![]()

Search Market Research Report

Medical X-ray Film Market Size, Share Global Analysis Report, 2026-2034

Medical X-ray Film Market Size, Share, Growth Analysis Report By Type (Traditional X-ray Film, Digital X-ray Film, Thermal X-ray Film, and Others), By Application (General Radiography, Dental, Mammography, Orthopedic, Others), By End-User (Hospitals, Diagnostic Imaging Centers, Clinics, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

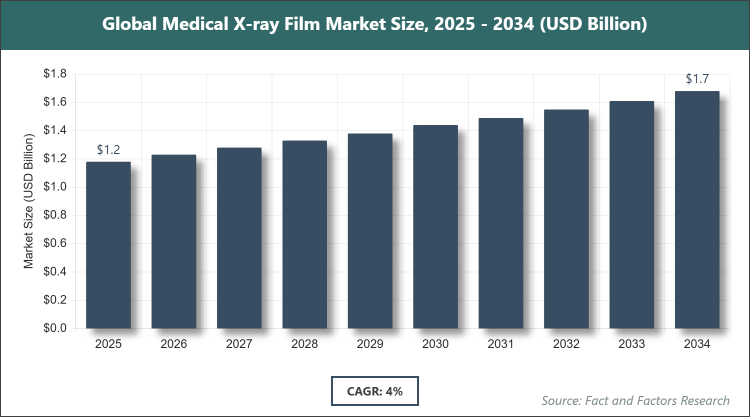

[232+ Pages Report] According to Facts & Factors, the global Medical X-ray Film market size was estimated at USD 1.18 billion in 2025 and is expected to reach USD 1.68 billion by the end of 2034. The Medical X-ray Film industry is anticipated to grow by a CAGR of 4.0% between 2026 and 2034. The Medical X-ray Film Market is driven by sustained demand in developing regions and specialized diagnostic applications despite digital transition.

Market Overview

Market Overview

Medical X-ray film is a light-sensitive photographic material used in traditional radiography to capture diagnostic images produced by X-ray radiation passing through the body. It consists of a polyester base coated with an emulsion layer containing silver halide crystals that react to X-ray exposure, forming a visible image after chemical processing. Although largely supplanted by digital radiography in advanced healthcare systems, X-ray film remains relevant in resource-limited settings, for specific modalities such as mammography and orthopedics, and in facilities requiring archival hard-copy images or operating without reliable digital infrastructure, providing a cost-effective and proven method for visualizing internal structures.

Key Insights

- As per the analysis shared by our research analyst, the global Medical X-ray Film market is estimated to grow annually at a CAGR of around 4.0% over the forecast period (2026-2034).

- In terms of revenue, the global Medical X-ray Film market size was valued at around USD 1.18 billion in 2025 and is projected to reach USD 1.68 billion by 2034.

- The market is driven by continued usage in emerging economies and specialized imaging applications.

- Based on the type, the traditional X-ray film segment dominated the market with a share of 68%, as it remains the most affordable and widely available option in low-resource healthcare facilities.

- Based on the application, the general radiography segment dominated with a share of 52%, due to its broad utility in routine chest, abdominal, and skeletal examinations.

- Based on the end-user, the hospitals segment dominated with a share of 58%, attributed to high patient volumes and the presence of radiology departments in large facilities.

- Asia Pacific dominated the global market with a share of 48%, owing to large population base, growing healthcare infrastructure in rural areas, and slower digital radiography adoption rates.

Growth Drivers

- Persistent Demand in Developing Regions

In many low- and middle-income countries, traditional X-ray film continues to be the backbone of diagnostic imaging due to lower capital investment requirements compared to digital systems and the absence of reliable electricity or IT infrastructure needed for digital workflows. This sustained usage supports steady consumption volumes, particularly in public hospitals and rural clinics where affordability and simplicity are prioritized.

Moreover, government health programs in emerging markets frequently include procurement of analog X-ray systems and consumables as part of expanding basic diagnostic services, ensuring a reliable baseline demand even as digital penetration gradually increases.

Restraints

- Accelerating Shift to Digital Radiography

The global transition toward computed radiography (CR) and direct digital radiography (DR) systems continues to erode the market for conventional X-ray film, as digital solutions offer immediate image availability, no chemical processing, lower long-term operating costs, and easier storage and sharing capabilities. This shift is especially pronounced in high-income countries and urban centers of developing nations.

Additionally, environmental regulations targeting the reduction of silver-containing waste and hazardous processing chemicals further discourage new installations of film-based systems, accelerating the replacement cycle and limiting future film demand.

Opportunities

- Specialized and Niche Applications

Certain high-resolution and archival applications, including full-field digital mammography backups, orthopedic templating, and forensic radiography, continue to favor traditional film for its proven image quality characteristics and tactile review properties preferred by some radiologists.

Furthermore, hybrid environments in mid-tier facilities where digital systems are used for routine work but film remains for specific procedures create a transitional demand window that can be captured through targeted product offerings and service support.

Challenges

- Supply Chain Vulnerabilities & Raw Material Costs

The market remains vulnerable to supply disruptions of key raw materials (silver halides, polyester base film) and the reduction in global production capacity as major manufacturers scale back analog film lines in favor of digital media.

In addition, price volatility of silver and increasing logistics costs for temperature-controlled transport of unexposed film add pressure on margins and make long-term pricing agreements difficult, particularly affecting smaller distributors in price-sensitive markets.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.18 Billion |

Projected Market Size in 2034 |

USD 1.68 Billion |

CAGR Growth Rate |

4.0% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Fujifilm Holdings Corporation, Carestream Health, Agfa-Gevaert N.V., Konica Minolta, Inc., Shanghai Shenbei Photosensitive Co., Ltd., Tianjin Medical X-ray Film Co., Ltd., Lucky Film Co., Ltd., Foma Bohemia spol. s r.o., China Lucky Film Corporation, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Medical X-ray Film market is segmented by type, application, end-user, and region.

Based on Type Segment, the Medical X-ray Film market is divided into traditional X-ray film, digital X-ray film, thermal X-ray film, and others. The traditional X-ray film segment emerges as the most dominant, holding approximately 68% market share, primarily due to its entrenched position in cost-sensitive healthcare systems and regions with limited digital infrastructure, driving the market by maintaining baseline consumption in general radiography worldwide. The digital X-ray film (CR cassette-based) segment follows as the second most dominant, with around 22% share, benefiting from its role as a bridge technology in facilities upgrading from analog to full DR, contributing to market stability during the transition phase.

Based on Application Segment, the Medical X-ray Film market is divided into general radiography, dental, mammography, orthopedic, others. The general radiography segment is the most dominant, capturing about 52% of the market, as it covers the largest volume of routine diagnostic procedures (chest, abdomen, extremities) still performed using film in many parts of the world, helping to drive the market through sheer procedural volume in emerging healthcare systems. The dental segment ranks second, with roughly 18% share, leveraging dedicated intraoral and extraoral films that remain popular in private dental practices and regions with slower digital adoption.

Based on End-User Segment, the Medical X-ray Film market is divided into hospitals, diagnostic imaging centers, clinics, others. The hospitals segment is the most dominant, capturing about 58% of the market, propelled by large patient throughput, trauma & emergency imaging needs, and centralized radiology departments that continue using film in many public and mid-tier facilities, thereby driving the market through consistent bulk procurement. The diagnostic imaging centers segment ranks second, with roughly 22% share, utilizing film for specialized studies and as backup in hybrid setups.

Recent Developments

- In late 2024, Fujifilm reduced production of certain lines of medical X-ray film at its Ashigara facility but maintained output of high-demand orthopedic and mammography films to serve transitional markets.

- In March 2025, Carestream Health announced an extension of its legacy film production commitment through 2028 in response to requests from government health ministries in Southeast Asia and Africa.

- In September 2025, Agfa-Gevaert restructured its radiology consumables division, consolidating analog film manufacturing in one European plant to improve cost efficiency while continuing supply to public-sector clients.

- In January 2026, Konica Minolta introduced an enhanced green-sensitive X-ray film optimized for lower-dose imaging protocols still using film-screen systems in emerging markets.

- In Q1 2026, several Indian and Chinese manufacturers increased export volumes of economy-grade medical X-ray film to African and South Asian countries to fill supply gaps left by Western producers.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific remains the largest consumer of medical X-ray film, driven by vast population coverage, uneven digital radiography penetration, and continued reliance on analog systems in public hospitals and rural diagnostic facilities. China dominates this region with its enormous number of county-level hospitals and township health centers still using film-based imaging, while simultaneously supporting domestic manufacturers that supply low-cost film to both domestic and export markets.

North America represents a mature but declining market, where film is largely limited to niche applications, legacy equipment, and specific customer preferences. The United States leads, with remaining demand concentrated in certain rural hospitals, chiropractic clinics, podiatry practices, and forensic/orthopedic templating uses that have been slow to convert fully to digital.

Europe shows steady contraction, with most countries having completed the transition to digital radiography in public and large private facilities. Germany remains the most significant regional player, primarily due to its conservative radiology community and continued use of film in select orthopedic and mammography applications, as well as for teaching and archival purposes.

Latin America exhibits mixed trends, with urban centers rapidly adopting digital while rural and public-sector facilities maintain analog systems. Brazil stands out as the dominant country, with large public health networks and private diagnostic chains still procuring substantial volumes of traditional X-ray film for cost and infrastructure reasons.

The Middle East & Africa region displays the slowest transition pace, supported by infrastructure limitations, budget constraints, and high procedural volumes in under-resourced facilities. South Africa and Egypt lead consumption, driven by large tertiary hospitals and national tuberculosis control programs that continue to rely on chest X-ray film for screening and diagnosis.

Competitive Analysis

The global Medical X-ray Film market is dominated by players:

- Fujifilm Holdings Corporation

- Carestream Health

- Agfa-Gevaert N.V.

- Konica Minolta, Inc.

- Shanghai Shenbei Photosensitive Co., Ltd.

- Tianjin Medical X-ray Film Co., Ltd.

- Lucky Film Co., Ltd.

- Foma Bohemia spol. s r.o.

- China Lucky Film Corporation

- And Others.

The global Medical X-ray Film market is segmented as follows:

By Type

- Traditional X-ray Film

- Digital X-ray Film

- Thermal X-ray Film

- Others

By Application

- General Radiography

- Dental

- Mammography

- Orthopedic

- Others

By End-User

- Hospitals

- Diagnostic Imaging Centers

- Clinics

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Fujifilm Holdings Corporation

- Carestream Health

- Agfa-Gevaert N.V.

- Konica Minolta, Inc.

- Shanghai Shenbei Photosensitive Co., Ltd.

- Tianjin Medical X-ray Film Co., Ltd.

- Lucky Film Co., Ltd.

- Foma Bohemia spol. s r.o.

- China Lucky Film Corporation

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors