![]()

Search Market Research Report

PET Preforms Market Size, Share Global Analysis Report, 2026-2034

PET Preforms Market Size, Share, Growth Analysis Report By Capacity (Up to 500 ml, 500 to 1000 ml, 1000 to 2000 ml, More than 2000 ml), By Neck Type (ROPP/BPV, PCO/BPF, Alaska/Bericap/Obrist, Others), By Application (Carbonated Soft Drinks, Water, Food, Non-Carbonated Drinks, Cosmetics & Chemicals, Pharma & Liquor, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

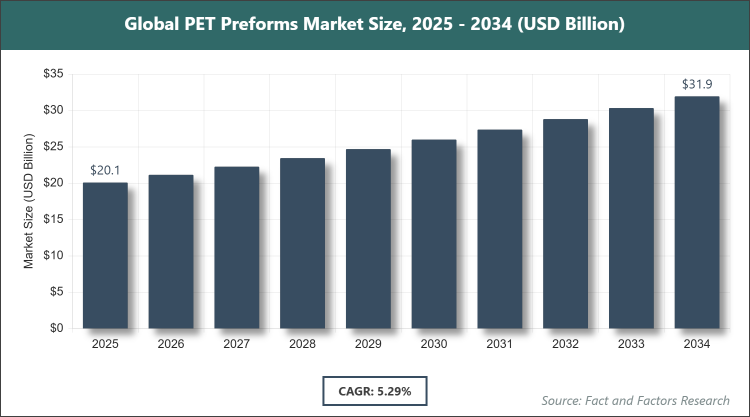

[250+ Pages Report] According to Facts & Factors, the global PET Preforms market size was estimated at USD 20.09 billion in 2025 and is expected to reach USD 31.95 billion by 2034, growing at a CAGR of 5.29% from 2026 to 2034. The PET Preforms Market is driven by the rising demand for packaged beverages and sustainable packaging solutions.

Market Overview

Market Overview

PET preforms are semi-finished products made from polyethylene terephthalate resin, shaped into tubular forms with a threaded neck, designed to be blow-molded into bottles or containers for various applications in packaging. These preforms serve as the foundational component in the production of lightweight, durable, and recyclable plastic bottles, offering advantages such as clarity, barrier properties against gases and moisture, and compatibility with high-speed manufacturing processes, making them essential in industries requiring efficient and cost-effective packaging solutions without compromising on product integrity or shelf life.

Key Insights

- The PET Preforms market was valued at USD 20.09 billion in 2025 and is projected to reach USD 31.95 billion by the end of 2034.

- The market is expected to grow at a CAGR of 5.29% between 2026 and 2034.

- The PET Preforms market is driven by rising demand for packaged beverages and sustainable packaging solutions.

- Based on the Capacity segment, the 500 to 1000 ml subsegment dominated the market in 2025 with a share of 44.0% because of its suitability for standard beverage formats like water and soft drinks, optimizing production efficiency and distribution.

- Based on the Neck Type segment, the PCO/BPF subsegment dominated the market in 2025 with a share of 45.0% because it is the standard for carbonated beverages, ensuring secure sealing and compatibility with capping systems.

- Based on the Application segment, the Carbonated Soft Drinks subsegment dominated the market in 2025 with a share of 61.55% because of high global consumption and the need for pressure-resistant packaging.

- Asia Pacific held the largest market share of 46.20% in 2025 due to rapid urbanization, large population, and booming manufacturing in countries like China and India.

Growth Drivers

- Increasing Demand for Packaged Beverages

The surge in consumption of bottled water, soft drinks, and ready-to-drink beverages globally has heightened the need for PET preforms, as they provide lightweight and shatter-resistant packaging options. This driver is amplified by urbanization and changing lifestyles in emerging economies, where convenience-oriented products drive volume growth, supported by advancements in blow-molding technology for efficient production.

- Shift Toward Sustainable and Recyclable Packaging

Growing environmental awareness and regulations promoting recycled PET (rPET) have boosted adoption, as PET preforms enable circular economy practices with high recyclability rates. This trend is reinforced by brand commitments to sustainability, leading to innovations in lightweighting and bio-based PET, reducing carbon footprints and appealing to eco-conscious consumers.

- Expansion in Emerging Markets

Rapid industrialization in Asia-Pacific and Latin America has increased manufacturing capacities, fueling demand for cost-effective PET preforms in diverse applications. This growth is driven by rising disposable incomes and retail sector development, enabling broader access to packaged goods and supporting local production to meet regional needs.

Restraints

- Volatility in Raw Material Prices

Fluctuations in petroleum-based PET resin prices, influenced by oil market dynamics, increase production costs and impact profitability for manufacturers. This restraint challenges pricing stability, as suppliers pass on costs to end-users, potentially slowing adoption in price-sensitive markets and encouraging shifts to alternatives.

- Environmental Regulations and Plastic Bans

Stringent policies on single-use plastics and recycling mandates in regions like Europe pose compliance hurdles, raising operational expenses for non-sustainable practices. This limits market expansion by necessitating investments in rPET infrastructure, while public anti-plastic sentiment could reduce demand in certain segments.

Opportunities

- Advancements in Recycled PET Technology

Innovations in rPET processing offer opportunities to meet regulatory recycled content requirements, such as EU's 30% by 2030, expanding premium sustainable segments. This enables differentiation through eco-friendly products, attracting partnerships with brands and unlocking growth in high-value applications like pharmaceuticals.

- Growth in Non-Beverage Applications

Expanding use in food, cosmetics, and chemicals provides diversification, as PET preforms offer superior barrier properties and customization. This opportunity is fueled by e-commerce trends requiring durable packaging, fostering new market entries and collaborations for specialized preforms.

Challenges

- Supply Chain Disruptions

Global events like pandemics or geopolitical tensions disrupt resin supply, leading to shortages and delayed deliveries. This affects production timelines, compelling manufacturers to stockpile or seek alternatives, increasing costs and hindering responsiveness to demand fluctuations.

- Competition from Alternative Materials

Rise of biodegradable plastics and glass in eco-focused markets challenges PET's dominance, as consumers prefer perceived sustainable options. This requires ongoing R&D to enhance PET's environmental profile, straining resources for smaller players in a competitive landscape.

Report Scope

Report Attribute |

Details |

Market Size in 2025 |

USD 20.09 Billion |

Projected Market Size in 2034 |

USD 31.95 Billion |

CAGR Growth Rate |

5.29% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

ALPLA Group, Indorama Ventures Public Company Limited, Plastipak Holdings Inc., RESILUX NV, Retal Industries Ltd., Sipa S.p.A., Societe Generale Des Techniques (SGT), Amcor Limited, Taiwan Hon Chuan Enterprise Co. Ltd., CAIBA, Chemco Group, Esterform Ltd., KÖKSAN Pet Packaging Industry Co., Polisan Hellas, Varioform PET, and Others. |

Key Segment |

By Capacity, By Neck Type, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The PET Preforms market is segmented by type, application, end-user, and region.

Based on Capacity Segment, the PET Preforms market is divided into Up to 500 ml, 500 to 1000 ml, 1000 to 2000 ml, and More than 2000 ml. The most dominant segment is 500 to 1000 ml, holding 44.0% share, due to its alignment with popular beverage sizes for water and soft drinks, enabling high-volume production and efficient logistics that drive market growth through cost savings and broad applicability; the second most dominant is Up to 500 ml, which supports market expansion by catering to single-serve and portable products in on-the-go consumption trends, enhancing convenience and reducing material usage.

Based on Neck Type Segment, the PET Preforms market is divided into ROPP/BPV, PCO/BPF, Alaska/Bericap/Obrist, and others. The most dominant segment is PCO/BPF, with 45.0% share, owing to its standardization in carbonated beverage packaging for optimal pressure resistance and capping efficiency, propelling market growth via compatibility with existing machinery; the second most dominant is ROPP/BPV, contributing to the market by providing tamper-evident features for non-carbonated drinks and pharmaceuticals, supporting diversification and regulatory compliance.

Based on Application Segment, the PET Preforms market is divided into Carbonated Soft Drinks, Water, Food, Non-Carbonated Drinks, Cosmetics & Chemicals, Pharma & Liquor, and Others. The most dominant segment is Carbonated Soft Drinks, capturing 61.55% share, because of global high consumption and the need for durable, gas-barrier packaging that fuels market expansion through large-scale production; the second most dominant is Water, which aids growth by addressing demand for safe, portable hydration solutions in developing regions, promoting lightweight and recyclable options.

Recent Developments

- In February 2025, Indorama Ventures acquired a 24.9% stake in EPL Limited, an Indian specialty packaging company, for $219 million, enhancing its presence in the packaging sector and supporting sustainable growth.

- In September 2024, Indorama Ventures, in a joint venture with Dhunseri Ventures Limited and Varun Beverages Limited, began constructing two PET recycling facilities in India to boost recycled content production.

- In May 2026, Alpla introduced a new 0.75-liter recyclable PET wine bottle, reducing carbon emissions by up to 50% and costs by 30%, fully made from recycled PET for the Austrian market.

- In August 2025, Husky Technologies and Origin Materials Inc. integrated sustainable chemical furan dicarboxylic acid (FDCA) for advanced packaging, polymerizing bio-based FDCA into PET for eco-friendly preforms.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific dominates the PET Preforms market with a 46.20% share, driven by massive population growth, urbanization, and expanding beverage industries; China leads the region as the largest producer and consumer, with its vast manufacturing infrastructure in cities like Shanghai and Guangzhou supporting low-cost production, government incentives for recycling, and high demand from domestic and export markets for bottled water and soft drinks.

North America shows steady growth, supported by sustainability initiatives and advanced technology; the United States dominates, with key players in states like Texas and California driving innovation in rPET, where regulations like California's recycled content mandates and consumer preferences for eco-packaging in urban areas like New York boost market penetration.

Europe emphasizes regulatory compliance and circular economy; Germany leads, leveraging efficient recycling systems in hubs like Munich and Berlin, with EU directives on tethered caps and recycled content fostering high-purity preform production for premium beverages and cosmetics.

Latin America experiences emerging growth amid economic recovery; Brazil dominates, with expanding retail in Sao Paulo and Rio de Janeiro fueling demand for affordable packaging in soft drinks and water, supported by local resin production and sustainability efforts.

The Middle East and Africa are developing, focused on infrastructure; South Africa leads in Africa with growing urbanization in Johannesburg, while Saudi Arabia drives in the Middle East through investments in petrochemicals and beverage exports from Riyadh, emphasizing halal-certified and durable preforms.

Competitive Analysis

The global PET Preforms market is dominated by players:

- ALPLA Group

- Indorama Ventures Public Company Limited

- Plastipak Holdings Inc.

- RESILUX NV

- Retal Industries Ltd.

- Sipa S.p.A.

- Societe Generale Des Techniques (SGT)

- Amcor Limited

- Taiwan Hon Chuan Enterprise Co. Ltd.

- CAIBA

- Chemco Group

- Esterform Ltd.

- KÖKSAN Pet Packaging Industry Co.

- Polisan Hellas

- Varioform PET

The global PET Preforms market is segmented as follows:

By Capacity

- Up to 500 ml

- 500 to 1000 ml

- 1000 to 2000 ml

- More than 2000 ml

By Neck Type

- ROPP/BPV

- PCO/BPF

- Alaska/Bericap/Obrist

- Others

By Application

- Carbonated Soft Drinks

- Water

- Food

- Non-Carbonated Drinks

- Cosmetics & Chemicals

- Pharma & Liquor

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors