![]()

Search Market Research Report

Laboratory Water Purifier Market Size, Share Global Analysis Report, 2026-2034

Laboratory Water Purifier Market Size, Share, Growth Analysis Report By Type (Type I, Type II, Type III, and Others), By Application (HPLC, Immunochemistry, Ion Chromatography, Mammalian Cell Culture, and Others), By End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Diagnostic Laboratories, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

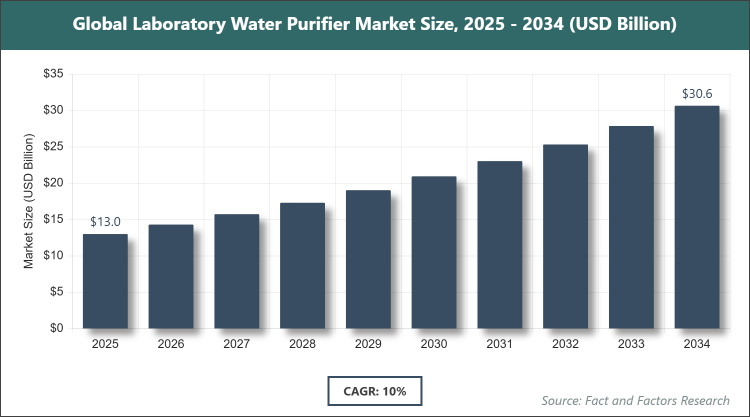

According to Facts & Factors, the global Laboratory Water Purifier market size was estimated at USD 13 billion in 2025 and is expected to reach USD 34.5 billion by the end of 2034. The Laboratory Water Purifier industry is anticipated to grow by a CAGR of 10% between 2026 and 2034. The Laboratory Water Purifier Market is driven by increasing demand for ultrapure water in pharmaceutical and biotechnology research.

Market Overview

Market Overview

The laboratory water purifier market encompasses systems designed to remove impurities, contaminants, and ions from water to produce high-purity water suitable for scientific and analytical applications. These purifiers utilize technologies such as reverse osmosis, deionization, ultraviolet oxidation, and ultrafiltration to achieve varying levels of water purity, categorized typically as Type I, Type II, or Type III. This market serves critical needs in research environments where even trace contaminants can compromise experimental results, ensuring reliability in processes like chemical analysis, cell culture, and molecular biology.

Key Insights

- As per the analysis shared by our research analyst, the global Laboratory Water Purifier market is estimated to grow annually at a CAGR of around 10% over the forecast period (2026-2034).

- In terms of revenue, the global Laboratory Water Purifier market size was valued at around USD 13 billion in 2025 and is projected to reach USD 34.5 billion, by 2034.

- The global Laboratory Water Purifier market is projected to grow at a significant rate due to the rising investments in pharmaceutical and biotechnology R&D.

- Based on the Type, Type I segment accounted for the largest market share of 40% and is dominated due to its requirement for ultrapure water in sensitive applications like HPLC and molecular biology.

- Based on the Application, HPLC segment accounted for the largest market share of 35% and is dominated due to its widespread use in analytical chemistry requiring high-purity water to avoid interference in results.

- Based on the End-User, Pharmaceutical & Biotechnology Companies segment accounted for the largest market share of 45% and is dominated due to stringent quality standards and high-volume needs in drug development and testing.

- Based on region, North America accounted for the largest market share of 35% and is dominated due to advanced research infrastructure and presence of major pharmaceutical firms.

Growth Drivers

- Increasing Demand for High-Purity Water in Research and Diagnostics

The expansion of pharmaceutical and biotechnology sectors has heightened the need for ultrapure water to ensure accurate experimental outcomes and compliance with regulatory standards. This driver is fueled by ongoing advancements in life sciences, where water quality directly impacts research integrity and product safety.

Innovations in purification technologies, such as integrated UV and filtration systems, further support this growth by enhancing efficiency and reliability in laboratory settings.

Restraints

- High Initial and Maintenance Costs

The substantial upfront investment required for advanced laboratory water purifiers poses a barrier, particularly for small-scale labs and institutions in developing regions. Ongoing expenses for consumables like filters and resins add to the financial burden, potentially limiting adoption.

Maintenance complexities and the need for specialized technicians can also deter potential users, impacting market penetration in cost-sensitive environments.

Opportunities

- Expansion in Emerging Markets

Rapid industrialization and increasing healthcare investments in Asia-Pacific and Latin America present opportunities for market growth through localized manufacturing and affordable solutions. Collaborations with local distributors can facilitate entry into these high-potential areas.

Technological adaptations tailored to regional water quality challenges can further capitalize on this opportunity, driving demand in underserved research facilities.

Challenges

- Risk of Contamination and System Downtime

Ensuring consistent water purity amid varying source water quality remains a challenge, with risks of microbial growth or ion breakthrough affecting system performance. Downtime during maintenance disrupts laboratory operations, posing operational hurdles.

Addressing these through robust monitoring and automated alerts is essential, but requires ongoing innovation to mitigate impacts on user productivity.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 13 Billion |

Projected Market Size in 2034 |

USD 34.5 Billion |

CAGR Growth Rate |

10% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Merck KGaA, Thermo Fisher Scientific Inc., Sartorius AG, ELGA LabWater (Veolia), Evoqua Water Technologies, Pall Corporation (Danaher), Labconco Corporation, Aqua Solutions Inc., Biobase Group, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Laboratory Water Purifier market is segmented by type, application, end-user, and region.

Based on Type Segment, the Laboratory Water Purifier market is divided into Type I, Type II, Type III, and others. The most dominant segment is Type I, which provides ultrapure water essential for high-sensitivity applications, holding the largest share due to its critical role in preventing contamination in advanced research. The second most dominant is Type II, used for general lab purposes like buffer preparation, offering a balance of purity and cost-effectiveness that drives market growth by supporting routine operations efficiently.

Based on Application Segment, the Laboratory Water Purifier market is divided into HPLC, Immunochemistry, Ion Chromatography, Mammalian Cell Culture, and others. The most dominant segment is HPLC, as it requires ultrapure water to maintain chromatographic accuracy and prevent peak distortions, dominating due to its extensive use in pharmaceutical quality control. The second most dominant is Mammalian Cell Culture, which relies on pure water to avoid cytotoxicity, contributing to market expansion through its importance in biotech research and vaccine development.

Based on End-User Segment, the Laboratory Water Purifier market is divided into Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Diagnostic Laboratories, and others. The most dominant segment is Pharmaceutical & Biotechnology Companies, driven by strict regulatory requirements for water quality in drug manufacturing, leading the market with high adoption rates. The second most dominant is Academic & Research Institutes, where diverse experimental needs fuel demand, aiding overall market growth through educational and innovative applications.

Recent Developments

- In January 2024, MilliporeSigma launched a new laboratory water purification system designed for high-purity needs in research applications, enhancing efficiency with integrated monitoring features.

- In March 2024, Thermo Fisher Scientific partnered with Veolia Water Technologies to offer integrated solutions for life sciences, focusing on sustainable water purification.

- In May 2024, Pall Corporation acquired Arix Water to expand its portfolio in laboratory water treatment, strengthening its market position.

- In September 2025, Merck KGaA opened a new filtration facility in Ireland, emphasizing sustainable manufacturing for laboratory water systems.

- In July 2025, Sartorius acquired MatTek Corp and Visikol Inc., bolstering its offerings in advanced lab purification technologies.

Regional Analysis

- North America to dominate the global market

North America maintains a leading position in the laboratory water purifier market, supported by robust research infrastructure and significant investments in healthcare and biotechnology. The United States stands out as the dominating country, with its concentration of top pharmaceutical companies and research universities driving demand for advanced purification systems. This region's emphasis on innovation and regulatory compliance ensures consistent adoption of high-quality water solutions, fostering technological advancements and market leadership.

Europe follows closely, benefiting from strong academic and industrial research ecosystems. Germany emerges as the dominating country, renowned for its engineering expertise and focus on precision in life sciences. The region's stringent environmental and quality standards promote the use of efficient purifiers, while collaborations between institutions and manufacturers enhance product development and accessibility across diverse applications.

Asia Pacific is experiencing rapid growth, driven by expanding pharmaceutical sectors and increasing R&D activities. China is the dominating country, with its massive investments in biotech parks and manufacturing hubs accelerating market expansion. Improving infrastructure and rising awareness of water purity's role in research quality are key factors, positioning the region as a future powerhouse in laboratory equipment.

Latin America shows emerging potential, with growing healthcare initiatives and research capabilities. Brazil dominates the region, supported by its developing pharmaceutical industry and government-backed science programs. Challenges like varying water sources are being addressed through adapted technologies, gradually increasing purifier adoption in academic and clinical settings.

The Middle East & Africa region is progressing, aided by investments in education and healthcare. South Africa leads as the dominating country, with its focus on medical research and diagnostic labs. International partnerships are introducing advanced systems, helping overcome regional water quality issues and supporting gradual market integration.

Competitive Analysis

The global Laboratory Water Purifier market is dominated by players:

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Sartorius AG

- ELGA LabWater (Veolia)

- Evoqua Water Technologies

- Pall Corporation (Danaher)

- Labconco Corporation

- Aqua Solutions Inc.

- Biobase Group

- And Others

The global Laboratory Water Purifier market is segmented as follows:

By Type

- Type I

- Type II

- Type III

- Others

By Application

- HPLC

- Immunochemistry

- Ion Chromatography

- Mammalian Cell Culture

- Others

By End-User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Hospitals & Diagnostic Laboratories

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Laboratory Water Purifier market is dominated by players:

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Sartorius AG

- ELGA LabWater (Veolia)

- Evoqua Water Technologies

- Pall Corporation (Danaher)

- Labconco Corporation

- Aqua Solutions Inc.

- Biobase Group

- And Others

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors