![]()

Search Market Research Report

3D IC Market Size, Share Global Analysis Report, 2026-2034

3D IC Market Size, Share, Growth Analysis Report By Technology (Through-Silicon Via (TSV), 3D Fan-Out Packaging, 3D Wafer-Scale-Level Chip-Scale Packaging (WLCSP), Monolithic 3D ICs, and Others), By Component (3D Memory, LEDs, Sensors, Processors, and Others), By Application (Logic and Memory Integration, Imaging and Optoelectronics, MEMS and Sensors, LED Packaging, and Others), By End-user (Consumer Electronics, IT and Telecommunications, Automotive, Healthcare, Aerospace and Defense, Industrial, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

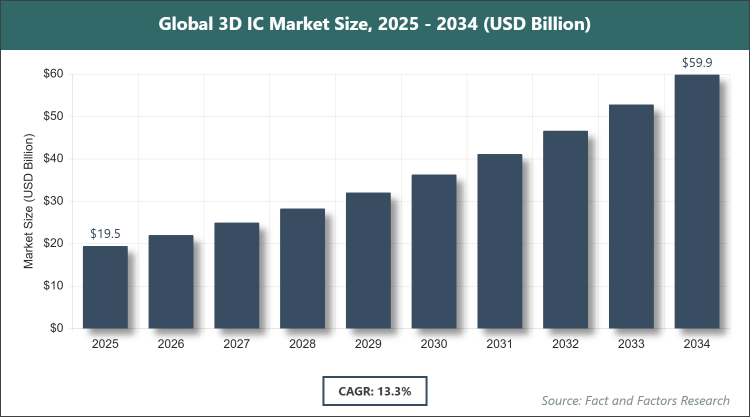

[220+ Pages Report] According to Facts & Factors, the global 3D IC market size was estimated at USD 19.46 billion in 2025 and is expected to reach USD 60.14 billion by the end of 2034. The 3D IC industry is anticipated to grow by a CAGR of 13.30% between 2026 and 2034. The 3D IC Market is driven by increasing demand for high-performance and miniaturized electronic devices.

Market Overview

Market Overview

The 3D IC market encompasses integrated circuits that stack silicon wafers or dies vertically, connected through vias, to achieve higher performance, reduced power consumption, and smaller form factors compared to traditional 2D ICs. This technology integrates multiple layers of active electronic components, enabling enhanced functionality in applications ranging from consumer devices to advanced computing systems without relying on traditional scaling limits.

Key Insights

-

As per the analysis shared by our research analyst, the global 3D IC market is estimated to grow annually at a CAGR of around 13.30% over the forecast period (2026-2034).

- In terms of revenue, the global 3D IC market size was valued at around USD 19.46 billion in 2025 and is projected to reach USD 60.14 billion by 2034.

- The market is driven by rising demand for high-performance computing, AI, and miniaturized electronics.

- Based on the technology, Through-Silicon Via (TSV) dominated with a 30.20% share due to its ability to enable high-speed connections, reduce latency, and improve power efficiency in stacked architectures.

- Based on the component, 3D Memory dominated with a significant share due to its role in enhancing data storage density and speed, crucial for AI and data center applications.

- Based on the application, Logic and Memory Integration dominated with a major share due to its efficiency in combining processing and storage for faster data access and reduced power use.

- Based on the end-user, Consumer Electronics dominated with a substantial share due to the need for compact, high-performance devices like smartphones and wearables.

- Based on region, North America dominated with a 37.90% share due to the presence of leading semiconductor firms and heavy investments in R&D for AI and computing technologies.

Growth Drivers

-

Increasing Demand for Advanced Consumer Electronics

The surge in consumer demand for compact, high-performance devices such as smartphones, tablets, and wearables is propelling the adoption of 3D ICs. These circuits allow for greater functionality in smaller spaces by stacking components vertically, addressing the limitations of 2D designs in terms of size and efficiency. This trend is further amplified by the integration of features like high-resolution displays and advanced sensors, which require enhanced processing power without increasing device footprint.

As electronics manufacturers strive to meet evolving user expectations for battery life and speed, 3D ICs provide a solution through improved interconnectivity and reduced signal delays. The ongoing miniaturization in the industry, coupled with the rise of IoT devices, ensures sustained growth in this area.

Restraints

- High Manufacturing Costs

The complex fabrication processes involved in 3D IC production, including precise alignment and bonding of layers, result in elevated costs that can limit widespread adoption. Specialized equipment and materials further contribute to these expenses, making it challenging for smaller players to enter the market.

Thermal management issues arise from the dense stacking, requiring additional investments in cooling solutions, which add to the overall cost burden. As a result, high upfront expenditures may slow down the transition from traditional ICs in cost-sensitive applications.

Opportunities

- Advancements in AI and High-Performance Computing

The rapid growth of AI applications and data centers creates opportunities for 3D ICs to deliver the necessary computational power and efficiency. Innovations in stacking technologies enable better integration of logic and memory, supporting complex AI models with lower latency.

Emerging markets in autonomous vehicles and edge computing also present avenues for expansion, as 3D ICs can handle intensive data processing in real-time environments. Collaborations between semiconductor firms and tech giants are likely to accelerate these developments.

Challenges

- Thermal Management Concerns

Heat dissipation in vertically stacked structures poses significant challenges, potentially leading to performance degradation or reliability issues if not addressed properly. The close proximity of components exacerbates thermal buildup, necessitating advanced materials and designs.

Supply chain complexities for specialized components and the need for standardized testing protocols further complicate deployment. Overcoming these hurdles requires ongoing research into new cooling techniques and materials.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 19.46 Billion |

Projected Market Size in 2034 |

USD 60.14 Billion |

CAGR Growth Rate |

13.30% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Samsung (South Korea), Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan), Advanced Micro Devices, Inc. (U.S.), Broadcom Inc. (U.S.), Micron Technology, Inc. (U.S.), NVIDIA Corporation (U.S.), Amkor Technology, Inc. (U.S.), ASE Technology Holding Co., Ltd. (Taiwan), Intel Corporation (U.S.), STMicroelectronics (Switzerland), Toshiba Corporation (Japan), Xilinx Inc. (U.S.), United Microelectronics Corp (Taiwan), and Others. |

Key Segment |

By Technology, By Component, By Application, By End-user, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The 3D IC market is segmented by technology, component, application, end-user, and region.

Based on Technology Segment, the 3D IC market is divided into Through-Silicon Via (TSV), 3D Fan-Out Packaging, 3D Wafer-Scale-Level Chip-Scale Packaging (WLCSP), Monolithic 3D ICs, and others. The most dominant segment is Through-Silicon Via (TSV), which excels in providing high-bandwidth interconnections and compact designs essential for advanced applications. The second most dominant is 3D Fan-Out Packaging, valued for its cost-effectiveness and ability to integrate diverse components without substrates, driving market growth through enhanced scalability and performance in consumer electronics.

Based on Component Segment, the 3D IC market is divided into 3D Memory, LEDs, Sensors, Processors, and others. The most dominant segment is 3D Memory, which leads due to its high density and speed, critical for data-intensive tasks like AI processing. The second most dominant is Processors, which benefit from vertical integration to achieve superior computing power and efficiency, fueling market expansion in high-performance sectors.

Based on Application Segment, the 3D IC market is divided into Logic and Memory Integration, Imaging and Optoelectronics, MEMS and Sensors, LED Packaging, and others. The most dominant segment is Logic and Memory Integration, prominent for reducing data bottlenecks and enhancing system speed in computing devices. The second most dominant is MEMS and Sensors, which leverage stacking for miniaturized, responsive systems in IoT and automotive applications, contributing to overall market propulsion.

Based on End-user Segment, the 3D IC market is divided into Consumer Electronics, IT and Telecommunications, Automotive, Healthcare, Aerospace and Defense, Industrial, and others. The most dominant segment is Consumer Electronics, driven by the need for slim, powerful gadgets with extended battery life. The second most dominant is IT and Telecommunications, where 3D ICs support faster data handling in networks and servers, advancing market growth through technological infrastructure demands.

Recent Developments

- In November 2023, Samsung Electronics unveiled its cutting-edge 3D chip packaging technology called SAINT with three variants: SAINT S, SAINT D, and SAINT L, aimed at enhancing performance in AI and high-computing applications.

- In June 2024, Ansys integrated NVIDIA Omniverse APIs into its platform, empowering 3D-IC designers to visualize physics simulations in real-time for improved semiconductor design in 5G/6G, IoT, AI, cloud computing, and autonomous vehicles.

- In April 2024, Synopsys strengthened its partnership with TSMC, unveiling a next-gen Photonic IC design flow to optimize power and performance in advanced computing systems.

Regional Analysis

- North America to dominate the global market

North America leads the 3D IC market, driven by its robust ecosystem of technology innovators and substantial R&D investments. The region benefits from leading companies like Intel and NVIDIA, which pioneer advancements in semiconductor design. High demand in data centers and AI applications further solidifies its position, with the United States as the dominant country due to its concentration of tech hubs and supportive policies.

Asia Pacific is experiencing rapid growth in the 3D IC market, fueled by extensive electronics manufacturing and government initiatives in semiconductor production. Countries like Taiwan and South Korea host major foundries such as TSMC and Samsung, enabling efficient scaling of advanced technologies. China emerges as the dominant country, leveraging its vast market and investments in domestic chip capabilities to meet surging demand in consumer and telecom sectors.

Europe's 3D IC market is advancing through strong automotive and industrial applications, with emphasis on energy-efficient solutions. Collaborative efforts among firms and research institutions drive innovation in packaging technologies. Germany stands out as the dominant country, supported by its engineering expertise and focus on automotive integration, enhancing vehicle electronics and smart manufacturing.

Latin America is emerging in the 3D IC market, primarily through growing telecommunications and consumer electronics sectors. Investments in infrastructure and partnerships with global players are accelerating adoption. Brazil is the dominant country, benefiting from its large economy and expanding tech industry, which demands advanced ICs for mobile and computing devices.

The Middle East & Africa region is gradually adopting 3D IC technologies, driven by diversification into high-tech industries and smart city projects. Collaborations with international firms aid in building local capabilities. The United Arab Emirates is the dominant country, leveraging its strategic investments in AI and semiconductors to foster innovation in data processing and telecommunications.

Competitive Analysis

The global 3D IC market is dominated by players:

- Samsung (South Korea)

- Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan)

- Advanced Micro Devices, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Micron Technology, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Amkor Technology, Inc. (U.S.)

- ASE Technology Holding Co., Ltd. (Taiwan)

- Intel Corporation (U.S.)

- STMicroelectronics (Switzerland)

- Toshiba Corporation (Japan)

- Xilinx Inc. (U.S.)

- United Microelectronics Corp (Taiwan)

The global 3D IC market is segmented as follows:

By Technology

- Through-Silicon Via (TSV)

- 3D Fan-Out Packaging

- 3D Wafer-Scale-Level Chip-Scale Packaging (WLCSP)

- Monolithic 3D ICs

- Others

By Component

- 3D Memory

- LEDs

- Sensors

- Processors

- Others

By Application

- Logic and Memory Integration

- Imaging and Optoelectronics

- MEMS and Sensors

- LED Packaging

- Others

By End-user

- Consumer Electronics

- IT and Telecommunications

- Automotive

- Healthcare

- Aerospace and Defense

- Industrial

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global 3D IC market is dominated by players:

- Samsung (South Korea)

- Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan)

- Advanced Micro Devices, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Micron Technology, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Amkor Technology, Inc. (U.S.)

- ASE Technology Holding Co., Ltd. (Taiwan)

- Intel Corporation (U.S.)

- STMicroelectronics (Switzerland)

- Toshiba Corporation (Japan)

- Xilinx Inc. (U.S.)

- United Microelectronics Corp (Taiwan)

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors