![]()

Search Market Research Report

Conveyor Systems Market Size, Share Global Analysis Report, 2026-2034

Conveyor Systems Market Size, Share, Growth Analysis Report By Type (Flat Belt Conveyors, Roller Conveyors, Wheel Conveyors, Vertical Conveyors, and Others), By Application (Food & Beverages, Pharmaceuticals, Supply Chain & Logistics, Manufacturing, Mining, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

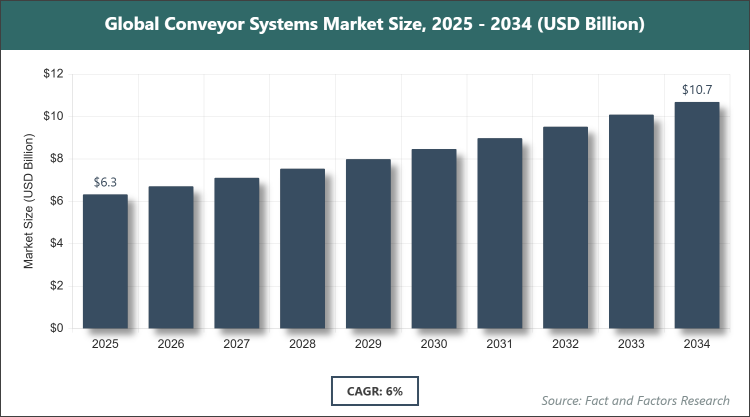

[220+ Pages Report] According to Facts & Factors, the global Conveyor Systems market size was estimated at USD 6.33 billion in 2025 and is expected to reach USD 10.61 billion by the end of 2034. The Conveyor Systems industry is anticipated to grow by a CAGR of 6.00% between 2026 and 2034. The Conveyor Systems Market is driven by increasing automation in manufacturing and logistics sectors.

Market Overview

Market Overview

Conveyor systems refer to mechanical handling equipment designed to move materials, products, or goods from one location to another within a facility or across different sites, enhancing efficiency in various industrial processes. These systems typically consist of belts, rollers, chains, or other mechanisms powered by motors or gravity, allowing for continuous or intermittent transportation of items in a controlled manner. They are integral to operations in warehouses, manufacturing plants, distribution centers, and airports, where they streamline workflows by reducing manual labor and minimizing handling errors. Conveyor systems can be customized for specific needs, such as handling bulk materials, unit loads, or specialized items, and often incorporate advanced features like sensors and automation for optimized performance.

Key Insights

- As per the analysis shared by our research analyst, the global Conveyor Systems market is estimated to grow annually at a CAGR of around 6.00% over the forecast period (2026-2034).

- In terms of revenue, the global Conveyor Systems market size was valued at around USD 6.33 billion in 2025 and is projected to reach USD 10.61 billion, by 2034.

- The market is driven by handling large volumes of goods in manufacturing and warehousing to reduce production time and labor costs.

- Based on the Type, Flat Belt Conveyors dominated the market in 2025 with a share of 31.98% as they provide endless, continuous belts for constant motion, suitable for diverse products and heavier loads made from materials like plastics, rubbers, metals, fabrics, and leather.

- Based on the Application, Supply Chain & Logistics dominated the market in 2025 with a share of 25.79% due to increasing automation, cost reduction, and its vital role in material handling across industrial processes.

- Based on the region, Asia Pacific dominated the market in 2025 with a share of 34.80% owing to the high concentration of manufacturing industries aiming to automate facilities amid rising human-resource costs.

Growth Drivers

- Automated Material Handling for Efficiency

The adoption of automated conveyor systems has significantly boosted market growth by enabling seamless handling of large volumes of goods in manufacturing, warehousing, and distribution environments. This automation reduces reliance on manual labor, minimizes errors, and accelerates production cycles, leading to cost savings and improved operational throughput. Industries such as e-commerce and logistics particularly benefit from these systems, as they facilitate quick sorting, packaging, and shipping processes to meet rising consumer demands for faster deliveries.

Furthermore, the integration of Industry 4.0 technologies, including IoT and AI, enhances conveyor functionalities by providing real-time monitoring and predictive maintenance, preventing downtime and extending equipment lifespan. This technological advancement not only optimizes warehouse space but also supports sustainable practices through energy-efficient designs, driving broader adoption across global supply chains.

Restraints

- Uncertainty in Global Trade Due to External Disruptions

Global trade uncertainties, exacerbated by events like the COVID-19 pandemic, have posed significant restraints on the conveyor systems market by disrupting supply chains and reducing demand for non-essential products. Lockdowns and restricted operations led to minimized industrial activities, causing delays in installations and upgrades of conveyor infrastructure.

Additionally, fluctuating raw material prices and logistical challenges have increased costs for manufacturers, making it difficult to maintain competitive pricing. These factors collectively hinder market expansion in the short term, as businesses prioritize essential operations over capital investments in automation.

Opportunities

- Expansion in Developing Economies Through Partnerships

Opportunities arise from the rapid industrialization in developing regions, where companies are increasingly adopting conveyor systems to enhance production efficiency and compete globally. Strategic acquisitions and partnerships allow key players to penetrate these markets, offering tailored solutions that address local needs such as cost-effective automation.

Moreover, the surge in demand for essential sectors like food & beverages and pharmaceuticals post-disruptions creates avenues for innovative conveyor designs that ensure hygiene and reliability. This trend supports long-term growth by fostering technological collaborations and expanding market reach.

Challenges

- Impact from Supply Chain Disruptions on Demand

Supply chain disruptions present ongoing challenges by affecting the availability of components and increasing lead times for conveyor system deployments. This results in project delays and higher operational costs for end-users, particularly in industries reliant on just-in-time manufacturing.

In addition, adapting to evolving safety standards and environmental regulations adds complexity to system designs, requiring continuous investment in R&D. These hurdles can slow market recovery and innovation pace in affected regions.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 6.33 Billion |

Projected Market Size in 2034 |

USD 10.61 Billion |

CAGR Growth Rate |

6.00% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Dürr Group (Germany), ATS Automation Tooling Systems Inc. (Canada), Daifuku Co., Ltd. (Japan), viastore SYSTEMS GmbH (Germany), TOYOTA INDUSTRIES CORPORATION (Japan), FlexLink (Sweden), KION GROUP AG (Germany), ERIKS North America, Inc (U.S.), Taikisha Ltd. (Japan), Conveyor Systems Ltd (England), and Others. |

Key Segment |

By Type, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Conveyor Systems market is segmented by type, application, and region.

Based on Type Segment, the Conveyor Systems market is divided into Flat Belt Conveyors, Roller Conveyors, Wheel Conveyors, Vertical Conveyors, and Others. The most dominant segment is Flat Belt Conveyors, holding a significant market share due to their versatility in handling a wide range of products, including heavy loads, with continuous and smooth operation that minimizes product damage and enhances efficiency in high-volume environments. This dominance drives the market by enabling cost-effective automation in diverse industries, reducing labor needs, and improving throughput. The second most dominant is Roller Conveyors, which excel in gravity-fed or powered applications for straight or curved paths, offering durability and low maintenance; their popularity stems from ease of integration in warehouses and assembly lines, contributing to market growth through flexible material handling solutions that support scalable operations.

Based on Application Segment, the Conveyor Systems market is divided into Food & Beverages, Pharmaceuticals, Supply Chain & Logistics, Manufacturing, Mining, and Others. The most dominant segment is Supply Chain & Logistics, capturing a substantial portion owing to the critical need for efficient sorting, distribution, and inventory management in e-commerce and global trade, where automated systems reduce costs and speed up processes. This segment propels the market by addressing the growing demand for optimized warehouse operations and real-time tracking. The second most dominant is Manufacturing, driven by the requirement for streamlined assembly lines and material flow in automotive and electronics sectors; it aids market expansion through enhanced productivity and integration with smart technologies like AI for predictive maintenance.

Recent Developments

- In July 2023, Dematic launched its Noise Reduction Portfolio, featuring 3D noise mapping and enhanced rollers, slats, and belts to reduce operational noise by up to 15 decibels, improving workplace environments in logistics and distribution centers.

- In June 2023, Dematic introduced third-generation freezer-rated Automated Guided Vehicles (AGVs) equipped with advanced sensors and navigation technology, exceeding global safety standards and enabling efficient operations in cold storage facilities.

- In May 2023, SSI SCHAEFER unveiled the SSI Piece Picking system, incorporating AI for object recognition, patented gripping mechanisms, and gentle handling to optimize picking accuracy in e-commerce and retail applications.

- In March 2023, Swisslog upgraded its CarryPick mobile robotic system, enhancing operating speed and efficiency for intralogistics, particularly in dynamic warehouse settings.

- In January 2023, SSI SCHAEFER acquired DS AUTOMOTION GmbH to strengthen its portfolio in autonomous mobile robotics and AGVs, expanding solutions for intralogistics and material handling.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific stands out as the leading region in the conveyor systems market, driven by rapid industrialization and a booming manufacturing sector that demands advanced automation to handle increasing production volumes. China emerges as the dominating country, with its vast network of automotive, electronics, and consumer goods manufacturers investing heavily in conveyor technologies to streamline operations and reduce labor dependencies. The region's emphasis on cost-effective solutions and technological integration further solidifies its position, as local firms collaborate with global players to adopt IoT-enabled systems for enhanced efficiency.

North America exhibits strong growth through widespread adoption of smart manufacturing practices, where conveyor systems are pivotal in optimizing supply chains across diverse industries like e-commerce and pharmaceuticals. The United States leads as the dominating country, benefiting from a mature infrastructure and high investments in AI and robotics to minimize downtime and boost productivity in warehouses and assembly lines. This region's focus on sustainability and energy-efficient designs also contributes to its robust market presence.

Europe maintains a competitive edge with its emphasis on precision engineering and regulatory compliance, fostering innovation in conveyor systems for sectors such as food processing and automotive. Germany is the dominating country, renowned for its engineering prowess and leadership in Industry 4.0 initiatives that integrate advanced sensors and automation for seamless material handling. The region's commitment to eco-friendly technologies and worker safety standards drives continuous advancements in system reliability.

Latin America is experiencing gradual expansion, supported by growing investments in mining and agriculture that require durable conveyor solutions for bulk material transport. Brazil dominates as the key country, leveraging its resource-rich economy to modernize logistics and manufacturing facilities with cost-effective systems. This progress is aided by international partnerships that introduce efficient technologies to enhance operational resilience.

The Middle East & Africa region is witnessing emerging growth, primarily fueled by infrastructure developments in oil & gas and logistics hubs. The United Arab Emirates leads as the dominating country, with its strategic ports and airports adopting high-tech conveyor systems to manage high-throughput operations efficiently. The focus on diversification beyond oil, through investments in smart warehouses, positions the region for sustained advancement in material handling capabilities.

Competitive Analysis

The global Conveyor Systems market is dominated by players:

- Dürr Group (Germany)

- ATS Automation Tooling Systems Inc. (Canada)

- Daifuku Co., Ltd. (Japan)

- viastore SYSTEMS GmbH (Germany)

- TOYOTA INDUSTRIES CORPORATION (Japan)

- FlexLink (Sweden)

- KION GROUP AG (Germany)

- ERIKS North America, Inc (U.S.)

- Taikisha Ltd. (Japan)

- Conveyor Systems Ltd (England)

The global Conveyor Systems market is segmented as follows:

By Type

- Flat Belt Conveyors

- Roller Conveyors

- Wheel Conveyors

- Vertical Conveyors

- Others

By Application

- Food & Beverages

- Pharmaceuticals

- Supply Chain & Logistics

- Manufacturing

- Mining

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors