![]()

Search Market Research Report

Automotive Gear Shifter Market Size, Share Global Analysis Report, 2026-2034

Automotive Gear Shifter Market Size, Share, Growth Analysis Report By Component (Solenoid Actuator, CAN Module, Electronic Control Unit (ECU)), By System Type (Automatic, Mechanical), By Vehicle Type (Passenger Vehicle, Commercial Vehicle), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

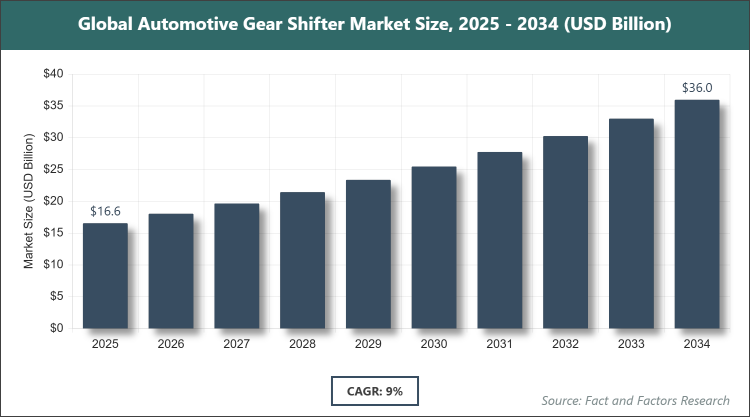

[220+ Pages Report] According to Facts & Factors, the global Automotive Gear Shifter market size was estimated at USD 16.56 billion in 2025 and is expected to reach USD 35.97 billion by the end of 2034. The Automotive Gear Shifter industry is anticipated to grow by a CAGR of 9.0% between 2026 and 2034. The Automotive Gear Shifter Market is driven by rising adoption of automatic transmissions and technological advancements in electronic gear shifters.

Market Overview

Market Overview

The automotive gear shifter market encompasses the design, manufacturing, and distribution of mechanisms used in vehicles to change gears, facilitating smooth transitions between different speed ratios in transmission systems. These shifters are integral components in both manual and automatic transmissions, enabling drivers to control vehicle speed and torque efficiently. The market includes various technologies such as mechanical linkages and advanced electronic systems that integrate with vehicle electronics for enhanced performance and user experience. It serves a wide range of vehicles, from passenger cars to commercial fleets, and is influenced by evolving automotive trends towards automation and electrification.

Key Insights

- As per the analysis shared by our research analyst, the global Automotive Gear Shifter market is estimated to grow annually at a CAGR of around 9.0% over the forecast period (2026-2034).

- In terms of revenue, the global Automotive Gear Shifter market size was valued at around USD 16.56 Billion in 2025 and is expected to reach USD 35.97 Billion by 2034.

- The Automotive Gear Shifter market is driven by rising adoption of automatic transmissions.

- Based on the component, the Solenoid Actuator segment dominated the market with a revenue share of 58.74% in 2023.

- The Solenoid Actuator is dominated due to its critical role in enabling precise and reliable gear shifting in automated transmission systems, which are increasingly preferred for their efficiency and integration with advanced driver assistance systems.

- Based on the system type, the Mechanical segment dominated the market with a revenue share of 60% in 2023.

- The Mechanical segment is dominated because of its widespread use in traditional vehicles, offering cost-effectiveness and familiarity to drivers, particularly in emerging markets where manual transmissions remain popular.

- Based on the vehicle type, the Passenger Vehicle segment dominated the market with a revenue share of 70% in 2023.

- The Passenger Vehicle segment is dominated owing to high consumer demand for personal mobility, coupled with the integration of advanced shifter technologies in sedans, SUVs, and crossovers to enhance driving comfort.

- Based on region, Asia Pacific dominated the market with a revenue share of 43% in 2023.

- Asia Pacific is dominated due to robust automotive manufacturing hubs, increasing vehicle production, and rising disposable incomes driving demand for advanced vehicles in countries like China and India.

Growth Drivers

- Rising Adoption of Automatic Transmissions

The shift towards automatic transmissions is a primary driver in the automotive gear shifter market, as consumers increasingly prefer vehicles that offer ease of use and reduced driver fatigue, especially in urban environments with heavy traffic. This trend is supported by advancements in transmission technology that improve fuel efficiency and performance, leading to broader integration of automatic shifters across various vehicle segments. Manufacturers are responding by developing more sophisticated gear shifter systems that seamlessly integrate with automatic transmissions, enhancing overall vehicle appeal and market penetration.

Furthermore, regulatory pressures for lower emissions and better fuel economy are accelerating the adoption of automatic systems, which often incorporate optimized gear shifting algorithms. This not only boosts market growth but also encourages innovation in shifter designs, such as paddle shifters and electronic controls, to meet evolving consumer expectations and compliance standards.

- Technological Advancements in Electronic Gear Shifters

Innovations in electronic gear shifters, including shift-by-wire technology, are propelling market expansion by providing precise control and integration with advanced driver assistance systems (ADAS). These electronic systems replace traditional mechanical linkages with sensors and actuators, offering smoother gear changes and enhanced safety features like automatic parking modes. As vehicles become more connected and autonomous, the demand for such advanced shifters rises, driving investments in research and development.

Additionally, the use of lightweight materials and smart electronics in gear shifters contributes to vehicle weight reduction and improved efficiency, aligning with global sustainability goals. This technological evolution not only attracts tech-savvy consumers but also opens new avenues for differentiation among automotive manufacturers, fostering competitive growth in the market.

- Increasing Demand for Passenger Vehicles

The surge in passenger vehicle sales, particularly SUVs and crossovers, is fueling the gear shifter market, as these vehicles often feature advanced transmission systems requiring sophisticated shifters. Rising urbanization and improving economic conditions in developing regions are boosting personal vehicle ownership, thereby increasing the need for comfortable and efficient gear shifting mechanisms. This demand is further amplified by consumer preferences for luxury features and seamless driving experiences.

Moreover, the integration of gear shifters with infotainment and connectivity systems in passenger vehicles enhances user interaction, making them more appealing. As automakers focus on enhancing vehicle interiors and ergonomics, the market for gear shifters in this segment continues to expand, supported by ongoing innovations and market diversification.

Restraints

- High Cost of Advanced Gear Shifter Systems

The elevated costs associated with developing and implementing advanced electronic gear shifters pose a significant restraint, limiting adoption in price-sensitive markets and entry-level vehicles. These systems require sophisticated components like sensors and ECUs, which increase manufacturing expenses and ultimately the vehicle price, deterring budget-conscious consumers. In regions with lower disposable incomes, this cost barrier slows market penetration and favors traditional mechanical alternatives.

Furthermore, the complexity of these advanced systems can lead to higher maintenance and repair costs, adding to the overall ownership burden. As automakers strive to balance innovation with affordability, this restraint challenges widespread adoption, particularly in emerging economies where cost remains a key purchasing factor.

- Shift Towards Electric Vehicles Reducing Multi-Gear Needs

The growing popularity of electric vehicles (EVs), which typically use single-speed transmissions without traditional gear shifters, is restraining demand for conventional multi-gear shifter systems. EVs rely on electric motors that provide instant torque across a wide range, eliminating the need for complex gear shifting mechanisms. This transition is accelerated by environmental regulations and consumer shifts towards sustainable mobility, impacting the market for traditional shifters.

Additionally, as EV adoption rises, investments in gear shifter R&D for internal combustion engines may decline, further constraining market growth. Manufacturers must adapt by developing EV-specific shifter interfaces, such as button-based or software-driven selectors, to mitigate this restraint and align with the electrification trend.

Opportunities

- Growth in Electric and Hybrid Vehicle Segments

The expansion of electric and hybrid vehicles presents opportunities for innovative gear shifter designs tailored to these platforms, such as cosmetic manual shifters or advanced electronic interfaces. As EV manufacturers seek to enhance driver engagement, simulated shifting mechanisms can differentiate products and attract enthusiasts. This niche allows for the development of unique shifter technologies that blend traditional feel with modern electric drivetrains.

Moreover, the integration of shifters with EV-specific features like regenerative braking modes opens new market avenues. With global EV sales projected to soar, this opportunity enables companies to diversify their portfolios and capture emerging demand in the sustainable automotive sector.

- Expansion in Emerging Markets

Rapid urbanization and rising middle-class populations in emerging markets offer opportunities for gear shifter manufacturers to tap into increasing vehicle demand. These regions are witnessing a surge in automotive production and sales, creating a fertile ground for affordable and reliable shifter systems. Partnerships with local manufacturers can facilitate market entry and customization to meet regional preferences.

Furthermore, infrastructure development and improving road networks in these areas boost the need for vehicles equipped with efficient gear shifters. By focusing on cost-effective innovations, companies can capitalize on this growth, expanding their global footprint and revenue streams.

Challenges

- Supply Chain Disruptions and Raw Material Uncertainties

Volatile supply chains and fluctuations in raw material availability pose challenges to gear shifter production, leading to delays and increased costs. Geopolitical tensions and global events can disrupt the sourcing of essential components like metals and electronics, affecting manufacturing timelines. This uncertainty requires robust supply chain strategies to maintain production stability.

In addition, dependency on specific suppliers for advanced materials heightens vulnerability. Companies must invest in diversification and local sourcing to overcome these challenges, ensuring consistent supply and mitigating risks to market operations.

- Evolving Regulatory Standards and Trade Relations

Stringent and varying regulatory standards across regions challenge compliance and product development in the gear shifter market. Changes in emission norms and safety regulations necessitate frequent adaptations, increasing R&D expenditures. International trade policies and tariffs can further complicate global operations and cost structures.

Moreover, shifting trade relationships and partnerships demand agile business strategies. Navigating these complexities requires ongoing monitoring and flexibility to sustain market presence and competitiveness.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 16.56 Billion |

Projected Market Size in 2034 |

USD 35.97 Billion |

CAGR Growth Rate |

9.0% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

ATSUMITEC Co., Ltd., BorgWarner Inc, Eaton, Ficosa Internacional SA, Kongsberg Automotive, Leopold Kostal GmbH & Co. KG, Lumax Industries, Orscheln Products, Stoneridge, ZF Friedrichshafen AG, and Others. |

Key Segment |

By Component, By System Type, By Vehicle Type, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Automotive Gear Shifter market is segmented by component, system type, vehicle type, and region.

Based on Component Segment, the Automotive Gear Shifter market is divided into Solenoid Actuator, CAN Module, and Electronic Control Unit (ECU). The most dominant segment is Solenoid Actuator, while the second most dominant is CAN Module. The Solenoid Actuator dominates due to its essential function in facilitating quick and accurate gear engagements in automatic and semi-automatic systems, driving market growth by enhancing vehicle responsiveness and integrating seamlessly with modern transmission technologies; its widespread adoption in both passenger and commercial vehicles helps propel overall market expansion through improved efficiency and reduced mechanical wear.

Based on System Type Segment, the Automotive Gear Shifter market is divided into Automatic and Mechanical. The most dominant segment is Mechanical, while the second most dominant is Automatic. The Mechanical segment dominates because of its reliability, lower cost, and established presence in a majority of vehicles worldwide, particularly in regions with high manual transmission preferences; it drives the market by providing durable solutions that cater to diverse driving conditions and support the transition towards more advanced systems.

Based on Vehicle Type Segment, the Automotive Gear Shifter market is divided into Passenger Vehicle and Commercial Vehicle. The most dominant segment is Passenger Vehicle, while the second most dominant is Commercial Vehicle. The Passenger Vehicle segment dominates owing to the high volume of personal car sales and the incorporation of user-friendly shifter designs that prioritize comfort and convenience; it contributes to market growth by aligning with consumer trends towards automated features and luxury enhancements in everyday transportation.

Recent Developments

- In June 2023, Toyota Motor Corporation advanced its plans for electric vehicles by introducing cosmetic manual transmission mimics, including a simulated stick shift, clutch pedal, and virtual engine revving sounds, aiming to provide EV drivers with a traditional driving experience while embracing electrification.

- In April 2023, BYD launched the BYD Seal sports sedan equipped with the KOSTAL Gear Shifter, which integrates buttons for additional comfort functions, enhancing the vehicle's ergonomic appeal and functionality in the competitive electric sedan market.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region is poised to lead the automotive gear shifter market, driven by its robust manufacturing infrastructure and high vehicle production volumes. Countries like China, as the dominating nation, benefit from extensive supply chains and technological investments, fostering innovation in shifter systems. The region's growing middle class and urbanization fuel demand for advanced vehicles, while government incentives for automotive exports strengthen its global position. Additionally, collaborations with international firms enhance local capabilities, ensuring sustained growth and market leadership.

North America exhibits strong potential in the automotive gear shifter market, with the United States as the dominating country due to its emphasis on technological integration and consumer preference for automatic transmissions. The region's focus on ADAS and electric vehicle adoption drives demand for sophisticated shifters. Robust R&D investments and a mature automotive industry support innovation, while stringent safety regulations encourage advanced system implementations. Economic stability and high disposable incomes further bolster market expansion in this area.

Europe maintains a significant share in the automotive gear shifter market, led by Germany as the dominating country renowned for its engineering prowess and premium vehicle manufacturing. The emphasis on sustainability and emission reductions propels the adoption of electronic shifters. Strong regulatory frameworks promote innovation, while collaborations among automakers enhance product development. The region's affluent consumer base demands high-quality, feature-rich vehicles, contributing to steady market growth.

Latin America is emerging in the automotive gear shifter market, with Brazil as the dominating country supported by its expanding automotive sector and increasing vehicle exports. Economic recovery and infrastructure improvements drive demand for reliable shifter systems. Local manufacturing initiatives reduce import dependencies, while rising urbanization boosts personal vehicle ownership. Partnerships with global players introduce advanced technologies, fostering gradual market development.

The Middle East & Africa region shows promising growth in the automotive gear shifter market, dominated by South Africa with its established automotive assembly plants and export focus. Oil-rich economies invest in vehicle fleets, increasing demand for commercial shifters. Improving infrastructure and economic diversification efforts support market entry. International trade agreements facilitate technology transfers, aiding regional advancement in automotive components.

Competitive Analysis

The global Automotive Gear Shifter market is dominated by players:

- ATSUMITEC Co., Ltd.

- BorgWarner Inc

- Eaton

- Ficosa Internacional SA

- Kongsberg Automotive

- Leopold Kostal GmbH & Co. KG

- Lumax Industries

- Orscheln Products

- Stoneridge

- ZF Friedrichshafen AG

The global Automotive Gear Shifter market is segmented as follows:

By Component

- Solenoid Actuator

- CAN Module

- Electronic Control Unit (ECU)

By System Type

- Automatic

- Mechanical

By Vehicle Type

- Passenger Vehicle

- Commercial Vehicle

By Regional

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Automotive Gear Shifter market is dominated by players:

- ATSUMITEC Co., Ltd.

- BorgWarner Inc

- Eaton

- Ficosa Internacional SA

- Kongsberg Automotive

- Leopold Kostal GmbH & Co. KG

- Lumax Industries

- Orscheln Products

- Stoneridge

- ZF Friedrichshafen AG

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors