![]()

Search Market Research Report

2G, 3G and 4G Wireless Subscriptions, Spectrum Licensing, Ownership and Infrastructure Contracts Database Market Size, Share Global Analysis Report, 2026-2034

2G, 3G and 4G Wireless Subscriptions, Spectrum Licensing, Ownership and Infrastructure Contracts Database Market Size, Share, Growth Analysis Report By Data Type (Wireless Subscriptions, Spectrum Licensing, Ownership, Infrastructure Contracts, and Others), By Application (Market Analysis, Regulatory Compliance, Investment Planning, and Others), By End-User (Telecom Operators, Government Agencies, Consulting Firms, Research Institutions, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

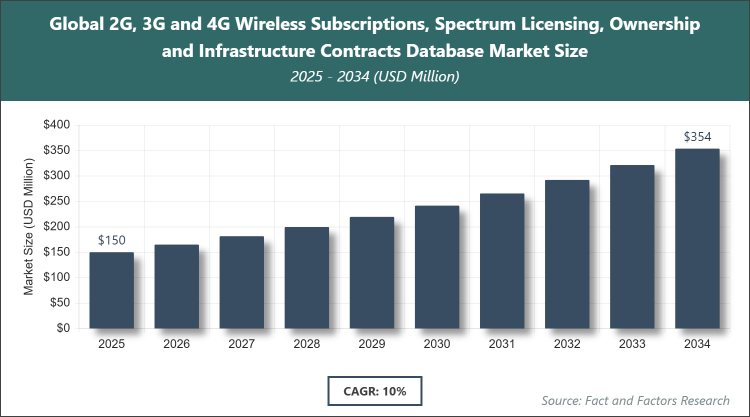

[230+ Pages Report] According to Facts & Factors, the global 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market size was estimated at USD 150 million in 2025 and is expected to reach USD 350 million by the end of 2034. The 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database industry is anticipated to grow by a CAGR of 10% between 2026 and 2034. The 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database Market is driven by increasing demand for comprehensive telecom data analytics.

Market Overview

Market Overview

The 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market encompasses specialized databases that compile and organize data related to wireless network subscriptions across legacy technologies, spectrum allocation and licensing details, ownership structures of telecom assets, and contractual agreements for infrastructure development and maintenance. These databases serve as critical tools for stakeholders in the telecommunications sector, providing structured information to support decision-making, regulatory compliance, and strategic planning without relying on quantitative metrics like market size or growth rates in this definitional overview.

Key Insights

- As per the analysis shared by our research analyst, the global 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market is estimated to grow annually at a CAGR of around 10% over the forecast period (2026-2034).

- In terms of revenue, the global 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market size was valued at around USD 150 million in 2025 and is projected to reach USD 350 million by 2034.

- The market is driven by rising regulatory requirements for transparent spectrum management and the need for accurate data in telecom mergers and acquisitions.

- Based on the data type, the spectrum licensing segment is dominating the market with a share of 35%, as it is essential for operators to track allocations amid global spectrum auctions and reallocations.

- Based on the application, the regulatory compliance segment is dominating the market with a share of 40%, due to stringent government mandates on data reporting and licensing transparency.

- Based on the end-user, the telecom operators segment is dominating the market with a share of 45%, owing to their reliance on such databases for network planning and competitive analysis.

- North America is expected to dominate the market with a share of 38%, attributed to advanced telecom infrastructure and high regulatory oversight in the region.

Growth Drivers

- Increasing Digital Transformation in Telecom Sector

The telecom industry's shift towards data-driven decision-making has amplified the demand for comprehensive databases that track legacy wireless technologies. As operators transition from 2G and 3G to 4G and beyond, these databases provide historical and current insights into subscription trends, helping in resource allocation and network optimization.

Moreover, the integration of AI and analytics tools with these databases enhances predictive capabilities, allowing stakeholders to forecast market shifts and investment needs more accurately.

Restraints

- High Costs of Data Maintenance and Updates

Maintaining up-to-date databases requires continuous monitoring of global telecom regulations and contracts, which incurs significant operational expenses. Smaller providers may struggle with these costs, limiting market accessibility.

Additionally, the complexity of harmonizing data from diverse international sources can lead to inaccuracies, further restraining widespread adoption.

Opportunities

- Expansion into Emerging Markets

Developing regions with growing telecom infrastructures present untapped opportunities for database providers to offer localized data solutions. Partnerships with local regulators can facilitate market entry and customization.

Furthermore, the rise of 5G preparations necessitates backward-compatible data on 4G networks, creating avenues for expanded database offerings.

Challenges

- Data Privacy and Security Concerns

Handling sensitive ownership and contract data raises privacy issues, especially under varying global regulations like GDPR. Breaches could erode trust and hinder market growth.

In addition, the rapid evolution of telecom standards challenges database providers to keep pace without compromising data integrity.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 150 Million |

Projected Market Size in 2034 |

USD 350 Million |

CAGR Growth Rate |

10% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Huawei Technologies Co., Ltd., Ericsson AB, Nokia Corporation (including Alcatel-Lucent / Motorola infrastructure), ZTE Corporation, Samsung Electronics Co., Ltd., Cisco Systems, Inc., Juniper Networks, Inc., Qualcomm, Inc., CommScope Holding Company, Inc., HUBER+SUHNER, Corning Incorporated, Fujitsu Ltd. |

Key Segment |

By Data Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market is segmented by data type, application, end-user, and region.

Based on Data Type Segment, the 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market is divided into wireless subscriptions, spectrum licensing, ownership, infrastructure contracts, and others. The spectrum licensing subsegment is the most dominant, holding 35% share, due to its critical role in enabling operators to navigate complex auction processes and ensure compliance, thereby driving market growth through informed bidding strategies. The wireless subscriptions subsegment is the second most dominant, with 25% share, as it aids in analyzing user trends and retention, supporting operators in optimizing service offerings and reducing churn.

Based on Application Segment, the 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market is divided into market analysis, regulatory compliance, investment planning, and others. The regulatory compliance subsegment dominates with 40% share, as it streamlines adherence to international standards, minimizing penalties and fostering trust, which propels overall market expansion. The market analysis subsegment follows as second dominant at 30%, empowering stakeholders with competitive intelligence to identify growth opportunities and strategic alliances.

Based on End-User Segment, the 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market is divided into telecom operators, government agencies, consulting firms, research institutions, and others. Telecom operators lead with 45% share, utilizing databases for operational efficiency and expansion planning, directly contributing to market vitality. Government agencies are the second dominant at 25%, leveraging data for policy formulation and spectrum management, enhancing regulatory frameworks that support industry stability.

Recent Developments

- In 2025, SNS Telecom launched an updated version of its Americas 2G, 3G & 4G database, incorporating real-time spectrum licensing data to assist operators in navigating post-auction landscapes.

- GSMA announced a collaboration with regulatory bodies in Europe to enhance its infrastructure contracts database, focusing on ownership transparency amid increasing mergers in the telecom sector.

- ResearchAndMarkets released a comprehensive report on global wireless subscriptions trends, integrating AI-driven analytics for predictive insights into 4G migration patterns.

Regional Analysis

- North America to Dominate the Global Market

North America's dominance stems from its robust telecom ecosystem and stringent regulatory environment, with the United States leading due to major operators like AT&T and Verizon relying on detailed databases for spectrum management and infrastructure planning. This region's advanced digital infrastructure supports seamless data integration, fostering innovation in database technologies.

Europe follows closely, driven by the European Union's emphasis on harmonized spectrum policies, where countries like Germany and the UK excel in utilizing databases for cross-border compliance and ownership tracking, enhancing market transparency.

Asia Pacific is rapidly growing, led by China and India, where exploding wireless subscriptions demand sophisticated databases for licensing and contracts, supporting massive network expansions in densely populated areas.

Latin America shows potential, with Brazil dominating through government initiatives on spectrum auctions, using databases to attract investments and improve infrastructure ownership clarity.

The Middle East & Africa, spearheaded by Saudi Arabia, leverages databases for regulatory reforms, focusing on ownership and contracts to build resilient telecom infrastructures amid regional digital transformations.

Competitive Analysis

The global 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market is dominated by players:

- Huawei Technologies Co., Ltd.

- Ericsson AB

- Nokia Corporation (including Alcatel-Lucent / Motorola infrastructure)

- ZTE Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems Inc.

- Juniper Networks Inc.

- Qualcomm Inc.

- CommScope Holding Company Inc.

- HUBER+SUHNER

- Corning Incorporated

- Fujitsu Ltd.

- And Others

The global 2G, 3G and 4G wireless subscriptions, spectrum licensing, ownership and infrastructure contracts database market is segmented as follows:

By Data Type

- Wireless Subscriptions

- Spectrum Licensing

- Ownership

- Infrastructure Contracts

- Others

By Application

- Market Analysis

- Regulatory Compliance

- Investment Planning

- Others

By End-User

- Telecom Operators

- Government Agencies

- Consulting Firms

- Research Institutions

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Huawei Technologies Co., Ltd.

- Ericsson AB

- Nokia Corporation (including Alcatel-Lucent / Motorola infrastructure)

- ZTE Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems Inc.

- Juniper Networks Inc.

- Qualcomm Inc.

- CommScope Holding Company Inc.

- HUBER+SUHNER

- Corning Incorporated

- Fujitsu Ltd.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors