% regional share, dominates through Vision 2030 initiatives, where BIM streamlines megaprojects, improves sustainability, and integrates with technologies like AI for predictive maintenance, driving a 12% CAGR in construction tech investments.

Competitive Analysis

The global BIM market is dominated by players:

- Autodesk Inc.

- Bentley Systems, Inc.

- Trimble Inc.

- Nemetschek Group

- Dassault Systèmes

- AECOM

- Beck Technology Ltd.

- Asite Solutions Ltd.

- Hexagon AB

- Procore Technologies, Inc.

- And Others.

The global BIM market is segmented as follows:

By Component

- Software

- Services

By Deployment Mode

- On-Premises

- Cloud

By Project Lifecycle

- Pre-Construction

- Construction

- Operation

By Application

- Commercial

- Residential

- Industrial

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global BIM market is dominated by players:

- Autodesk Inc.

- Bentley Systems, Inc.

- Trimble Inc.

- Nemetschek Group

- Dassault Systèmes

- AECOM

- Beck Technology Ltd.

- Asite Solutions Ltd.

- Hexagon AB

- Procore Technologies, Inc.

- And Others.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors