![]()

Search Market Research Report

Blenders and Juicers Market Size, Share Global Analysis Report, 2026-2034

Blenders and Juicers Market Size, Share, Growth Analysis Report By Type (Blenders, Juicers), By Application (Beverage Preparation, Food Processing, and Others), By End User (Residential, Commercial), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

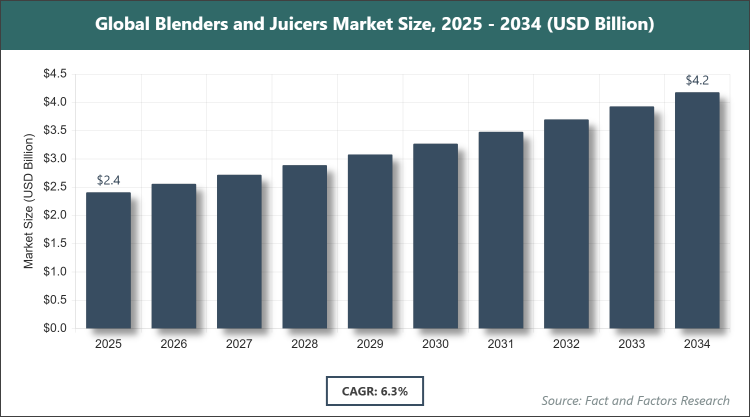

[225 Pages Report] According to Facts & Factors, the global blenders and juicers market size was estimated at USD 2.41 billion in 2025 and is expected to reach USD 3.43 billion by the end of 2034. The Blenders and Juicers industry is anticipated to grow by a CAGR of 6.3% between 2026 and 2034. The Blenders and Juicers Market is driven by rising health consciousness and demand for convenient home beverage preparation.

Market Overview

Market Overview

The blenders and juicers market comprises the manufacturing, distribution, and consumption of kitchen appliances designed for processing fruits, vegetables, and other ingredients into smoothies, juices, and purees, catering to health-focused consumers seeking nutrient-rich beverages and meals, while incorporating features like variable speeds, durability, and ease of cleaning to enhance user experience in both household and commercial settings. This market involves innovation in design and technology to address diverse culinary needs, promoting wellness through fresh, homemade preparations that align with global trends towards healthier lifestyles and sustainable eating habits.

Key Insights

- As per the analysis shared by our research analyst, the Blenders and Juicers market is expected to grow at a CAGR of 6.3% during the forecast period of 2026-2034.

- In terms of revenue, the Blenders and Juicers market size was valued at about USD 2.41 billion in 2025 and is expected to reach USD 3.43 billion by 2034.

- The Blenders and Juicers market is driven by rising health consciousness and demand for convenient home beverage preparation.

- Based on the type, the Blenders segment dominated the market with a share of 55% in 2025 due to their versatility in handling a variety of tasks beyond juicing, such as blending smoothies and soups, appealing to a broader consumer base.

- Based on the application, the Beverage Preparation segment dominated the market with a share of 60% in 2025 owing to increasing consumer preference for fresh juices and smoothies as part of daily health routines.

- Based on the end user, the Residential segment dominated the market with a share of 70% in 2025 because of growing home cooking trends and personal health management among households.

- Based on the distribution channel, the Online Retail segment dominated the market with a share of 45% in 2025 as e-commerce platforms offer convenience, variety, and competitive pricing to consumers.

- Asia Pacific dominated the market with a share of 40% in 2025 due to rapid urbanization, rising disposable incomes, and expanding middle-class populations, driving demand for kitchen appliances.

Growth Drivers

- Increasing Health Awareness

The surge in consumer focus on wellness and nutrition is propelling demand for blenders and juicers, as individuals seek appliances that facilitate the preparation of fresh, nutrient-packed beverages and meals at home, supported by global health campaigns and dietary shifts towards plant-based options. This driver is further amplified by social media influencers promoting smoothie recipes and detox plans.

Additionally, advancements in appliance features like nutrient extraction technology enhance appeal, encouraging upgrades and attracting new users in emerging markets where health education is expanding.

- Technological Innovations

Development of smart blenders with app connectivity and automated settings is driving market growth by offering convenience and customization, appealing to tech-savvy consumers who value efficiency in kitchen tasks. This includes energy-efficient models and multi-functional designs.

Moreover, integration of AI for recipe suggestions and voice control is fostering premium product adoption, boosting sales through differentiated offerings in competitive retail environments.

- Rising Disposable Incomes

Economic growth in developing regions is enabling more households to invest in modern kitchen appliances, with blenders and juicers seen as essential for convenient meal prep amid busy lifestyles. This is complemented by urbanization trends.

Furthermore, promotional strategies and financing options are making products accessible, sustaining demand across diverse income segments and regions.

Restraints

- High Product Costs

Premium pricing of advanced models limits accessibility for price-sensitive consumers in emerging markets, hindering widespread adoption despite interest in health benefits. This is exacerbated by economic fluctuations.

Strategies like entry-level variants and discounts are needed to broaden reach, though they may impact profit margins.

- Maintenance and Durability Issues

Concerns over cleaning difficulties and part wear reduce repeat purchases, as users seek low-maintenance options in fast-paced lives. This restraint affects brand loyalty.

Innovations in self-cleaning features aim to address this, requiring R&D investments to improve user satisfaction.

Opportunities

- Expansion in Emerging Markets

Growing middle-class populations in Asia and Latin America present untapped potential for affordable, compact models tailored to local preferences. This aligns with increasing urbanization.

Partnerships with local retailers can accelerate penetration, unlocking new revenue streams.

- Eco-Friendly Product Development

Demand for sustainable materials and energy-efficient designs offers differentiation, attracting environmentally conscious buyers. This includes recyclable components.

Certifications and green marketing can enhance brand image, driving premium sales.

Challenges

- Intense Market Competition

Numerous brands vying for share lead to price wars and innovation pressures, challenging smaller players to compete with established giants. This requires strategic positioning.

Diversification and niche focusing are essential for survival in saturated segments.

- Supply Chain Disruptions

Global events affecting raw materials and logistics increase costs and delay deliveries, impacting availability. This demands resilient sourcing.

Building local supply networks can mitigate risks, though initial setup is costly.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 2.41 Billion |

Projected Market Size in 2034 |

USD 3.43 Billion |

CAGR Growth Rate |

6.3% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Omega, Breville, Oster (Sunbeam), Hurom, Braun, Cuisinart, Kuvings, Philips, Panasonic, Electrolux, Joyoung, Midea, Supor, Donlim (Guangdong Xinbao), SKG, and Others. |

Key Segment |

By Type, By Application, By End User, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Blenders and Juicers market is segmented by type, application, end user, distribution channel, and region.

Based on Type Segment, the blenders and juicers market is divided into Blenders and Juicers. The most dominant segment is Blenders, holding the largest share due to their multi-functional capabilities for blending, pureeing, and crushing, which cater to a wide range of recipes beyond juicing, driving market growth by appealing to versatile home cooks and commercial users; the second most dominant is Juicers, favored for specialized nutrient extraction from fruits and vegetables, contributing to expansion through health-focused trends and demand for fresh juices.

Based on Application Segment, the blenders and juicers market is divided into Beverage Preparation, Food Processing, and others. The most dominant segment is Beverage Preparation, leading because of the rising popularity of smoothies and juices as healthy alternatives to sugary drinks, propelling growth via consumer wellness initiatives; the second most dominant is Food Processing, used for sauces and purees, supporting market drive in culinary applications.

Based on End User Segment, the blenders and juicers market is divided into Residential and Commercial. The most dominant segment is Residential, commanding top position owing to home-based health routines and cooking trends, boosting overall growth through personal use; the second most dominant is Commercial, in cafes and restaurants for efficient preparation, aiding expansion in hospitality.

Based on Distribution Channel Segment, the blenders and juicers market is divided into supermarkets/hypermarkets, specialty stores, online retail, and others. The most dominant segment is Online Retail, dominating due to convenience and wide selection, driving growth via the e-commerce boom; the second most dominant is Supermarkets/Hypermarkets, offering hands-on demos, contributing to accessibility.

Recent Developments

- In March 2025, Crompton introduced the Fresh Mix Ultra juicer, a 500W appliance with dual modes for fruits and vegetables, enhancing efficiency for home users.

- In February 2025, Yuone Lifestyle launched the Gallery 1000 and Gallery 2000 portable blender juicers, targeting on-the-go consumers with compact designs for gyms and offices.

- In September 2025, NutriBullet announced a high-speed, co-branded collection with McLaren F1, featuring Ultra, Pro 900, and Portable models with premium design elements.

- In May 2025, NutriBullet launched a limited-edition co-branded blender collection with McLaren, incorporating papaya accents for a sporty aesthetic.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific leads the blenders and juicers market, with China as the dominating country, where rapid urbanization and a burgeoning middle class fuel demand for affordable kitchen appliances, supported by local manufacturing that keeps prices competitive, while health trends like smoothie consumption in urban youth drive adoption, alongside e-commerce platforms expanding reach to rural areas for diverse product options.

North America follows strongly, dominated by the United States, benefiting from high health awareness and premium product preferences in fitness-oriented lifestyles, with robust retail networks and innovations like smart features catering to busy professionals, while cultural emphasis on fresh diets boosts usage in households and cafes.

Europe maintains a significant share, led by Germany, emphasizing quality and energy-efficient models aligned with sustainability goals, with mature markets favoring multifunctional appliances for home cooking, supported by regulatory pushes for healthy eating and strong brand presence in specialty stores.

Latin America shows growth potential, with Brazil as the key country, driven by tropical fruit abundance encouraging juice preparation, alongside rising incomes enabling appliance purchases, with local festivals and health campaigns promoting usage in vibrant food cultures.

The Middle East & Africa region is emerging, dominated by South Africa, where increasing urbanization spurs demand for convenient kitchen tools, with imports of affordable models meeting needs in growing households, aided by awareness programs on nutrition and expanding retail infrastructure.

Competitive Analysis

The global Blenders and Juicers market is dominated by players:

- Omega

- Breville

- Oster (Sunbeam)

- Hurom

- Braun

- Cuisinart

- Kuvings

- Philips

- Panasonic

- Electrolux

- Joyoung

- Midea

- Supor

- Donlim (Guangdong Xinbao)

- SKG

The global Blenders and Juicers market is segmented as follows:

By Type

- Blenders

- Juicers

By Application

- Beverage Preparation

- Food Processing

- Others

By End User

- Residential

- Commercial

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail

- Others

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Blenders and Juicers market is dominated by players:

Omega

Breville

Oster (Sunbeam)

Hurom

Braun

Cuisinart

Kuvings

Philips

Panasonic

Electrolux

Joyoung

Midea

Supor

Donlim (Guangdong Xinbao)

SKG

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors