![]()

Search Market Research Report

Home / Smart Healthcare Products Market Size, Share Global Analysis Report, 2026-2034

Home / Smart Healthcare Products Market Size, Share, Growth Analysis Report By Type (Wearable Devices, Remote Monitoring Devices, Smart Diagnostic Devices, and Others), By Application (Chronic Disease Management, Fitness & Wellness, Elderly Care, and Others), By End-User (Individual Consumers, Homecare Providers, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

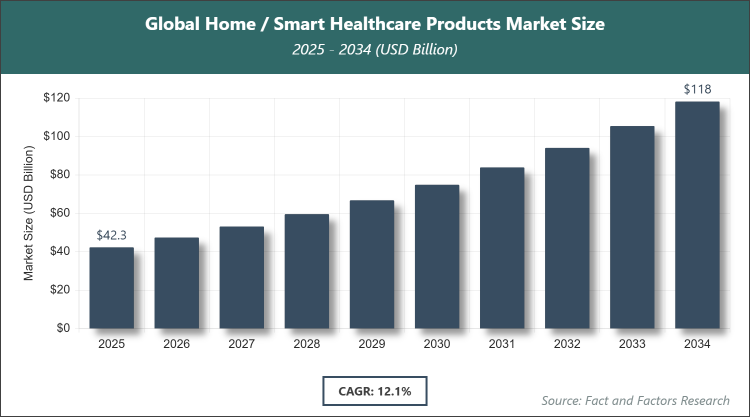

[246 Pages Report] According to Facts & Factors, the global Home / Smart Healthcare Products market size was estimated at USD 42.3 billion in 2025 and is expected to reach USD 118.7 billion by the end of 2034. The Home / Smart Healthcare Products industry is anticipated to grow by a CAGR of 12.1% between 2026 and 2034. The Home / Smart Healthcare Products Market is driven by the growing elderly population, rising prevalence of chronic diseases, and increasing adoption of IoT-enabled remote monitoring solutions.

Market Overview

Market Overview

The Home / Smart Healthcare Products market encompasses a broad range of connected, IoT-enabled devices and systems designed to deliver medical monitoring, diagnostics, treatment support, and wellness management directly within residential settings. These products integrate sensors, wireless connectivity, mobile applications, and cloud platforms to track vital signs, manage medications, detect falls, and facilitate virtual consultations with healthcare providers. By empowering individuals to manage their health independently while enabling real-time data sharing with physicians, this market bridges the gap between clinical care and everyday living, particularly benefiting aging populations, chronic disease patients, and post-acute recovery cases through improved convenience, early intervention, and reduced hospital readmissions.

Key Insights

- As per the analysis shared by our research analyst, the Home / Smart Healthcare Products market is estimated to grow annually at a CAGR of around 12.1% over the forecast period (2026-2034).

- In terms of revenue, the Home / Smart Healthcare Products market size was valued at around USD 42.3 billion in 2025 and is projected to reach USD 118.7 billion by 2034.

- The Home / Smart Healthcare Products Market is driven by an aging population and a rising chronic disease burden.

- Based on the Type, the Wearable Devices segment dominated the market in 2025 with a share of 48% due to continuous real-time monitoring capabilities and user-friendly integration with smartphones.

- Based on the Application, the Chronic Disease Management segment dominated the market in 2025 with a share of 52% owing to the high prevalence of diabetes, hypertension, and cardiovascular conditions requiring ongoing home-based tracking.

- Based on the End-User, the Individual Consumers segment dominated the market in 2025 with a share of 62% because of growing preference for self-managed health solutions and direct-to-consumer sales channels.

- North America dominated the global Home / Smart Healthcare Products market in 2025 with a share of 41%, attributed to advanced digital infrastructure, high healthcare spending, and early adoption of connected health technologies.

Growth Drivers

- Rising Aging Population and Chronic Disease Prevalence

The global increase in life expectancy and the surge in lifestyle-related chronic conditions have created strong demand for convenient, non-invasive home monitoring tools that allow seniors and patients to manage health without frequent hospital visits.

Technological convergence of AI, 5G, and wearable sensors has made these products more accurate and affordable, encouraging widespread consumer acceptance and insurance reimbursement in several markets.

Restraints

- Data Privacy Concerns and High Device Costs

Consumers remain wary of sharing sensitive health data through connected devices, while stringent regulations such as HIPAA and GDPR add compliance costs for manufacturers.

Premium pricing of advanced smart devices limits accessibility for lower-income households and slows penetration in price-sensitive emerging economies.

Opportunities

- Expansion of Telehealth and AI-Driven Personalization

The post-pandemic acceptance of virtual care has opened doors for integrated home ecosystems that combine monitoring devices with AI-powered predictive analytics and remote physician consultations.

Partnerships between device makers, insurers, and tech giants are enabling subscription-based models and bundled offerings that improve affordability and long-term adherence.

Challenges

- Interoperability Issues and Digital Divide

Lack of standardized protocols among different manufacturers creates integration difficulties with existing electronic health records and hospital systems.

Uneven internet access and low digital literacy in rural and elderly populations hinder effective utilization of smart healthcare solutions in many regions.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 42.3 Billion |

Projected Market Size in 2034 |

USD 118.7 Billion |

CAGR Growth Rate |

12.1% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Philips Healthcare, Medtronic plc, Abbott Laboratories, Omron Corporation, Apple Inc., Samsung Electronics Co., Ltd., Fitbit (Google), Honeywell International Inc., Withings (Nokia), iHealth Labs Inc., and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Home / Smart Healthcare Products market is segmented by type, application, end-user, and region.

Based on Type Segment, the Home / Smart Healthcare Products market is divided into wearable devices, remote monitoring devices, smart diagnostic devices, and others. The most dominant segment is Wearable Devices, driven by continuous tracking of vital signs and lifestyle metrics. The second most dominant is Remote Monitoring Devices, favored for stationary multi-parameter systems. Wearable Devices dominate due to their portability, real-time data transmission, and integration with consumer smartphones, helping drive market growth by appealing to tech-savvy users and enabling proactive health management that reduces hospital visits.

Based on Application Segment, the Home / Smart Healthcare Products market is divided into chronic disease management, fitness & wellness, elderly care, and others. The most dominant segment is Chronic Disease Management, supported by the need for continuous glucose, blood pressure, and ECG monitoring. The second most dominant is Elderly Care, boosted by fall detection and medication reminders. Chronic Disease Management leads because it addresses the largest patient population requiring lifelong monitoring, propelling market expansion through insurance coverage and physician-prescribed adoption.

Based on End-User Segment, the Home / Smart Healthcare Products market is divided into Individual consumers, homecare providers, and others. The most dominant segment is Individual Consumers, fueled by direct-to-consumer sales and self-health awareness. The second most dominant is Homecare Providers. Individual Consumers dominate due to growing empowerment through mobile apps and e-commerce platforms, driving market growth by increasing volume sales and fostering brand loyalty through personalized health insights.

Recent Developments

- In January 2026, Philips Healthcare launched the next-generation BioTelemetry remote cardiac monitoring patch with improved battery life and AI arrhythmia detection for home use.

- In November 2025, Abbott introduced the FreeStyle Libre 4 continuous glucose monitor with enhanced smartphone integration and 14-day wear time.

- In October 2025, Omron Healthcare partnered with Withings to offer combined blood pressure and sleep tracking ecosystems for elderly users.

- In July 2025, Medtronic received FDA clearance for its new Guardian 5 sensor designed specifically for home-based insulin management in Type 1 diabetes patients.

- In March 2025, Apple expanded Apple Watch health capabilities with FDA-cleared sleep apnea detection and new hypertension trend monitoring features.

Regional Analysis

- North America to dominate the global market

North America leads the Home / Smart Healthcare Products market through high consumer awareness, robust reimbursement policies, and a mature ecosystem of technology providers and healthcare payers. The region benefits from widespread smartphone penetration and strong venture capital support for digital health startups. The United States dominates within North America, with its advanced regulatory framework, large aging population, and cultural emphasis on preventive care driving rapid adoption of wearable monitors and remote diagnostic tools across both urban and suburban households.

Europe maintains significant momentum in the Home / Smart Healthcare Products market, supported by universal healthcare systems and strict data protection standards that build consumer trust. Collaborative EU initiatives accelerate interoperability between devices and national health records. Germany leads the region, leveraging its engineering excellence and strong medical device industry to develop high-precision home monitoring solutions that align with national digital health strategies and aging-in-place policies.

Asia Pacific is the fastest-growing region in the Home / Smart Healthcare Products market, propelled by rising middle-class incomes, government digital health programs, and massive elderly populations in China, Japan, and India. Rapid 5G rollout enables real-time remote consultations in rural areas. China dominates, with its vast manufacturing base and national “Healthy China 2030” initiative promoting widespread deployment of affordable smart wearables and home monitoring kits through both public and private channels.

Latin America shows steady progress in the Home / Smart Healthcare Products market, driven by improving healthcare access and growing chronic disease awareness. Brazil leads, with expanding private insurance coverage and urban consumer demand for fitness trackers and blood pressure monitors supporting gradual market maturation.

The Middle East & Africa region demonstrates promising potential in the Home / Smart Healthcare Products market, fueled by smart-city projects and rising investments in telemedicine infrastructure. The United Arab Emirates leads, incorporating advanced home healthcare solutions into its national vision for personalized preventive care and medical tourism enhancement.

Competitive Analysis

The global Home / Smart Healthcare Products market is dominated by players:

- Philips Healthcare

- Medtronic plc

- Abbott Laboratories

- Omron Corporation

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Fitbit (Google)

- Honeywell International Inc.

- Withings (Nokia)

- iHealth Labs Inc.

The global Home / Smart Healthcare Products market is segmented as follows:

By Type

- Wearable Devices

- Remote Monitoring Devices

- Smart Diagnostic Devices

- Others

By Application

- Chronic Disease Management

- Fitness & Wellness

- Elderly Care

- Others

By End-User

- Individual Consumers

- Homecare Providers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Philips Healthcare

- Medtronic plc

- Abbott Laboratories

- Omron Corporation

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Fitbit (Google)

- Honeywell International Inc.

- Withings (Nokia)

- iHealth Labs Inc.

Frequently Asked Questions

What are the major challenges restraining the growth of the Home / Smart Healthcare Products market?

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors