![]()

Search Market Research Report

Automotive Water Pump Market Size, Share Global Analysis Report, 2026-2034

Automotive Water Pump Market Size, Share, Growth Analysis Report By Type (Mechanical Water Pumps, Electric Water Pumps), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), By Distribution Channel (OEM, Aftermarket), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

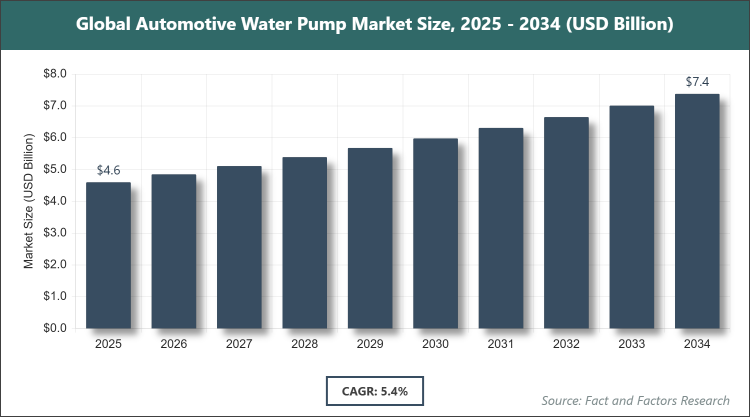

[228+ Pages Report] According to Facts & Factors, the global Automotive Water Pump market size was estimated at USD 4.6 billion in 2025 and is expected to reach USD 7.4 billion by the end of 2034. The Automotive Water Pump industry is anticipated to grow by a CAGR of 5.4% between 2026 and 2034. The Automotive Water Pump Market is driven by increasing vehicle production and the shift towards electric and hybrid vehicles requiring advanced cooling systems.

Market Overview

Market Overview

The automotive water pump market refers to the sector involved in the design, manufacturing, and supply of pumps that circulate coolant fluids within vehicle engines and thermal management systems. These pumps play a critical role in regulating engine temperature by facilitating the flow of coolant to dissipate heat generated during operation, thereby enhancing engine performance, longevity, and fuel efficiency. Traditionally associated with internal combustion engines, the market now extends to hybrid and electric vehicles where pumps support battery cooling and other thermal needs, adapting to evolving automotive technologies that prioritize energy efficiency and reduced emissions.

Key Insights

- As per the analysis shared by our research analyst, the global Automotive Water Pump market is estimated to grow annually at a CAGR of around 5.4% over the forecast period (2026-2034).

- In terms of revenue, the global Automotive Water Pump market size was valued at around USD 4.6 billion in 2025 and is projected to reach USD 7.4 billion by 2034.

- The market is driven by rising vehicle electrification, stringent emission regulations, and advancements in pump technology for better efficiency.

- Based on the Type, the Mechanical Water Pumps segment dominated with a 70% share, as they are widely used in conventional internal combustion engine vehicles due to their cost-effectiveness and reliability in high-volume production.

- Based on the Vehicle Type, the Passenger Cars segment dominated with a 65% share, owing to the sheer volume of passenger vehicle sales globally and the integration of water pumps in both traditional and electrified models.

- Based on the Distribution Channel, the OEM segment dominated with a 75% share, driven by direct integration into new vehicle assemblies and long-term supplier contracts with automakers.

- Based on region, Asia Pacific dominated with a 45% share, attributed to high automotive manufacturing output in countries like China and India, supported by low production costs and expanding EV infrastructure.

Growth Drivers

- Increasing Adoption of Electric and Hybrid Vehicles

The surge in electric and hybrid vehicle adoption is a primary growth driver for the automotive water pump market, as these vehicles require advanced thermal management systems to cool batteries, motors, and power electronics. Electric water pumps, in particular, offer precise control over coolant flow, improving energy efficiency and extending component life, which aligns with global efforts to reduce carbon emissions and enhance vehicle range.

This trend is further amplified by government incentives and regulations promoting clean mobility, leading to higher demand for innovative pump solutions that integrate seamlessly with electrified powertrains. As automakers scale up EV production, the need for reliable, high-performance water pumps continues to rise, fostering market expansion across both OEM and aftermarket channels.

Restraints

- High Initial Costs of Electric Water Pumps

The elevated cost of electric water pumps compared to traditional mechanical ones acts as a significant restraint, particularly in price-sensitive markets and for entry-level vehicles. These pumps incorporate advanced electronics and materials, increasing manufacturing expenses and potentially deterring adoption in cost-constrained segments like compact cars in developing regions.

Additionally, the complexity of integrating electric pumps into existing vehicle architectures can lead to higher development and installation costs for automakers, slowing the transition from mechanical systems. This price barrier may limit market penetration in the short term, especially amid economic uncertainties and fluctuating raw material prices.

Opportunities

- Technological Advancements in Pump Design

Innovations such as brushless DC motors and smart sensors in water pumps present substantial opportunities by enabling variable speed operation and predictive maintenance, which enhance overall vehicle efficiency. These advancements allow for better integration with autonomous and connected vehicle systems, opening new avenues in premium and luxury segments where performance optimization is key.

Moreover, the growing focus on sustainable materials and energy-efficient designs aligns with environmental goals, attracting investments from tech-savvy automakers. As R&D in this area accelerates, opportunities arise for suppliers to collaborate on next-generation solutions, potentially capturing share in emerging markets like autonomous electric fleets.

Challenges

- Supply Chain Disruptions and Raw Material Volatility

Global supply chain vulnerabilities, exacerbated by geopolitical tensions and pandemics, pose challenges by causing delays in component sourcing and increasing costs for key materials like rare earth elements used in electric pumps. This instability can disrupt production timelines and affect market availability, particularly for just-in-time manufacturing models prevalent in the automotive industry.

Furthermore, volatility in commodity prices adds financial pressure on manufacturers, potentially leading to higher end-user costs or reduced profit margins. Addressing these challenges requires diversified sourcing strategies and resilient logistics, but ongoing uncertainties may hinder steady market growth in the near term.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 4.6 Billion |

Projected Market Size in 2034 |

USD 7.4 Billion |

CAGR Growth Rate |

5.4% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Aisin Seiki, Continental AG, Denso Corporation, Robert Bosch GmbH, Mahle GmbH, Gates Corporation, Cardone Industries, Toyo Radiator Co., Ltd., Hella GmbH & Co. KGaA, and Others. |

Key Segment |

By Type, By Vehicle Type, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Automotive Water Pump market is segmented by Type, Vehicle Type, Distribution Channel, and region.

Based on Type Segment, the Automotive Water Pump market is divided into Mechanical Water Pumps and Electric Water Pumps. The Mechanical Water Pumps segment emerges as the most dominant, holding a significant market share due to its widespread use in traditional internal combustion engine vehicles, where it provides reliable, belt-driven operation without the need for additional electrical systems, making it cost-effective and easy to maintain. This dominance is driven by the continued prevalence of ICE vehicles in global fleets, particularly in emerging markets, where mechanical pumps help optimize engine cooling efficiently, contributing to overall market growth by supporting high-volume production and aftermarket replacements. The Electric Water Pumps segment is the second most dominant, gaining traction for its ability to offer on-demand coolant flow, reducing parasitic losses and improving fuel efficiency in hybrid and electric vehicles; its growth is propelled by the shift toward electrification, enabling precise thermal management that extends battery life and enhances vehicle performance, thus driving the market forward through innovation in sustainable automotive technologies.

Based on Vehicle Type Segment, the Automotive Water Pump market is divided into Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles. The Passenger Cars segment is the most dominant, capturing a large portion of the market owing to the high global sales volume of passenger vehicles, which require efficient cooling systems for both conventional and electrified powertrains, ensuring optimal engine and battery performance. This segment drives the market by fueling demand for compact, reliable pumps that align with consumer preferences for fuel-efficient and eco-friendly cars, supporting mass adoption and technological integration. The Light Commercial Vehicles segment ranks as the second most dominant, benefiting from the expanding logistics and delivery sectors, where durable pumps are essential for maintaining engine reliability under varying loads; it contributes to market growth by addressing the needs of urban mobility and e-commerce-driven transport, promoting advancements in pump efficiency for reduced downtime and operational costs.

Based on Distribution Channel Segment, the Automotive Water Pump market is divided into OEM and Aftermarket. The OEM segment dominates the market, as it involves direct supply to vehicle manufacturers for new assemblies, ensuring standardized quality and integration that meets stringent automotive standards. This dominance stems from long-term partnerships and bulk procurement, driving the market through consistent demand tied to global vehicle production rates and innovations in OEM-specific designs. The Aftermarket segment is the second most dominant, thriving on replacement needs for aging vehicles and customization options, where affordability and availability play key roles; it propels market expansion by catering to maintenance and upgrade demands, enhancing accessibility and supporting extended vehicle lifecycles in diverse regional markets.

Recent Developments

- In July 2024, Valeo showcased its advanced battery thermal regulation and heat pump technologies at IAA Transportation, highlighting innovations in coolant management for electric vehicles to improve efficiency and range.

- In June 2024, Rheinmetall secured a major contract from an international automaker to supply millions of electric coolant pumps, with power ratings from 50 to 2000 watts, emphasizing plug-and-play solutions for EV thermal systems.

- In April 2024, SHW AG presented its latest coolant pumps, including electrical main coolant pumps and motor oil pumps, at the Vienna Motor Symposium, focusing on enhanced performance for hybrid and electric applications.

- In March 2024, Schaeffler expanded its INA brand aftermarket range with water-cooled auxiliary electric pumps, targeting improved availability for repair shops and vehicle owners in the growing EV sector.

Regional Analysis

- Asia Pacific to Dominate the Global Market

The Asia Pacific region dominates the global automotive water pump market, driven by robust vehicle manufacturing hubs and rapid urbanization that boost demand for efficient cooling systems. China stands out as the dominating country, with its massive automotive production capacity and government push for electric vehicle adoption, fostering innovation in pump technologies to meet emission standards and support the world's largest EV market.

North America exhibits strong growth in the automotive water pump market, fueled by technological advancements and a shift toward sustainable mobility solutions. The United States leads as the dominating country, benefiting from a mature automotive industry, high EV penetration, and investments in R&D for advanced thermal management, which enhance pump efficiency and align with stringent environmental regulations.

Europe maintains a prominent position in the automotive water pump market, emphasizing eco-friendly innovations and regulatory compliance for reduced emissions. Germany emerges as the dominating country, renowned for its engineering prowess and leadership in premium vehicle manufacturing, where sophisticated water pumps are integral to hybrid and electric models, driving market progress through cutting-edge design and supply chain integration.

Latin America is experiencing gradual expansion in the automotive water pump market, supported by increasing vehicle ownership and infrastructure development. Brazil is the dominating country, with its growing automotive sector and focus on affordable, reliable vehicles that rely on cost-effective mechanical pumps, contributing to market growth amid economic recovery and export-oriented production.

The Middle East & Africa region shows emerging potential in the automotive water pump market, driven by oil-dependent economies diversifying into automotive assembly. South Africa leads as the dominating country, leveraging its established manufacturing base and aftermarket demand for durable pumps suited to harsh climates, aiding market development through regional trade and vehicle fleet modernization.

Competitive Analysis

The global Automotive Water Pump market is dominated by players:

- Aisin Seiki

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Mahle GmbH

- Gates Corporation

- Cardone Industries

- Toyo Radiator Co., Ltd.

- Hella GmbH & Co. KGaA

- And Others

The global Automotive Water Pump market is segmented as follows:

By Type

- Mechanical Water Pumps

- Electric Water Pumps

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Distribution Channel

- OEM

- Aftermarket

By Regional

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Automotive Water Pump market is dominated by players:

- Aisin Seiki

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Mahle GmbH

- Gates Corporation

- Cardone Industries

- Toyo Radiator Co., Ltd.

- Hella GmbH & Co. KGaA

- And Others

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors