![]()

Search Market Research Report

Heat Meter Market Size, Share Global Analysis Report, 2026-2034

Heat Meter Market Size, Share, Growth Analysis Report By Type (Mechanical, Static, and Others), By Connectivity (Wired, Wireless, and Others), By Application (Residential, Commercial, Industrial, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

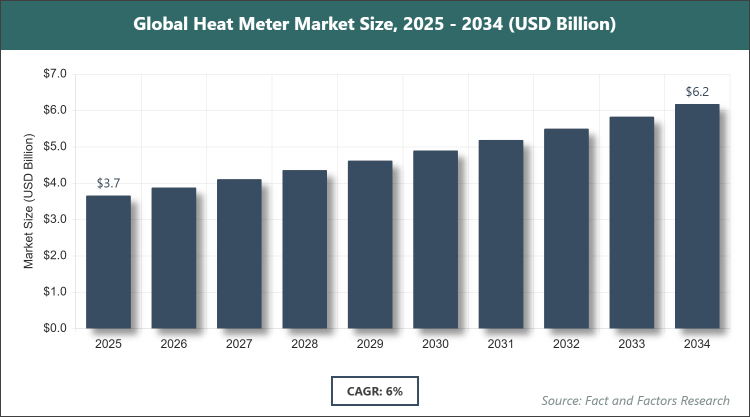

[250+ Pages Report] According to Facts & Factors, the global Heat Meter market size was estimated at USD 3.66 billion in 2025 and is expected to reach USD 6.17 billion by 2034, growing at a CAGR of 6% from 2026 to 2034. Heat Meter Market is driven by increasing demand for energy-efficient solutions and stringent government regulations on energy conservation.

Market Overview

Market Overview

A heat meter is a specialized device designed to measure the thermal energy supplied or consumed in heating and cooling systems, enabling accurate billing and efficient energy management in residential, commercial, and industrial settings. It operates by calculating the heat transfer based on the flow rate of a heat-carrying fluid, such as water, and the temperature difference between the supply and return lines, without relying on direct energy consumption metrics. This instrument plays a crucial role in district heating networks, HVAC systems, and sub-metering applications, promoting transparency in energy usage and supporting sustainability initiatives by facilitating optimized resource allocation and reduced wastage.

Key Insights

- The global Heat Meter market was valued at USD 3.66 billion in 2025 and is projected to reach USD 6.17 billion by 2034.

- The market is expected to grow at a CAGR of 6% during the forecast period from 2026 to 2034.

- The market is driven by rising adoption of district heating systems, government mandates for energy metering, and advancements in smart metering technologies.

- Based on the Type segment, Mechanical subsegment dominated with 74% share due to its cost-effectiveness, reliability, and widespread use in traditional heating infrastructures.

- Based on the Connectivity segment, Wired subsegment dominated with 65% share owing to its stable data transmission and lower susceptibility to interference in large-scale installations.

- Based on the Application segment, Residential subsegment dominated with 50% share because of increasing urbanization and the need for individual billing in multi-family housing.

- Europe dominated the global market with 40% share attributed to stringent EU energy efficiency directives and extensive district heating networks in countries like Germany and Denmark.

Growth Drivers

- Rising Demand for Energy Efficiency

The push for energy conservation has intensified globally, with governments implementing policies that mandate the installation of heat meters in new and existing buildings to monitor and optimize heat consumption. This regulatory environment encourages utilities and consumers to adopt metering solutions that provide precise data, reducing overall energy waste and lowering operational costs in heating systems.

Furthermore, technological advancements in sensor accuracy and integration with IoT platforms have made heat meters more appealing, allowing real-time monitoring and predictive maintenance that enhance system efficiency. As industries and households seek to comply with sustainability goals, the market benefits from increased investments in smart infrastructure, driving sustained growth.

Restraints

- High Initial Installation Costs

The upfront expenses associated with deploying heat meters, including hardware, installation, and calibration, pose a significant barrier, particularly in developing regions where budget constraints limit widespread adoption. This cost factor deters small-scale users and older infrastructure retrofits, slowing market penetration despite long-term savings.

Additionally, compatibility issues with legacy heating systems can escalate expenses, requiring custom modifications or replacements. Economic uncertainties and fluctuating raw material prices further exacerbate this restraint, making stakeholders hesitant to invest without clear ROI timelines.

Opportunities

- Expansion of Smart City Initiatives

Urban development projects worldwide are incorporating smart metering as part of intelligent energy management systems, creating opportunities for heat meter manufacturers to integrate with broader IoT ecosystems for enhanced data analytics and remote control. This trend is particularly prominent in Asia-Pacific, where rapid urbanization fuels demand for efficient district heating.

Moreover, partnerships between tech firms and utilities are fostering innovative solutions like wireless and ultrasonic meters, opening new revenue streams. As renewable energy sources gain traction, heat meters can play a pivotal role in measuring efficiency in hybrid systems, expanding market scope.

Challenges

- Technical Integration and Maintenance Issues

Integrating heat meters into diverse heating infrastructures often encounters challenges related to standardization and interoperability, leading to potential inaccuracies or system failures if not addressed properly. This complexity requires skilled technicians, which may be scarce in certain regions, impacting reliability.

Ongoing maintenance demands, such as periodic calibration to ensure accuracy, add to operational burdens and costs. Environmental factors like fluid quality and temperature variations can also affect performance, necessitating robust designs that increase development expenses for manufacturers.

Report Scope

Report Attribute |

Details |

Market Size in 2025 |

USD 3.66 Billion |

Projected Market Size in 2034 |

USD 6.17 Billion |

CAGR Growth Rate |

6% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Sycous Limited, Zenner International GmbH & Co. KG, Kamstrup, Danfoss, Apator SA., B Meters, Itron, Diehl Stiftung & Co. KG, Siemens, Trend Control Systems Ltd, Premier Control Technologies Ltd, Cosmic Technologies, Grundfos, Spire Metering Technology, Omni Instruments, Xi'an Kacise Optronics Tech Co., Ltd., and Others. |

Key Segment |

By Type, By Connectivity, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Heat Meter market is segmented by type, connectivity, application, and region.

Based on Type Segment, the Heat Meter market is divided into Mechanical, Static, and Others. The most dominant subsegment is Mechanical, holding approximately 74% market share, primarily due to its affordability, simple design, and proven reliability in measuring heat flow without requiring power sources, which makes it ideal for cost-sensitive applications in residential and commercial settings. This dominance drives the market by enabling broad accessibility and facilitating compliance with basic metering regulations in emerging economies. The second most dominant is Static, with around 26% share, favored for its high accuracy, low maintenance, and resistance to wear, as it uses ultrasonic or electromagnetic principles to measure flow without moving parts; this subsegment propels market growth by supporting advanced smart metering integrations that enhance energy efficiency and data-driven decision-making in modern infrastructures.

Based on Connectivity Segment, the Heat Meter market is divided into Wired, Wireless, and Others. Wired dominates with about 65% share, owing to its dependable connectivity, minimal signal loss, and suitability for fixed installations in industrial and large commercial environments where consistent data transmission is critical. It contributes to market expansion by providing a stable foundation for legacy systems transitioning to digital monitoring, ensuring accurate billing and energy management. Wireless follows as the second dominant with 35% share, driven by its flexibility, ease of installation, and compatibility with remote reading technologies, which reduce labor costs and enable real-time data access; this helps accelerate market growth through adoption in smart cities and retrofitted buildings seeking scalable, non-intrusive solutions.

Based on Application Segment, the Heat Meter market is divided into Residential, Commercial, Industrial, and Others. Residential leads with roughly 50% share, attributed to the surge in multi-unit housing and district heating systems that require individual consumption tracking for fair billing and energy conservation. This segment boosts the overall market by addressing consumer demands for transparency and efficiency in home heating, encouraging widespread installations. Commercial ranks second with 30% share, benefiting from applications in offices and retail spaces where precise sub-metering optimizes HVAC operations and reduces utility expenses; it drives growth by aligning with corporate sustainability goals and regulatory pressures for green building certifications.

Recent Developments

- In April 2025, Kamstrup announced a record-breaking demand for its smart heat metering solutions across Europe, with year-over-year order growth exceeding 45%, driven by the company's innovative ultrasonic meters that integrate seamlessly with IoT platforms for enhanced energy monitoring.

- In January 2026, Astute Analytica reported collaborations between urban planners, energy providers, and technology companies to advance data-driven heat meters, emphasizing IoT integration and smart technologies to improve accuracy and remote consumption tracking in district heating systems.

- Diehl Stiftung & Co. KG launched a new line of wireless heat meters in mid-2025, featuring advanced electromagnetic sensors that offer improved durability and real-time data analytics, targeting the growing commercial sector in Asia-Pacific.

Regional Analysis

- Europe to dominate the global market

Europe continues to lead the Heat Meter market with over 40% share, bolstered by comprehensive EU directives like the Energy Efficiency Directive that mandate metering in district heating, fostering innovation and adoption. Germany stands out as the dominating country, driven by its extensive district heating infrastructure serving millions of households and industries, supported by government subsidies for energy-efficient upgrades that reduce carbon emissions and promote sustainable urban development.

North America follows with significant growth, particularly in the U.S., where aging infrastructure replacement programs and incentives for smart metering in states like California and New York are accelerating adoption. The region's focus on integrating renewable energy sources into heating systems enhances meter utility, with Canada contributing through cold-climate demands for precise heat measurement in residential and commercial buildings, emphasizing energy conservation amid rising utility costs.

Asia-Pacific is emerging rapidly, led by China as the dominating country due to massive urbanization and government initiatives like the "Clean Heating" plan that subsidize heat meter installations in northern provinces. India's market is expanding with smart city projects in cities like Mumbai and Delhi, where heat meters aid in efficient district cooling, while Japan's advanced technology adoption focuses on seismic-resistant designs for industrial applications, driving regional innovation.

Latin America shows moderate progress, with Brazil dominating through investments in bioenergy-integrated heating systems in urban areas like Sao Paulo, supported by policies promoting energy metering to combat inefficiency. Mexico contributes via commercial sector growth in Mexico City, where heat meters help manage HVAC in high-rises, though challenges like economic variability slow broader adoption.

The Middle East & Africa region is nascent but growing, with the UAE leading in the Middle East through district cooling projects in Dubai that utilize advanced meters for sustainable urban planning. South Africa dominates in Africa, focusing on industrial applications in Johannesburg to optimize energy use in mining and manufacturing, aided by international funding for green initiatives.

Competitive Analysis

The global Heat Meter market is dominated by players:

- Sycous Limited

- Zenner International GmbH & Co. KG

- Kamstrup

- Danfoss

- Apator SA.

- B Meters

- Itron

- Diehl Stiftung & Co. KG

- Siemens

- Trend Control Systems Ltd

- Premier Control Technologies Ltd

- Cosmic Technologies

- Grundfos

- Spire Metering Technology

- Omni Instruments

- Xi'an Kacise Optronics Tech Co., Ltd.

The global Heat Meter market is segmented as follows:

By Type

- Mechanical

- Static

- Others

By Connectivity

- Wired

- Wireless

- Others

By Application

- Residential

- Commercial

- Industrial

- Others

By Regional

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors