![]()

Search Market Research Report

Rail Wheel Market Size, Share Global Analysis Report, 2026-2034

Rail Wheel Market Size, Share, Growth Analysis Report By Type (Forged Wheels, Cast Wheels, and Others), By Application (High-Speed Rail, Freight Wagons, Passenger Wagons, Locomotives, and Others), By End-User (OEM, Aftermarket, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

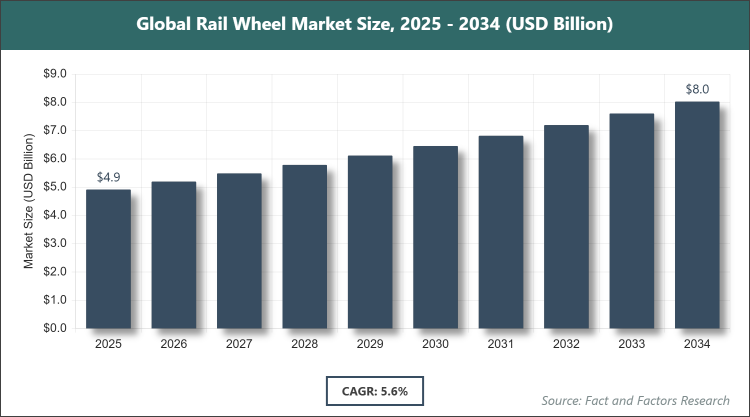

[232+ Pages Report] According to Facts & Factors, the global Rail Wheel market size was estimated at USD 4.92 billion in 2025 and is expected to reach USD 8.06 billion by the end of 2034. The Rail Wheel industry is anticipated to grow by a CAGR of 5.6% between 2026 and 2034. The Rail Wheel Market is driven by expanding global rail infrastructure and rising demand for efficient transportation systems.

Market Overview

Market Overview

The Rail Wheel market pertains to the production and supply of wheels used in railway vehicles, which are critical components designed to support loads, provide traction, and ensure smooth movement on tracks, typically manufactured from steel alloys to withstand high stress and wear. This market includes various types, such as forged and cast wheels, serving applications in freight, passenger, and high-speed rail systems, focusing on enhancing durability, safety, and performance without incorporating specific quantitative data.

Key Insights

- As per the analysis shared by our research analyst, the global Rail Wheel market is estimated to grow annually at a CAGR of around 5.6% over the forecast period (2026-2034).

- In terms of revenue, the global Rail Wheel market size was valued at around USD 4.92 billion in 2025 and is projected to reach USD 8.06 billion by 2034.

- The market is driven by increasing investments in rail infrastructure andthe adoption of high-speed trains globally.

- Based on the type, the forged wheels segment dominated with a 60% share due to their superior strength and fatigue resistance.

- Based on the application, the freight wagons segment dominated with a 45% share owing to high demand in logistics and heavy cargo transport.

- Based on the end-user, the OEM segment dominated with a 70% share because of direct integration in new rail vehicle manufacturing.

- Based on the region, Asia Pacific dominated with a 45% share attributed to rapid urbanization and extensive rail network expansions in China and India.

Growth Drivers

- Expanding Rail Infrastructure Investments

Governments worldwide are channeling funds into railway expansions to support economic growth and reduce road congestion, boosting demand for durable rail wheels that enhance operational efficiency. This driver is particularly evident in emerging economies where high-speed rail projects require advanced wheel technologies for safety and performance.

Additionally, technological advancements in wheel materials, such as alloy enhancements for better wear resistance, contribute to longer service life and lower maintenance costs, further propelling market growth through improved sustainability.

Restraints

- High Manufacturing and Material Costs

The elevated expenses associated with high-quality steel and precision forging processes limit market accessibility, especially for smaller manufacturers in developing regions. This restraint is compounded by fluctuating raw material prices influenced by global supply chain disruptions.

Moreover, stringent quality standards and certification requirements increase production timelines and costs, potentially delaying market entry for new players and affecting overall expansion.

Opportunities

- Adoption of Sustainable and Lightweight Materials

The shift toward eco-friendly materials and lightweight designs presents opportunities to reduce energy consumption in rail operations, aligning with global sustainability goals. This can attract investments in R&D for innovative composites.

Furthermore, emerging markets in Africa and Latin America offer untapped potential through infrastructure development, enabling partnerships for localized production and technology transfer.

Challenges

- Regulatory Compliance and Safety Standards

Varying international safety regulations complicate global trade, requiring adaptations that raise costs and hinder uniformity. This challenge demands ongoing compliance efforts to avoid penalties.

In addition, competition from alternative transport modes like aviation in passenger segments pressures the market, necessitating continuous innovation to maintain relevance.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 4.92 Billion |

Projected Market Size in 2034 |

USD 8.06 Billion |

CAGR Growth Rate |

5.6% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Nippon Steel Corporation, Amsted Rail, GHH-BONATRANS, Interpipe, OMK Steel, Lucchini RS Group, CAF USA, Inc., Kolowag, EVRAZ NTMK, Taiyuan Heavy Industry Co., Ltd., and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Rail Wheel market is segmented by type, application, end-user, and region.

Based on Type Segment, the Rail Wheel market is divided into forged wheels, cast wheels, and others. The most dominant segment is forged wheels, followed by cast wheels as the second most dominant. Forged wheels dominate due to their enhanced mechanical properties, including higher tensile strength and impact resistance, making them preferred for high-load applications like freight and high-speed rails, driving the market by ensuring reliability and reducing downtime; cast wheels, offering cost-effective production for standard uses, support growth by catering to budget-conscious segments while maintaining adequate performance.

Based on Application Segment, the Rail Wheel market is divided into high-speed rail, freight wagons, passenger wagons, locomotives, and others. The most dominant segment is freight wagons, followed by high-speed rail as the second most dominant. Freight wagons lead owing to the global surge in cargo transport needs, requiring robust wheels for heavy-duty operations, propelling market expansion through logistics efficiency; high-speed rail, with demands for precision and low noise, drives growth by supporting modern infrastructure projects.

Based on End-User Segment, the Rail Wheel market is divided into OEM, aftermarket, and others. The most dominant segment is OEM, followed by aftermarket as the second most dominant. OEM dominates as it involves direct supply to rail manufacturers for new vehicles, ensuring quality integration and boosting the market via large contracts; the aftermarket, focusing on replacements and maintenance, contributes to growth by extending vehicle lifespan.

Recent Developments

- In June 2025, Indian Railways partnered with Ramakrishna Forgings and Titagarh Rail Systems to establish a forged-wheel manufacturing plant in Tamil Nadu, aiming for 80,000 units annually from 2026.

- In January 2025, Nippon Steel Corporation announced advancements in alloy-steel wheels for improved durability in high-speed applications.

- In April 2025, Amsted Rail expanded its production facilities in North America to meet growing demand for freight wheels.

- In September 2024, GHH-BONATRANS introduced resilient wheels with enhanced vibration damping for urban rail systems.

Regional Analysis

- Asia Pacific to Dominate the Global Market

Asia Pacific dominates the Rail Wheel market, led by China, where massive investments in high-speed rail networks and freight corridors drive demand for advanced wheels, supported by government initiatives like Belt and Road that expand connectivity, fostering local manufacturing and technological upgrades for efficiency.

North America maintains a strong position, with the United States leading through freight rail expansions and modernization efforts, emphasizing durable wheels for heavy-haul operations amid growing e-commerce logistics needs.

Europe exhibits steady growth, dominated by Germany, focusing on sustainable rail systems with EU funding for green transport, promoting innovative wheels that reduce emissions and noise in dense urban areas.

Latin America is emerging, led by Brazil, through infrastructure projects enhancing export capabilities, adopting cost-effective wheels to support mining and agricultural freight transport.

The Middle East & Africa region shows potential, with South Africa at the forefront, driven by mining rail demands and UAE's high-speed initiatives integrating modern wheels for reliability in harsh environments.

Competitive Analysis

The global Rail Wheel market is dominated by players:

- Nippon Steel Corporation

- Amsted Rail

- GHH-BONATRANS

- Interpipe

- OMK Steel

- Lucchini RS Group

- CAF USA, Inc.

- Kolowag

- EVRAZ NTMK

- Taiyuan Heavy Industry Co., Ltd.

- Others

The global Rail Wheel market is segmented as follows:

By Type

- Forged Wheels

- Cast Wheels

By Application

- High-Speed Rail

- Freight Wagons

- Passenger Wagons

- Locomotives

By End-User

- OEM

- Aftermarket

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Nippon Steel Corporation

- Amsted Rail

- GHH-BONATRANS

- Interpipe

- OMK Steel

- Lucchini RS Group

- CAF USA, Inc.

- Kolowag

- EVRAZ NTMK

- Taiyuan Heavy Industry Co., Ltd.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors