![]()

Search Market Research Report

Specialty Optical Fibers Market Size, Share Global Analysis Report, 2026-2034

Specialty Optical Fibers Market Size, Share, Growth Analysis Report By Type (Polarization-Maintaining Fibers, Erbium-Doped Fibers, High-Power Laser Delivery Fibers, Photonic Crystal Fibers, Hollow-Core Fibers, and Others), By Application (Telecommunications, Medical & Biotechnology, Sensing & Measurement, Defense & Aerospace, Industrial, and Others), By End-User (Telecom Operators, Medical Device Manufacturers, Aerospace & Defense Contractors, Oil & Gas Companies, Research Institutes, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

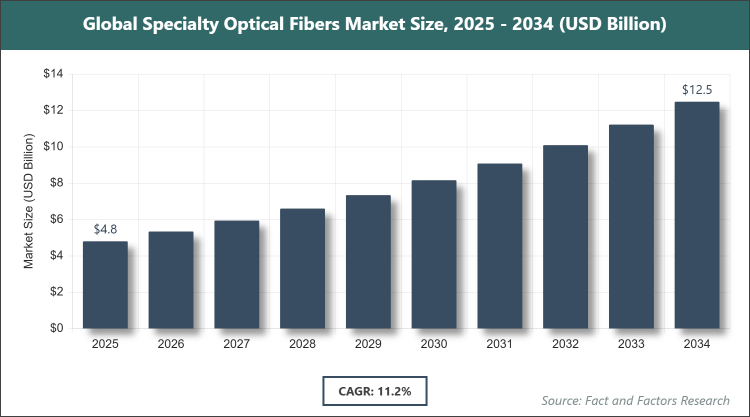

[235 + Pages Report] According to Facts & Factors, the global Specialty Optical Fibers market size was estimated at USD 4.8 billion in 2025 and is expected to reach USD 12.5 billion by the end of 2034. The Specialty Optical Fibers industry is anticipated to grow by a CAGR of 11.2% between 2026 and 2034. The Specialty Optical Fibers Market is driven by surging demand for high-performance fibers in 5G/6G infrastructure, medical imaging, industrial sensing, and high-power laser delivery applications.

Market Overview

Market Overview

The Specialty Optical Fibers market encompasses advanced optical fibers engineered with tailored core-cladding structures, dopants, coatings, and microstructures to deliver unique optical, mechanical, or environmental properties that standard telecom fibers cannot achieve. These fibers include polarization-maintaining, doped (erbium, ytterbium), large-mode-area, photonic crystal, hollow-core, and radiation-hardened variants designed for extreme conditions such as high power, high temperature, high pressure, or harsh chemical environments. They enable critical functions in long-haul coherent communications, medical endoscopy and laser surgery, distributed sensing in oil & gas and structural health monitoring, high-energy laser delivery, aerospace avionics, and quantum technologies, offering superior bandwidth, low loss, high power handling, or specific sensing capabilities that drive innovation across high-value industries.

Key Insights

- As per the analysis shared by our research analyst, the Specialty Optical Fibers market is estimated to grow annually at a CAGR of around 11.2% over the forecast period (2026-2034).

- In terms of revenue, the Specialty Optical Fibers market size was valued at around USD 4.8 billion in 2025 and is projected to reach USD 12.5 billion by 2034.

- The Specialty Optical Fibers Market is driven by the rapid expansion of 5G/6G networks and demand for advanced sensing solutions.

- Based on the Type, the Polarization-Maintaining Fibers segment dominated the market in 2025 with a share of 29% due to their essential role in coherent optical communication systems and high-precision sensing applications.

- Based on the Application, the Telecommunications segment dominated the market in 2025 with a share of 42%, owing to massive deployment in long-haul, submarine, and data-center interconnects requiring ultra-low loss and high bandwidth.

- Based on the End-User, the Telecom Operators segment dominated the market in 2025 with a share of 47% because global 5G rollout and upcoming 6G preparations demand specialty fibers for backbone and fronthaul networks.

- Asia Pacific dominated the global Specialty Optical Fibers market in 2025 with a share of 48% attributed to massive 5G infrastructure build-out in China and India, strong domestic manufacturing base, and government support for photonics and telecom industries.

Growth Drivers

- 5G/6G and Data Center Expansion

The global rollout of 5G and preparation for 6G networks require specialty fibers with ultra-low attenuation, high power handling, and polarization control to support higher data rates and longer transmission distances without repeaters.

Explosive growth in hyperscale data centers and cloud computing has increased demand for high-bandwidth, low-latency interconnect fibers that only specialty designs can deliver reliably.

Restraints

- High Manufacturing Complexity and Cost

Specialty fibers require precise doping, complex preform fabrication, and stringent quality control, resulting in significantly higher production costs than standard single-mode fibers and limiting adoption in price-sensitive applications.

Lengthy qualification cycles in the medical, defense, and oil & gas sectors delay revenue realization and increase working capital requirements for manufacturers.

Opportunities

- Medical, Sensing, and Quantum Technology Applications

Rising adoption in minimally invasive laser surgery, optical coherence tomography, and distributed acoustic sensing in oil & gas creates high-margin, high-growth niches for doped and photonic crystal fibers.

Emerging quantum communication and computing applications require ultra-low-loss hollow-core and polarization-maintaining fibers, opening entirely new premium market segments with substantial long-term potential.

Challenges

- Raw Material Supply and Geopolitical Risks

Dependence on high-purity silica, rare-earth dopants, and specialized chemicals exposes the industry to supply disruptions and price volatility, particularly for rare-earth elements dominated by limited suppliers.

Rapid technological evolution demands continuous heavy R&D investment, creating barriers for smaller players and intensifying competition among established manufacturers.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 4.8 Billion |

Projected Market Size in 2034 |

USD 12.5 Billion |

CAGR Growth Rate |

11.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Corning Incorporated, Prysmian Group, Furukawa Electric Co., Ltd., Yangtze Optical Fibre and Cable Joint Stock Limited Company (YOFC), Fujikura Ltd., Thorlabs, Inc., Coherent Corp., Sumitomo Electric Industries, Ltd., AFL (Subsidiary of Fujikura), Leoni AG, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Specialty Optical Fibers market is segmented by type, application, end-user, and region.

Based on Type Segment, the Specialty Optical Fibers market is divided into Polarization-Maintaining Fibers, Erbium-Doped Fibers, High-Power Laser Delivery Fibers, Photonic Crystal Fibers, Hollow-Core Fibers, and Others. The most dominant segment is Polarization-Maintaining Fibers, followed by Erbium-Doped Fibers. Polarization-Maintaining Fibers dominate because they are indispensable for coherent detection in long-haul telecom, fiber-optic gyroscopes in aerospace, and high-precision sensing systems, providing the critical performance that enables higher data rates and accuracy across the largest and fastest-growing applications, thereby driving the majority of market revenue and stimulating continuous innovation in coating and stress-rod technologies.

Based on Application Segment, the Specialty Optical Fibers market is divided into Telecommunications, Medical & Biotechnology, Sensing & Measurement, Defense & Aerospace, Industrial, and Others. The most dominant segment is Telecommunications, followed by Sensing & Measurement. Telecommunications leads the segment due to the enormous global investment in 5G/6G backbone and submarine cables that require ultra-low-loss and high-bandwidth specialty fibers, generating the highest volume demand and encouraging manufacturers to scale production while developing next-generation fibers that further reduce attenuation and increase capacity, fueling sustained market expansion.

Based on End-User Segment, the Specialty Optical Fibers market is divided into Telecom Operators, Medical Device Manufacturers, Aerospace & Defense Contractors, Oil & Gas Companies, Research Institutes, and Others. The most dominant segment is Telecom Operators, followed by Aerospace & Defense Contractors. Telecom Operators dominate because they are the primary procurers of long-haul and metro specialty fibers for network upgrades, controlling the largest budgets and driving standardization that benefits the entire supply chain while creating recurring demand through ongoing capacity expansions and technology refreshes.

Recent Developments

- In January 2025, Corning Incorporated introduced the SMF-28 Ultra 200 specialty fiber with record-low attenuation for next-generation submarine cable systems, securing multi-year supply agreements with leading operators.

- In April 2025, Thorlabs expanded its medical fiber portfolio with a new high-power erbium-doped fiber for advanced laser surgery platforms, gaining FDA clearance for clinical use.

- In July 2025, Yangtze Optical Fibre and Cable launched a commercial hollow-core photonic bandgap fiber for quantum communication pilots in China and Europe.

- In October 2025, Fujikura Ltd. unveiled a new radiation-hardened polarization-maintaining fiber qualified for space and defense applications, winning contracts with major satellite manufacturers.

- In February 2026, Prysmian Group announced the successful deployment of its latest sensing fiber in a 500 km offshore oil & gas monitoring project in the North Sea.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific leads the Specialty Optical Fibers market through its position as the global manufacturing powerhouse for optical components, massive 5G and data-center build-out in China and India, and strong government support for photonics and telecom infrastructure. The region benefits from vertically integrated supply chains that reduce costs and lead times, while rapid digital transformation across industries creates diverse demand for sensing, medical, and industrial fibers. Local innovation in photonic crystal and hollow-core technologies further strengthens its competitive edge. China dominates within Asia Pacific with the world’s largest telecom infrastructure investment, a dominant share of global fiber production capacity, state-backed R&D programs, and growing exports of high-end specialty fibers to international markets, enabling it to serve both domestic megaprojects and global demand.

North America maintains leadership in high-value and innovative segments of the Specialty Optical Fibers market, supported byan advanced R&D ecosystem, presence of major technology and defense companies, and strong demand from medical, aerospace, and quantum research communities. The region excels in developing next-generation fibers and benefits from robust venture funding for photonics startups. The United States dominates within North America through its concentration of leading specialty fiber manufacturers, NASA, and defense contracts, and early adoption of cutting-edge applications such as quantum networks and high-power laser systems.

Europe exhibits steady and technology-driven growth in the Specialty Optical Fibers market, fueled by ambitious 5G/6G targets, a strong medical device industry, and a focus on industrial sensing and structural health monitoring. The region leads in standardization and high-reliability fibers for harsh environments. Germany dominates within Europe with its world-class photonics research institutions, advanced manufacturing capabilities, and central role in supplying premium specialty fibers to automotive, aerospace, and energy sectors across the continent.

Latin America is experiencing emerging growth in the Specialty Optical Fibers market, supported by expanding telecom networks, oil & gas exploration in deepwater fields, and increasing medical device manufacturing. Brazil dominates the region through its large telecom market, offshore energy sector, and growing investment in fiber-based sensing solutions for infrastructure monitoring.

The Middle East & Africa region shows promising development in the Specialty Optical Fibers market, driven by smart-city initiatives, oil & gas digitalization, and telecom modernization programs. The United Arab Emirates dominates within the region through its ambitious digital transformation agenda, advanced data-center projects, and role as a regional hub for high-tech imports and innovation in photonics applications.

Competitive Analysis

The global Specialty Optical Fibers market is dominated by players:

- Corning Incorporated

- Prysmian Group

- Furukawa Electric Co., Ltd.

- Yangtze Optical Fibre and Cable Joint Stock Limited Company (YOFC)

- Fujikura Ltd.

- Thorlabs, Inc.

- Coherent Corp.

- Sumitomo Electric Industries, Ltd.

- AFL (Subsidiary of Fujikura)

- Leoni AG

The global Specialty Optical Fibers market is segmented as follows:

By Type

- Polarization-Maintaining Fibers

- Erbium-Doped Fibers

- High-Power Laser Delivery Fibers

- Photonic Crystal Fibers

- Hollow-Core Fibers

- Others

By Application

- Telecommunications

- Medical & Biotechnology

- Sensing & Measurement

- Defense & Aerospace

- Industrial

- Others

By End-User

- Telecom Operators

- Medical Device Manufacturers

- Aerospace & Defense Contractors

- Oil & Gas Companies

- Research Institutes

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Corning Incorporated

- Prysmian Group

- Furukawa Electric Co., Ltd.

- Yangtze Optical Fibre and Cable Joint Stock Limited Company (YOFC)

- Fujikura Ltd.

- Thorlabs, Inc.

- Coherent Corp.

- Sumitomo Electric Industries, Ltd.

- AFL (Subsidiary of Fujikura)

- Leoni AG

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors