![]()

Search Market Research Report

Automotive Interior Components/Accessories Market Size, Share Global Analysis Report, 2026-2034

Automotive Interior Components/Accessories Market Size, Share, Growth Analysis Report By Component (Seats, Infotainment Systems, Dashboard, Door Panels, Headliners, and Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

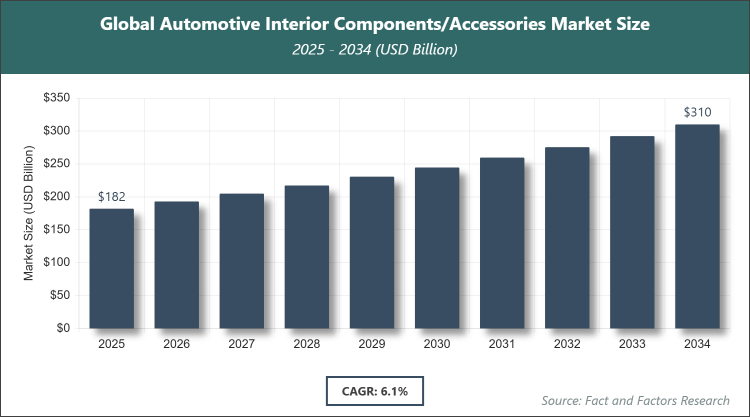

[225+ Pages Report] According to Facts & Factors, the global Automotive Interior Components/Accessories market size was estimated at USD 182 billion in 2025 and is expected to reach USD 310 billion by the end of 2034. The Automotive Interior Components/Accessories industry is anticipated to grow by a CAGR of 6.1% between 2026 and 2034. The Automotive Interior Components/Accessories Market is driven by increasing demand for enhanced vehicle comfort, technological advancements in infotainment and connectivity, and the rise of electric vehicles requiring innovative interior designs.

Market Overview

Market Overview

The Automotive Interior Components/Accessories Market encompasses a wide array of products and systems designed to enhance the functionality, aesthetics, comfort, and safety within vehicles. This market includes essential elements such as seating systems, dashboards, door panels, infotainment units, lighting, and various accessories that contribute to the overall interior environment of automobiles. It caters to both original equipment manufacturers (OEMs) and aftermarket needs, focusing on materials like leather, fabrics, plastics, and advanced composites that prioritize durability, ergonomics, and user experience. The market is influenced by evolving consumer preferences for personalized and tech-integrated spaces, alongside regulatory standards for sustainability and safety, making it a critical segment of the broader automotive industry that bridges engineering innovation with end-user satisfaction.

Key Insights

- As per the analysis shared by our research analyst, the global Automotive Interior Components/Accessories market is expected to grow at a CAGR of 6.1% during the forecast period.

- In terms of revenue, the global Automotive Interior Components/Accessories market size was valued at around USD 182 billion in 2025 and is projected to reach USD 310 billion, by 2034.

- The market is driven by rising consumer demand for advanced comfort features and integration of smart technologies in vehicles.

- Based on the component segment, the seats subsegment dominated the market with a share of 35%, as it plays a pivotal role in vehicle comfort, safety, and customization, driving higher adoption in premium and electric vehicles.

- Based on the vehicle type segment, the passenger cars subsegment dominated the market with a share of 70%, due to higher production volumes, consumer focus on personalization, and integration of luxury interiors in sedans and SUVs.

- Asia Pacific dominated the global market with a share of 45%, owing to its status as a major automotive manufacturing hub with cost-effective production and rapidly growing vehicle demand in emerging economies.

Growth Drivers

- Rising Demand for Enhanced Vehicle Comfort and Personalization

The increasing emphasis on vehicle interiors as extensions of personal living spaces has significantly boosted the market, with consumers seeking ergonomic designs, premium materials, and customizable features that improve the driving experience. This trend is particularly evident in the shift towards luxury and mid-range vehicles where interiors are differentiated through innovative seating and ambient lighting, fostering brand loyalty and higher sales margins for manufacturers.

Furthermore, advancements in material science have enabled lighter, more durable components that reduce vehicle weight while enhancing aesthetics and functionality, aligning with global sustainability goals and fuel efficiency standards. As urbanization accelerates, the need for comfortable commuting in congested traffic further amplifies this driver, encouraging OEMs to invest in R&D for adaptive interiors that cater to diverse user preferences.

- Integration of Advanced Technologies like Infotainment and Connectivity

The proliferation of smart devices and IoT has transformed automotive interiors into connected ecosystems, with infotainment systems, touchscreens, and voice-activated controls becoming standard features that enhance user engagement and safety. This integration not only meets the expectations of tech-savvy consumers but also opens avenues for over-the-air updates and seamless multimedia experiences, driving market expansion.

In addition, the rise of autonomous and semi-autonomous vehicles necessitates intuitive interior designs that prioritize passenger interaction and entertainment, prompting collaborations between tech firms and automakers. This technological convergence is reshaping supply chains, with suppliers focusing on modular components that support rapid innovation and scalability across vehicle models.

- Growth in Electric Vehicle Adoption Requiring Innovative Interiors

The global push towards electrification has created demand for interiors optimized for EVs, including space-efficient designs that accommodate larger batteries and advanced thermal management systems for occupant comfort. This shift encourages the use of sustainable materials and multifunctional components, aligning with environmental regulations and consumer eco-consciousness.

Moreover, EV manufacturers are leveraging interiors as key differentiators, incorporating features like augmented reality displays and adaptive seating to enhance range anxiety mitigation and overall appeal. This driver is supported by government incentives for green mobility, accelerating investments in EV-specific interior solutions that promise long-term market growth.

Restraints

- High Costs Associated with Advanced Materials and Technologies

The incorporation of premium materials such as genuine leather, carbon fiber, and high-tech electronics escalates production costs, posing challenges for mass-market adoption and profitability in price-sensitive segments. This restraint is compounded by fluctuating raw material prices, which can disrupt supply chains and lead to higher end-user prices, potentially slowing market penetration in developing regions.

Additionally, the need for specialized manufacturing processes and skilled labor further inflates expenses, limiting smaller players' ability to compete and innovate. As a result, OEMs may delay upgrades or opt for cost-cutting measures that compromise quality, hindering overall market progress amid economic uncertainties.

- Stringent Regulatory Standards on Safety and Emissions

Compliance with evolving global regulations for crash safety, fire resistance, and low-VOC emissions in interiors adds complexity and costs to product development, often requiring extensive testing and redesigns. This can delay time-to-market and increase R&D expenditures, particularly for suppliers navigating diverse regional standards.

Furthermore, non-compliance risks recalls and reputational damage, deterring investment in experimental features. While these regulations drive innovation in sustainable practices, they also create barriers for entry, consolidating the market among established players with robust compliance frameworks.

Opportunities

- Expansion in Emerging Markets with Rising Vehicle Ownership

Rapid economic growth in regions like Asia and Latin America is boosting vehicle sales, creating opportunities for affordable, localized interior components that cater to first-time buyers seeking value-added features. This expansion allows suppliers to tap into untapped demand through partnerships and localized production, enhancing market reach.

In parallel, infrastructure development and urbanization in these areas amplify the need for durable, climate-resilient interiors, opening doors for customized solutions that address specific environmental challenges and consumer preferences, fostering long-term growth.

- Advancements in Sustainable and Recyclable Materials

The shift towards eco-friendly materials like bio-based plastics and recycled fabrics presents opportunities for innovation, appealing to environmentally conscious consumers and aligning with corporate sustainability goals. This trend enables differentiation through green certifications and reduced carbon footprints, attracting premium pricing.

Moreover, collaborations with material scientists and startups can accelerate the development of cost-effective sustainable options, expanding applications in EVs and hybrid vehicles while meeting regulatory demands for circular economy practices.

Challenges

- Supply Chain Disruptions and Material Shortages

Global events such as geopolitical tensions and pandemics have highlighted vulnerabilities in supply chains, leading to shortages of key materials like semiconductors for infotainment systems, which delay production and increase costs. This challenge requires diversified sourcing strategies to mitigate risks.

Additionally, dependency on specific regions for raw materials exacerbates volatility, impacting delivery timelines and inventory management. Suppliers must invest in resilient logistics and alternative suppliers to maintain operational continuity amid unpredictable global dynamics.

- Intense Competition from Low-Cost Alternatives

The influx of inexpensive imports from low-wage countries intensifies price competition, pressuring established players to reduce margins or innovate rapidly to retain market share. This challenge is particularly acute in aftermarket segments where quality perceptions vary.

Furthermore, counterfeit products undermine brand trust and safety standards, necessitating robust anti-counterfeiting measures and consumer education. Balancing cost competitiveness with quality assurance remains a key hurdle in a fragmented market landscape.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 182 Billion |

Projected Market Size in 2034 |

USD 310 Billion |

CAGR Growth Rate |

6.1% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Adient Plc, Lear Corporation, Magna International Inc., Forvia (Faurecia), Yanfeng Automotive Interiors, Grupo Antolin, Hyundai Mobis, Toyota Boshoku Corporation, Samvardhana Motherson International Limited, and Others. |

Key Segment |

By Component, By Vehicle Type, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Automotive Interior Components/Accessories market is segmented by component, vehicle type, and region.

Based on Component Segment, the Automotive Interior Components/Accessories market is divided into seats, infotainment systems, dashboard, door panels, headliners, and others.

The seats segment emerges as the most dominant, capturing a significant portion due to its critical role in ensuring passenger comfort, safety, and ergonomic support, which directly influences vehicle purchase decisions and brand differentiation. As the second most dominant, the infotainment systems segment drives market growth by integrating advanced connectivity features like touchscreens and multimedia interfaces, catering to the rising demand for digital experiences that enhance entertainment and navigation, thereby boosting overall vehicle appeal and enabling premium pricing strategies in competitive automotive landscapes.

Based on Vehicle Type Segment, the Automotive Interior Components/Accessories market is divided into passenger cars, light commercial vehicles, heavy commercial vehicles.

Passenger cars represent the most dominant subsegment, propelled by high production volumes and consumer emphasis on luxurious, tech-enabled interiors that prioritize personalization and comfort for daily commuting and family use. Light commercial vehicles follow as the second most dominant, contributing to market expansion through the need for durable, functional interiors that support utility and efficiency in delivery and service applications, where modular designs and robust materials help optimize space and reduce maintenance costs, aligning with the growing e-commerce and logistics sectors.

Recent Developments

- In March 2025, FORVIA SE’s MATERI’ACT division announced the commercial launch of two sustainable material solutions, NAFILean-R NP47N and IniCycled-P VP32M ELV, aimed at enhancing eco-friendly instrument panels and promoting recycled plastics from end-of-life vehicles, marking a significant step towards circular economy practices in automotive interiors.

- In February 2025, Lear Corporation partnered with General Motors to integrate ComfortMax Seat technology, set for rollout in Q2 2025, focusing on advanced seating innovations that improve comfort and adaptability in next-generation vehicles.

- In June 2023, Samvardhana Motherson International Limited acquired an additional 30% stake in Youngshin Motherson Auto Tech Limited, strengthening its position in the auto components sector and expanding capabilities in interior manufacturing.

- In June 2023, Toyota Boshoku Corporation developed highly comfortable seats with flexible arrangements for the new Alphard and Vellfire models, emphasizing innovation in seating for enhanced passenger experience in premium minivans.

- In October 2022, Hyundai Mobis and Luxoft announced an agreement to market their new In-vehicle Infotainment (IVI) platform to independent automakers, fostering broader adoption of advanced digital interfaces in vehicle interiors.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region stands out as a powerhouse in the Automotive Interior Components/Accessories Market, primarily driven by its robust manufacturing ecosystem and rapid industrialization, with China emerging as the dominating country due to its massive production capacity and cost-effective labor force. This dominance is further bolstered by strong domestic demand from a burgeoning middle class seeking advanced vehicle features, alongside strategic investments in EV infrastructure that necessitate innovative interior solutions. The region's integrated supply chains and technological collaborations with global players enable swift adaptation to trends like smart connectivity, ensuring sustained leadership in export-oriented automotive production.

North America maintains a strong position through its focus on innovation and premium vehicle segments, where the United States leads as the dominating country with its emphasis on R&D in autonomous and connected technologies that enhance interior functionalities. The region's mature automotive industry benefits from consumer preferences for luxury and safety features, supported by stringent regulations that drive the adoption of high-quality materials. Close proximity to tech hubs facilitates partnerships that integrate cutting-edge infotainment and ergonomic designs, contributing to a competitive edge in high-value markets.

Europe excels in sustainability and design excellence, with Germany as the dominating country renowned for its engineering prowess and leadership in premium automotive brands that prioritize sophisticated interiors. The region's commitment to environmental standards promotes the use of eco-friendly materials and advanced manufacturing techniques, aligning with EU policies on emissions and recycling. This focus not only caters to discerning consumers but also positions Europe as a trendsetter in integrating aesthetics with functionality, influencing global standards.

Latin America is experiencing gradual growth fueled by increasing vehicle ownership and economic recovery, with Brazil dominating through its expanding automotive assembly plants and demand for affordable interior upgrades. The region's emphasis on cost-effective solutions suits emerging markets, where improvements in infrastructure and trade agreements enhance access to components, supporting local customization and aftermarket opportunities.

The Middle East & Africa region is poised for expansion driven by urbanization and oil-rich economies investing in diversified industries, with South Africa leading as the dominating country due to its established automotive sector and export capabilities. The focus here is on durable interiors suited to harsh climates, with growing interest in luxury vehicles among affluent populations, aided by foreign investments that bring technological know-how.

Competitive Analysis

The global Automotive Interior Components/Accessories market is dominated by players:

- Adient Plc

- Lear Corporation

- Magna International Inc.

- Forvia (Faurecia)

- Yanfeng Automotive Interiors

- Grupo Antolin

- Hyundai Mobis

- Toyota Boshoku Corporation

- Samvardhana Motherson International Limited

- And Others

The global Automotive Interior Components/Accessories market is segmented as follows:

By Component

- Seats

- Infotainment Systems

- Dashboard

- Door Panels

- Headliners

- Others

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Regional

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Automotive Interior Components/Accessories market is dominated by players:

- Adient Plc

- Lear Corporation

- Magna International Inc.

- Forvia (Faurecia)

- Yanfeng Automotive Interiors

- Grupo Antolin

- Hyundai Mobis

- Toyota Boshoku Corporation

- Samvardhana Motherson International Limited

- And Others

Frequently Asked Questions

Which are the major players leveraging the Automotive Interior Components/Accessories market growth?

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors