![]()

Search Market Research Report

LiPF6 Market Size, Share Global Analysis Report, 2026-2034

LiPF6 Market Size, Share, Growth Analysis Report By Type (Battery Grade, Industrial Grade, and Others), By Application (Electric Vehicles, Consumer Electronics, Industrial Energy Storage, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

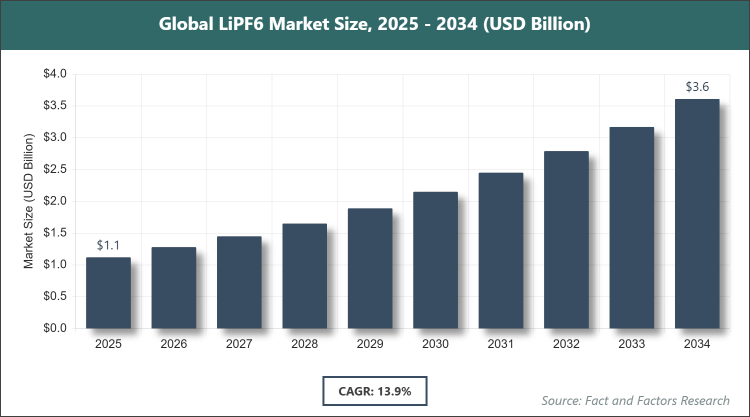

[228+ Pages Report] According to Facts & Factors, the global LiPF6 market size was estimated at USD 1.12 billion in 2025 and is expected to reach USD 6.1 billion by the end of 2034. The LiPF6 industry is anticipated to grow by a CAGR of 13.90% between 2026 and 2034. The LiPF6 Market is driven by surging demand for lithium-ion batteries in electric vehicles and renewable energy storage.

Market Overview

Market Overview

LiPF6, or Lithium Hexafluorophosphate, is a crucial inorganic compound serving as the primary electrolyte salt in lithium-ion batteries, facilitating ion conduction between electrodes for efficient charging and discharging. It is characterized by its high solubility in organic solvents, thermal stability, and ability to form a stable solid electrolyte interface, which enhances battery performance and longevity. This salt is integral to modern energy storage solutions, supporting applications where reliable power delivery is essential, such as in portable devices and large-scale energy systems, by enabling high energy density and operational safety under varying conditions.

Key Insights

- As per the analysis shared by our research analyst, the global LiPF6 market is estimated to grow annually at a CAGR of around 13.90% over the forecast period (2026-2034).

- In terms of revenue, the global LiPF6 market size was valued at around USD 1.12 billion in 2025 and is projected to reach USD 6.1 billion by 2034.

- The market is driven by the increasing adoption of electric vehicles and renewable energy systems.

- Based on the type, the battery grade segment dominated the market with a share of 70%, as it meets stringent purity requirements for high-performance lithium-ion batteries essential in EVs and electronics.

- Based on the application, the electric vehicles segment dominated with a share of 47%, due to the rapid expansion of EV manufacturing and the need for efficient battery electrolytes.

- Asia Pacific dominated the global market with a share of 47.50%, attributed to robust EV production, battery manufacturing hubs, and government incentives for clean energy in countries like China.

Growth Drivers

- Rising Demand for Electric Vehicles

The exponential growth in electric vehicle adoption worldwide has significantly boosted the demand for LiPF6, as it is a vital component in lithium-ion batteries that power these vehicles. Governments and consumers are increasingly prioritizing sustainable transportation to reduce carbon emissions, leading to massive investments in EV infrastructure and production. This trend is amplified by technological advancements in battery efficiency, where LiPF6's high conductivity and stability enable longer driving ranges and faster charging times, making EVs more appealing to the mass market.

Furthermore, collaborations between automakers and battery manufacturers are accelerating innovation, with LiPF6 playing a key role in developing next-generation batteries that offer improved safety and performance. As global regulations tighten on fossil fuel vehicles, the shift toward electrification is expected to sustain long-term demand, positioning LiPF6 as a cornerstone of the clean energy transition.

Restraints

- High Production Costs and Raw Material Volatility

The manufacturing of LiPF6 involves complex processes and expensive raw materials like phosphorus pentafluoride and lithium fluoride, which contribute to elevated production costs and limit market accessibility for smaller players. Fluctuations in raw material prices, often influenced by supply chain disruptions or geopolitical tensions, further exacerbate these challenges, leading to inconsistent pricing and potential shortages that hinder widespread adoption.

Additionally, the need for specialized facilities to handle hazardous chemicals increases operational expenses and regulatory compliance burdens. In emerging markets, where cost sensitivity is high, these factors can slow penetration, as alternatives or lower-cost substitutes are explored, potentially capping growth despite rising demand from key applications.

Opportunities

- Advancements in Renewable Energy Storage

The expanding renewable energy sector offers substantial opportunities for LiPF6, as it is essential for large-scale battery storage systems that stabilize grids powered by intermittent sources like solar and wind. Innovations in energy storage technologies, such as solid-state batteries, are incorporating LiPF6 to achieve higher energy densities and longer lifespans, enabling more efficient integration of renewables into power networks.

Moreover, government incentives and investments in green infrastructure are fostering partnerships between energy firms and chemical suppliers to develop customized LiPF6 formulations. This not only opens new revenue streams but also supports global sustainability goals, positioning manufacturers to capitalize on the shift toward decentralized and resilient energy systems.

Challenges

- Environmental and Safety Concerns

LiPF6's production and disposal raise environmental issues due to its potential to release toxic fluorides, prompting stricter regulations and the need for sustainable practices that could increase compliance costs. Safety risks in battery applications, such as thermal runaway, require ongoing research into safer alternatives, which might divert investment from LiPF6 development.

In addition, recycling challenges for lithium-ion batteries complicate end-of-life management, leading to waste accumulation and scrutiny from environmental groups. Addressing these through eco-friendly innovations is critical, but delays in adoption could impact market confidence and growth trajectories.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.12 Billion |

Projected Market Size in 2034 |

USD 6.1 Billion |

CAGR Growth Rate |

13.90% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Anhui Meisenbao Technology Co., Ltd., Foosung Co., Ltd., Iolitec Ionic Liquids Technologies GmbH, Kanto Denka Kogyo Co., Ltd., Morita New Energy Materials (Zhangjiagang) Co., Ltd., Do-Fluoride Chemicals, Tianjin Jinniu, Tinci, Stella Chemifa, Central Glass, and Others. |

Key Segment |

By Type, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The LiPF6 market is segmented by type, application, and region.

Based on Type Segment, the LiPF6 market is divided into battery grade, industrial grade, and others. The battery grade segment emerges as the most dominant, holding approximately 70% market share, primarily due to its high purity levels that ensure optimal battery performance, safety, and longevity in demanding applications like electric vehicles and consumer electronics, thereby driving market growth through enhanced reliability and efficiency in lithium-ion technology. The industrial grade segment follows as the second most dominant, with around 20% share, owing to its cost-effectiveness and suitability for large-scale energy storage and non-battery uses, contributing to market expansion by enabling broader industrial adoption and supporting scalable renewable energy solutions.

Based on Application Segment, the LiPF6 market is divided into electric vehicles, consumer electronics, industrial energy storage, and others. The electric vehicles segment is the most dominant, capturing about 47% of the market, as it leverages LiPF6's superior conductivity for high-performance batteries that enable longer ranges and faster charging, fueled by global electrification trends and helping to propel the market by meeting the surging demand for sustainable mobility. The consumer electronics segment ranks second, with roughly 30% share, benefiting from its role in compact, efficient batteries for devices like smartphones and laptops, driving market growth through continuous innovation in portable power and increasing consumer reliance on electronic gadgets.

Recent Developments

- In October 2023, Koura announced plans to invest USD 800 million in EV battery supply chain projects at St. Gabriel, Louisiana, including a LiPF6 production facility to enhance North American supply and support growing domestic battery manufacturing.

- In April 2023, Gujarat Fluorochemicals committed USD 500-600 million over three years for investments in EV batteries, including a LiPF6 complex at Dahej with an initial capacity of 1,800 tons per annum to bolster electrolyte production.

- In October 2022, Shida Shenghua formed a joint venture with Sichuan Zhongfuo Huatai New Material Technology to invest USD 280 million in a 100,000 tons annual liquid LiPF6 manufacturing project, aiming to expand production capabilities.

- In Q1 2024, Do-Fluoride Chemicals commissioned a new plant in Guangxi, China, with 30,000 metric tons annual capacity to address rising domestic EV battery demand and strengthen supply chain resilience.

- In late 2023, Tinci Materials integrated AI-based quality control into its LiPF6 production lines, improving consistency by 12% and reducing rejection rates to enhance product reliability for battery applications.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific commands the LiPF6 market, propelled by extensive battery manufacturing ecosystems and aggressive EV adoption policies that foster innovation and production scale. China dominates this region as the world's largest EV producer, with integrated supply chains from raw materials to assembly, enabling cost efficiencies and rapid technological advancements that support global exports and domestic demand for energy storage.

North America shows strong growth, driven by investments in clean energy infrastructure and incentives for domestic battery production to reduce import dependency. The United States leads here, with initiatives like the Inflation Reduction Act spurring gigafactory developments and R&D in advanced electrolytes, enhancing energy security and sustainability in transportation and grid applications.

Europe emphasizes sustainable practices and regulatory frameworks promoting green technologies, accelerating LiPF6 demand in automotive and renewable sectors. Germany stands out as the dominant country, leveraging its automotive heritage and EU subsidies to advance battery tech, focusing on high-efficiency solutions that align with carbon neutrality goals and bolster regional energy independence.

Latin America experiences emerging interest, supported by resource-rich economies exploring lithium extraction and battery value chains for economic diversification. Brazil emerges as key, utilizing its mineral reserves and partnerships with global firms to build local production, aiming to integrate into the EV supply chain and drive regional growth in renewable applications.

The Middle East & Africa region is gradually adopting LiPF6 amid diversification from oil and investments in solar energy storage. South Africa leads, capitalizing on its mining sector and renewable projects to develop battery capabilities, fostering job creation and energy access while positioning itself in the global clean energy transition.

Competitive Analysis

The global LiPF6 market is dominated by players:

- Anhui Meisenbao Technology Co., Ltd.

- Foosung Co., Ltd.

- Iolitec Ionic Liquids Technologies GmbH

- Kanto Denka Kogyo Co., Ltd.

- Morita New Energy Materials (Zhangjiagang) Co., Ltd.

- Do-Fluoride Chemicals

- Tianjin Jinniu

- Tinci

- Stella Chemifa

- Central Glass

- And Others.

The global LiPF6 market is segmented as follows:

By Type

- Battery Grade

- Industrial Grade

- Others

By Application

- Electric Vehicles

- Consumer Electronics

- Industrial Energy Storage

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Anhui Meisenbao Technology Co., Ltd.

- Foosung Co., Ltd.

- Iolitec Ionic Liquids Technologies GmbH

- Kanto Denka Kogyo Co., Ltd.

- Morita New Energy Materials (Zhangjiagang) Co., Ltd.

- Do-Fluoride Chemicals

- Tianjin Jinniu

- Tinci

- Stella Chemifa

- Central Glass

- And Others.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors