![]()

Search Market Research Report

Polyols (Polyester and Polyether) Market Size, Share Global Analysis Report, 2026-2034

Polyols (Polyester and Polyether) Market Size, Share, Growth Analysis Report By Type (Polyether Polyols, Polyester Polyols), By Application (Flexible Foam, Rigid Foam, CASE, Others), By End-User (Construction, Automotive, Furniture, Packaging, Electronics, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

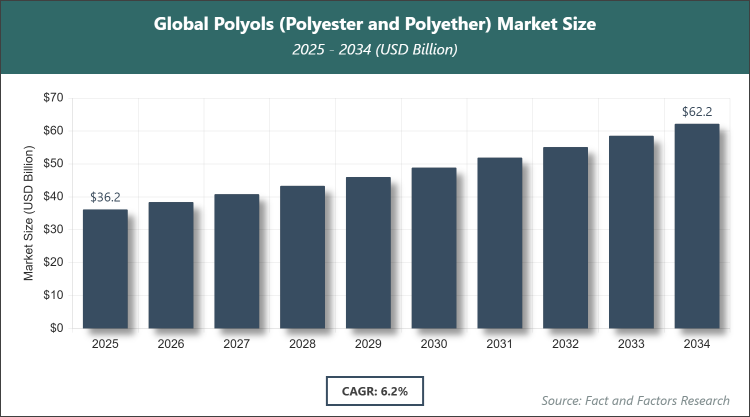

[220+ Pages Report] According to Facts & Factors, the global Polyols (Polyester and Polyether) market size was estimated at USD 36.2 billion in 2025 and is expected to reach USD 65.22 billion by the end of 2034. The Polyols (Polyester and Polyether) industry is anticipated to grow by a CAGR of 6.2% between 2026 and 2034. The Polyols (Polyester and Polyether) Market is driven by increasing demand for polyurethane foams in construction, automotive, and furniture sectors.

Market Overview

Market Overview

Polyols, specifically polyester and polyether types, refer to organic compounds containing multiple hydroxyl groups that serve as key raw materials in the production of polyurethanes. These compounds are essential in creating flexible and rigid foams, coatings, adhesives, sealants, and elastomers used across various industries. Polyester polyols are derived from the reaction of dicarboxylic acids and glycols, offering high thermal stability and mechanical strength, while polyether polyols are produced through the polymerization of epoxides like propylene oxide, providing superior flexibility and hydrolytic resistance. This market encompasses the synthesis, distribution, and application of these polyols, driven by their versatility in enhancing product performance in end-use sectors without relying on quantitative metrics.

Key Insights

- As per the analysis shared by our research analyst, the global Polyols (Polyester and Polyether) market is estimated to grow annually at a CAGR of around 6.2% over the forecast period (2026-2034).

- In terms of revenue, the global Polyols (Polyester and Polyether) market size was valued at around USD 36.2 billion in 2025 and is projected to reach USD 65.22 billion by 2034.

- The market is driven by rising demand for energy-efficient insulation materials in construction and automotive applications.

- Based on the type, the polyether polyols segment dominated with a 68% share due to its widespread use in flexible foams and superior compatibility with isocyanates.

- Based on the application, the flexible foam segment dominated with a 45% share owing to its extensive adoption in furniture, bedding, and automotive interiors for comfort and durability.

- Based on the end-user, the construction segment dominated with a 35% share because of the need for high-performance insulation and building materials.

- Based on the region, Asia Pacific dominated with a 42% share attributed to rapid industrialization, expanding manufacturing base, and high demand from China and India.

Growth Drivers

- Increasing Demand for Polyurethane Foams in Key Industries

The escalating need for lightweight and durable materials in sectors like automotive and construction has significantly boosted the adoption of polyurethane foams, which rely heavily on polyols as precursors. This trend is fueled by global efforts toward fuel efficiency and sustainable building practices, where polyols enable the creation of high-insulation products that reduce energy consumption.

Furthermore, advancements in polyol formulations have enhanced their properties, such as improved fire resistance and environmental compatibility, making them indispensable in modern manufacturing processes. The integration of polyols in innovative applications continues to expand market potential.

Restraints

- Volatility in Raw Material Prices

Fluctuations in the prices of key feedstocks like propylene oxide and adipic acid pose a significant challenge, impacting production costs and profit margins for manufacturers. These price instabilities are often influenced by geopolitical factors and supply chain disruptions, leading to unpredictable market conditions.

Additionally, stringent environmental regulations on petrochemical-derived materials increase compliance costs, potentially slowing down expansion in certain regions. This restraint necessitates strategic sourcing and hedging practices to mitigate risks.

Opportunities

- Rise of Bio-Based Polyols

The shift toward sustainable and eco-friendly alternatives presents substantial opportunities, as bio-based polyols derived from renewable sources like vegetable oils gain traction amid growing environmental awareness. This development aligns with global sustainability goals and opens new avenues in green chemistry applications.

Moreover, emerging markets in developing economies offer untapped potential for polyol penetration, driven by infrastructure growth and rising consumer demand for high-quality products. Innovation in bio-based technologies could further differentiate offerings and capture premium segments.

Challenges

- Environmental and Regulatory Pressures

Increasing scrutiny on the environmental impact of polyol production, including emissions and waste management, creates hurdles for industry players. Compliance with evolving regulations requires substantial investments in cleaner technologies and processes.

In addition, competition from alternative materials like phenolic resins in specific applications challenges market share, demanding continuous R&D to maintain polyols' competitive edge. Addressing these issues is crucial for long-term viability.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 36.2 Billion |

Projected Market Size in 2034 |

USD 65.22 Billion |

CAGR Growth Rate |

6.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

BASF SE, Covestro AG, The Dow Chemical Company, Huntsman Corporation, Shell Chemicals, Mitsui Chemicals, Sinopec, Stepan Company, Wanhua Chemical Group, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Polyols (Polyester and Polyether) market is segmented by type, application, end-user, and region.

Based on Type Segment, the Polyols (Polyester and Polyether) market is divided into polyether polyols, polyester polyols, and others. The most dominant segment is polyether polyols, followed by polyester polyols as the second most dominant. Polyether polyols lead due to their excellent flexibility, low viscosity, and high reactivity, which make them ideal for producing flexible foams used in automotive seating and furniture; this dominance drives the market by enabling cost-effective production of versatile polyurethane products that meet diverse industry needs for comfort and performance, while polyester polyols, with their superior thermal stability and mechanical strength, support growth in rigid applications like coatings and adhesives, contributing to overall market expansion through enhanced durability in high-end uses.

Based on Application Segment, the Polyols (Polyester and Polyether) market is divided into flexible foam, rigid foam, CASE, and others. The most dominant segment is flexible foam, followed by rigid foam as the second most dominant. Flexible foam dominates owing to its widespread use in cushioning for furniture, bedding, and automotive interiors, providing superior comfort and resilience that cater to consumer preferences; this drives market growth by fulfilling high-volume demands in everyday products, whereas rigid foam, valued for its excellent insulation properties, supports expansion in construction and appliances by enabling energy-efficient solutions that align with sustainability trends.

Based on End-User Segment, the Polyols (Polyester and Polyether) market is divided into construction, automotive, furniture, packaging, electronics, and others. The most dominant segment is construction, followed by automotive as the second most dominant. Construction leads because polyols are crucial for insulation foams and sealants that enhance building energy efficiency and durability, driving the market through large-scale infrastructure projects; automotive follows, utilizing polyols in lightweight interiors and components to improve fuel efficiency and safety, thereby boosting overall demand amid rising vehicle production.

Recent Developments

- In May 2025, Rymbal launched FluidX, an innovative polyurethane material that is fully recyclable using both physical and chemical recycling processes, aiming to enhance sustainability in the polyols sector.

- In May 2025, Dongsung Chemical opened a new 81,000 m² polyurethane production plant in Karawang, Indonesia, tripling its output with 67,000 tons annually of prepolymers, polyester polyols, and resins.

- In January 2025, Dow announced the closure of its 94 ktpa polyether polyols facility in Tertre, Belgium, by March 2026, due to high European energy costs.

- In September 2024, BASF and Future Foam introduced the first commercial flexible foam for the bedding industry, focusing on enhanced recyclability.

Regional Analysis

- Asia Pacific to Dominate the Global Market

The Asia Pacific region dominates the Polyols (Polyester and Polyether) market, primarily driven by rapid industrialization and a booming manufacturing sector in countries like China, which serves as the leading producer and consumer due to its vast chemical industry infrastructure and high demand from construction and automotive sectors.

North America follows as a key region, with the United States leading through advanced technological innovations and strong end-user industries such as automotive and furniture, supported by a focus on energy-efficient materials.

Europe maintains a significant presence, led by Germany, where stringent environmental regulations promote the adoption of high-performance polyols in sustainable building practices and automotive applications.

Latin America shows steady growth, with Brazil at the forefront, benefiting from expanding construction activities and increasing investments in polyurethane-based products.

The Middle East & Africa region is emerging, driven by infrastructure development in countries like South Africa, though it faces challenges from raw material dependencies.

Competitive Analysis

The global Polyols (Polyester and Polyether) market is dominated by players:

- BASF SE

- Covestro AG

- The Dow Chemical Company

- Huntsman Corporation

- Shell Chemicals

- Mitsui Chemicals

- Sinopec

- Stepan Company

- Wanhua Chemical Group

- Others

The global Polyols (Polyester and Polyether) market is segmented as follows:

By Type

- Polyether Polyols

- Polyester Polyols

By Application

- Flexible Foam

- Rigid Foam

- CASE

- Others

By End-User

- Construction

- Automotive

- Furniture

- Packaging

- Electronics

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- BASF SE

- Covestro AG

- The Dow Chemical Company

- Huntsman Corporation

- Shell Chemicals

- Mitsui Chemicals

- Sinopec

- Stepan Company

- Wanhua Chemical Group

Frequently Asked Questions

What are the emerging trends and innovations impacting the Polyols (Polyester and Polyether) market?

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors