![]()

Search Market Research Report

Brake Disc Market Size, Share Global Analysis Report, 2026-2034

Brake Disc Market Size, Share, Growth Analysis Report By Type (Cast Iron, Carbon Ceramic, and Others), By Vehicle Type (Passenger Cars, Commercial Vehicles, Motorcycles and Scooters, and Others), By Sales Channel (OEM, Aftermarket, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

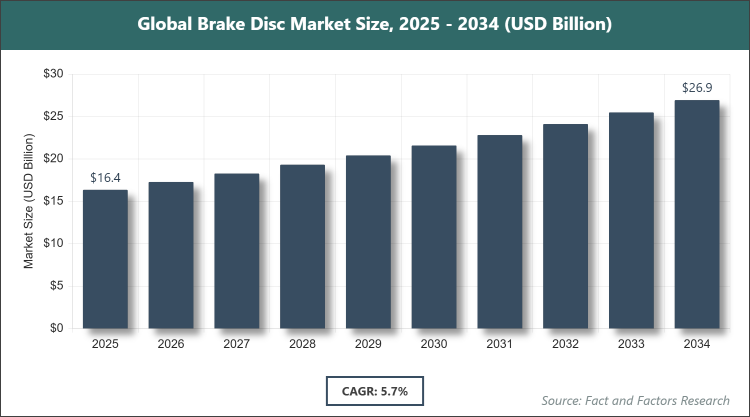

[235+ Pages Report] According to Facts & Factors, the global brake disc market size was estimated at USD 16.36 billion in 2025 and is expected to reach USD 26.24 billion by the end of 2034. The Brake Disc industry is anticipated to grow by a CAGR of 5.7% between 2026 and 2034. The Brake Disc Market is driven by increasing automotive production and stringent safety regulations worldwide.

Market Overview

Market Overview

The brake disc market refers to the sector involved in the manufacturing, distribution, and utilization of brake discs, which are essential components in vehicular braking systems designed to slow down or stop vehicles by converting kinetic energy into heat through friction with brake pads, primarily used in automobiles to ensure safety and performance across various vehicle types. This market includes a range of materials and designs tailored to different applications, involving key participants such as automotive manufacturers, suppliers, and aftermarket service providers focused on enhancing durability, efficiency, and compliance with evolving regulatory standards in global transportation.

Key Insights

- As per the analysis shared by our research analyst, the Brake Disc market is expected to grow at a CAGR of 5.7% during the forecast period of 2026-2034.

- In terms of revenue, the Brake Disc market size was valued at about USD 16.36 billion in 2025 and is expected to reach USD 26.24 billion by 2034.

- The Brake Disc market is driven by increasing automotive production and stringent safety regulations worldwide.

- Based on the type, the cast iron segment dominated the market with a share of 95% in 2025 due to its cost-effectiveness, excellent thermal conductivity, and durability in standard applications.

- Based on the vehicle type, the passenger cars segment dominated the market with a share of 60% in 2025 owing to high global sales volumes and emphasis on safety features in personal vehicles.

- Based on the sales channel, the OEM segment dominated the market with a share of 70% in 2025 as it integrates directly with vehicle assembly lines for new productions.

- Asia Pacific dominated the market with a share of 45% in 2025 due to massive vehicle manufacturing hubs in countries like China and India.

Growth Drivers

- Rising Automotive Production

The surge in global vehicle manufacturing, particularly in emerging economies, is a major driver, as it directly increases the demand for brake discs in new assemblies, supported by expanding middle-class populations and urbanization that boost car ownership. This growth is further propelled by investments in automotive infrastructure and supply chains.

Additionally, the shift towards electric and hybrid vehicles requires advanced braking systems, including regenerative braking compatible discs, fostering innovation and market expansion through R&D in lightweight materials.

- Stringent Safety Regulations

Government mandates for enhanced vehicle safety standards worldwide compel manufacturers to adopt high-performance brake discs, driving market growth by necessitating upgrades in braking efficiency and reliability. This includes regulations on emission reductions influencing brake design.

Moreover, consumer awareness of safety features influences purchasing decisions, encouraging OEMs to incorporate superior brake technologies, thereby sustaining demand and promoting technological advancements in the sector.

- Adoption of Electric Vehicles

The proliferation of EVs demands specialized brake discs for regenerative systems, propelling market growth as automakers transition to sustainable mobility solutions with lighter, more efficient components. This trend is amplified by incentives for green vehicles.

Furthermore, battery advancements and charging infrastructure development support EV uptake, indirectly boosting brake disc innovations tailored to unique EV braking patterns and weight distributions.

Restraints

- High Cost of Advanced Materials

The elevated prices of premium materials like carbon ceramic limit adoption in mass-market vehicles, restraining market growth in price-sensitive segments where cost outweighs performance benefits. This is particularly evident in developing regions.

Compounding this, manufacturing complexities for advanced discs increase production costs, deterring smaller players and slowing overall market penetration despite technological advantages.

- Competition from Drum Brakes

In certain commercial and low-cost vehicle segments, drum brakes remain preferred for their simplicity and lower maintenance, posing a restraint by capturing market share in applications where disc brakes are not essential.

Additionally, established supply chains for drum systems in heavy vehicles hinder the switch to discs, requiring significant investment in retrofitting and education.

Opportunities

- Aftermarket Expansion

Growing vehicle parc and aging fleets create opportunities in the aftermarket for replacement brake discs, as consumers seek affordable upgrades for safety and performance. This is supported by e-commerce platforms.

Such expansion allows for customization and premium offerings, tapping into enthusiast markets and fostering partnerships with service providers for broader reach.

- Technological Innovations

Developments in lightweight and eco-friendly brake discs offer opportunities to meet EV and sustainability demands, attracting investments in R&D for novel materials and designs.

Leveraging this involves collaborations with tech firms for smart braking integration, potentially opening new revenue streams in autonomous vehicle sectors.

Challenges

- Supply Chain Disruptions

Global supply chain vulnerabilities, including raw material shortages, challenge consistent production and delivery of brake discs, impacting market stability. This is exacerbated by geopolitical tensions.

Addressing this requires diversification of suppliers and local manufacturing, though it demands substantial upfront costs and logistical adjustments.

- Environmental Regulations

Strict rules on brake dust emissions necessitate redesigns, posing challenges in compliance while maintaining performance, affecting development timelines and costs.

Ongoing adaptations to evolving standards require continuous innovation, straining resources for smaller manufacturers in a competitive landscape.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 16.36 Billion |

Projected Market Size in 2034 |

USD 26.24 Billion |

CAGR Growth Rate |

5.7% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Brembo, Bosch, Continental, Akebono Brake Industry, ZF TRW, Aisin Seiki, Mando Corporation, Nissin Kogyo, Federal-Mogul, TEXTAR, Winhere, Kiriu, AC Delco, and Others. |

Key Segment |

By Type, By Vehicle Type, By Sales Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Brake Disc market is segmented by type, vehicle type, sales channel, and region.

Based on Type Segment, the brake disc market is divided into cast iron, carbon ceramic, and others. The most dominant segment is cast iron, leading the market owing to its affordability, robust heat dissipation properties, and widespread compatibility with various vehicle types, which drives the market by enabling mass production and meeting the demands of high-volume automotive manufacturing; the second most dominant is carbon ceramic, gaining prominence in premium and performance vehicles for its lightweight nature and superior resistance to fade under extreme conditions, contributing to market growth by catering to the expanding luxury and EV sectors where weight reduction enhances efficiency.

Based on Vehicle Type Segment, the brake disc market is divided into passenger cars, commercial vehicles, motorcycles and scooters, and others. The most dominant segment is passenger cars, commanding the largest share due to soaring global sales driven by urbanization and rising disposable incomes, propelling the market through integration of advanced safety features that require reliable brake discs; the second most dominant is commercial vehicles, essential for logistics and transportation industries, aiding market expansion by addressing the need for durable braking in heavy-duty applications amid growing e-commerce and freight demands.

Based on Sales Channel Segment, the brake disc market is divided into OEM, aftermarket, and others. The most dominant segment is OEM, dominating because of direct partnerships with automakers for new vehicle integrations, boosting the market via bulk orders and standardized quality in production lines; the second most dominant is aftermarket, supporting growth through replacements and upgrades for existing vehicles, driven by vehicle longevity and consumer preferences for customized performance enhancements.

Recent Developments

- In November 2023, Brembo introduced the CCM-R Plus disc, a new carbon ceramic model designed for high-performance applications, enhancing heat resistance and reducing weight for sports cars.

- In February 2025, Bosch launched next-generation coated discs that reduce particulate emissions by 20%, aligning with EU7 environmental standards and targeting eco-conscious markets.

- In March 2025, ZF Friedrichshafen expanded production of lightweight aluminum hybrid discs, increasing output by 18% to meet rising demand in electric vehicles.

- In April 2025, Brembo unveiled the GREENTELL brake disc with a novel coating technology that cuts brake dust emissions by up to 90%, preparing for stricter regulations.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific commands the brake disc market with China as the dominating country, where enormous automotive manufacturing capacity and export activities fuel demand for brake components, bolstered by government policies promoting vehicle safety and electric mobility that integrate advanced discs, while rapid urbanization increases passenger car ownership, supported by cost-effective local production that maintains competitive pricing and supply chain efficiency across the region.

North America follows prominently, led by the United States with its strong emphasis on innovation and regulatory compliance driving adoption of high-performance brake discs in luxury and EV segments, enhanced by robust aftermarket services and consumer focus on vehicle safety, where collaborations between OEMs and tech firms accelerate developments in smart braking systems.

Europe maintains a significant position dominated by Germany, renowned for its automotive engineering prowess that prioritizes precision and sustainability in brake disc designs, influenced by stringent EU emissions and safety norms that encourage carbon ceramic usage, alongside a mature market for premium vehicles fostering continuous upgrades and exports.

Latin America is growing steadily with Brazil at the forefront, where expanding commercial vehicle fleets for agriculture and logistics require durable brake solutions, aided by improving infrastructure and foreign investments that boost local assembly, addressing regional challenges like varied terrains through adapted disc technologies.

The Middle East & Africa region progresses with South Africa leading, focusing on mining and transport sectors needing reliable heavy-duty brake discs, supported by international trade agreements enhancing access to advanced components, while urban development increases demand for passenger vehicle safety features in emerging markets.

Competitive Analysis

The global Brake Disc market is dominated by players:

- Brembo

- Bosch

- Continental

- Akebono Brake Industry

- ZF TRW

- Aisin Seiki

- Mando Corporation

- Nissin Kogyo

- Federal-Mogul

- TEXTAR

- Winhere

- Kiriu

- AC Delco

The global Brake Disc market is segmented as follows:

By Type

- Cast Iron

- Carbon Ceramic

- Others

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Motorcycles and Scooters

- Others

By Sales Channel

- OEM

- Aftermarket

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Brake Disc market is dominated by players:

Brembo

Bosch

Continental

Akebono Brake Industry

ZF TRW

Aisin Seiki

Mando Corporation

Nissin Kogyo

Federal-Mogul

TEXTAR

Winhere

Kiriu

AC Delco

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors