![]()

Search Market Research Report

Concrete Fibers Market Size, Share Global Analysis Report, 2026-2034

Concrete Fibers Market Size, Share, Growth Analysis Report By Type (Steel Fibers, Synthetic Fibers, Glass Fibers, Natural Fibers, and Others), By Application (Concrete Reinforcement, Shotcrete, Precast Concrete, Pavements & Flooring, and Others), By End-User (Residential Construction, Commercial Construction, Industrial Construction, Infrastructure, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

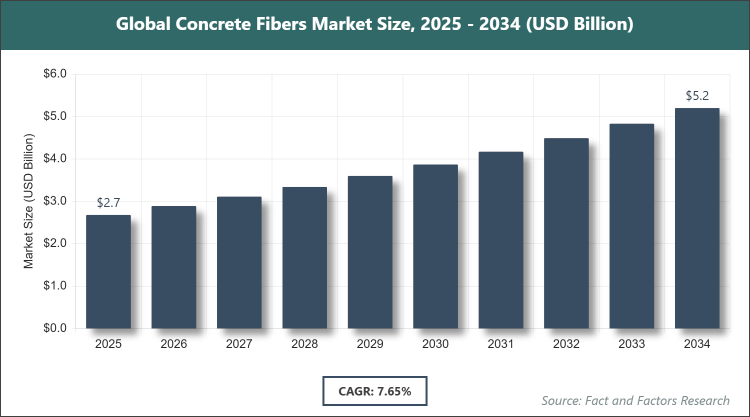

[241+ Pages Report] According to Facts & Factors, the global Concrete Fibers market size was estimated at USD 2.68 billion in 2025 and is expected to reach USD 5.19 billion by the end of 2034. The Concrete Fibers industry is anticipated to grow by a CAGR of 7.65% between 2026 and 2034. The Concrete Fibers Market is driven by increasing infrastructure development and the growing need for durable, crack-resistant concrete in construction projects.

Market Overview

Market Overview

The concrete fibers market refers to the global industry involved in the production, distribution, and application of discrete reinforcing fibers added to concrete mixtures to enhance mechanical properties such as tensile strength, flexural strength, toughness, impact resistance, fatigue resistance, and crack control. These fibers, ranging from steel to synthetic (polypropylene, nylon, polyester), glass, and natural (cellulose, sisal) types, are dispersed uniformly throughout the concrete matrix to provide three-dimensional reinforcement, reduce shrinkage cracking, improve durability, and in many cases partially or completely replace traditional steel rebar or welded wire mesh. The market serves a wide spectrum of construction applications, including industrial floors, pavements, precast elements, shotcrete, tunneling, residential/commercial slabs, and infrastructure projects, with ongoing innovation focused on high-performance macro-synthetic fibers, alkali-resistant glass fibers, and sustainable/bio-based alternatives to meet evolving demands for stronger, longer-lasting, and more environmentally responsible concrete.

Key Insights

- As per the analysis shared by our research analyst, the global Concrete Fibers market is estimated to grow annually at a CAGR of around 7.65% over the forecast period (2026-2034).

- In terms of revenue, the global Concrete Fibers market size was valued at around USD 2.68 billion in 2025 and is projected to reach USD 5.19 billion by 2034.

- The Concrete Fibers market is projected to witness significant growth due to booming global infrastructure spending and the shift toward high-performance, low-maintenance concrete solutions.

- Based on the Type, the Synthetic Fibers segment accounted for the largest market share of 44% due to excellent corrosion resistance, lower cost per unit volume compared to steel, and ease of dispersion in concrete.

- Based on the Application, the Pavements & Flooring segment dominated the market with the highest share, owing to the massive global demand for durable industrial floors, warehouse slabs, airport aprons, and road overlays that benefit significantly from fiber reinforcement.

- Based on the End-User, the Infrastructure segment held the leading position with a substantial share because of very large-scale public spending on highways, bridges, tunnels, ports, rail systems, and water infrastructure that require long-life, low-maintenance concrete.

- Based on the region, the Asia Pacific region captured around 48% market share, driven by massive infrastructure investment programs and the world’s largest concrete consumption in China and India.

Growth Drivers

- Massive Global Infrastructure Investment Wave

The world is in the midst of an unprecedented multi-trillion-dollar infrastructure build-out China’s Belt & Road Initiative and domestic mega-projects, India’s National Infrastructure Pipeline, U.S. Infrastructure Investment and Jobs Act, Europe’s NextGenerationEU and REPowerEU, Saudi Vision 2030 giga-projects, Africa’s Agenda 2063 corridors, and numerous other national plans all of which involve enormous volumes of concrete for highways, bridges, rail, ports, airports, water & wastewater facilities, data centers, and industrial plants. Fiber reinforcement is increasingly specified to extend service life, reduce maintenance, control cracking, and improve performance under heavy dynamic loads.

Additionally, governments and development banks are placing greater emphasis on lifecycle cost and sustainability rather than just initial construction cost, which strongly favors fiber-reinforced concrete over conventional reinforced concrete in many applications due to lower repair frequency and longer design life. This structural policy shift is one of the most powerful long-term drivers of fiber demand.

Restraints

- Higher Material Cost vs. Traditional Reinforcement

While fibers can reduce or eliminate conventional rebar in many slabs-on-ground, overlays, and precast elements, the direct material cost of high-performance macro-synthetic or steel fibers is still significantly higher per cubic meter of concrete than using conventional steel mesh or light rebar in some applications. This cost differential remains a barrier to adoption in price-sensitive public-sector projects and developing-country markets where initial capital is limited.

Moreover, the industry still faces a perception issue in some engineering communities that fibers are only a “secondary” reinforcement and cannot fully replace primary structural rebar in all load-bearing elements, limiting specification in certain critical structural applications despite growing code approvals and proven performance.

Opportunities

- Replacement of Traditional Mesh/Rebar in Flatwork & Precast

The single biggest near-to-mid-term growth opportunity lies in accelerating the substitution of welded wire mesh, light rebar mats, and conventional reinforcement cages with macro-synthetic fibers (and to a lesser extent steel fibers) in slabs-on-ground, industrial floors, warehouse floors, parking decks, precast barrier walls, septic tanks, utility vaults, box culverts, and other non-critical structural flatwork and precast elements. Design guides, ACI 360R, Eurocode provisions, and real-world performance are increasingly allowing engineers to eliminate conventional reinforcement in these applications when fibers are properly dosed.

Furthermore, the rapid growth of precast concrete construction (especially in India, Southeast Asia, the Middle East, and parts of Europe) creates a very large addressable market where fibers can be mixed at the batch plant, eliminating labor-intensive cage assembly and providing better crack control in thin elements.

Challenges

- Education Gap & Specification Inertia Among Engineers

Despite decades of research and thousands of successful projects, many structural engineers, public-works departments, and ready-mix producers remain hesitant to specify or allow fiber-only designs in place of conventional reinforcement due to lack of familiarity, conservative interpretation of codes, limited local case histories, or concern over long-term durability under certain exposure conditions. This specification inertia slows adoption even in applications where fibers are technically and economically superior.

Additionally, variability in fiber dispersion quality, incorrect dosage, poor mixing procedures, and inadequate finishing practices on job sites can still lead to sub-optimal performance, creating negative case studies that reinforce skepticism among conservative specifiers.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 2.68 Billion |

Projected Market Size in 2034 |

USD 5.19 Billion |

CAGR Growth Rate |

7.65% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Bekaert, Sika AG, GCP Applied Technologies (Saint-Gobain), Euclid Chemical (RPM International), BASF SE, ABC Fibers, Fabpro Polymers, FORTA Corporation, Owens Corning, BarChip Pty Ltd, Nycon Corporation, Fibercon International, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Concrete Fibers market is segmented by type, application, end-user, and region.

Based on Type Segment, the Concrete Fibers market is divided into Steel Fibers, Synthetic Fibers, Glass Fibers, Natural Fibers, and others. The most dominant segment is Synthetic Fibers, which holds the largest share due to their corrosion immunity, excellent crack-bridging performance at low dosages, ease of handling/mixing, and continuous price/performance improvement, driving the market by enabling rebar/mesh replacement in a wide range of flatwork and precast applications; the second most dominant is Steel Fibers, still preferred in very heavy-duty industrial floors and high-impact zones where highest flexural toughness and fatigue resistance are required.

Based on Application Segment, the Concrete Fibers market is divided into Concrete Reinforcement, Shotcrete, Precast Concrete, Pavements & Flooring, and others. The most dominant segment is Pavements & Flooring, commanding the highest share because industrial floors, warehouse slabs, airport pavements, container yards, and road overlays represent the single largest volume opportunity for macro-synthetic and steel fibers to replace mesh/rebar, drive the market by delivering the clearest cost/lifecycle savings; the second most dominant is Precast Concrete, growing rapidly due to faster production cycles, better surface quality, reduced reinforcement labor, and superior crack control in thin elements.

Based on End-User Segment, the Concrete Fibers market is divided into Residential Construction, Commercial Construction, Industrial Construction, Infrastructure, and others. The most dominant segment is Infrastructure, holding the biggest share due to enormous public spending on highways, bridges, tunnels, rail, ports, airports, and water infrastructure where long service life and minimal maintenance are critical, driving the market by creating very large, sustained project-based demand; the second most dominant is Industrial Construction, encompassing heavy manufacturing floors, logistics warehouses, power plants, refineries, and data centers that require ultra-durable, low-maintenance slabs.

Recent Developments

- In January 2025, Sika launched a new high-performance macro-synthetic fiber (SikaFiber® PP-480) specifically engineered for heavy-duty industrial floors with enhanced post-crack performance.

- In late 2024, GCP Applied Technologies (now part of Saint-Gobain) introduced STRUX® 90/40 synthetic macro-fiber with improved alkali resistance for long-life concrete overlays and pavements.

- In Q1 2025, Bekaert significantly expanded production capacity of Dramix® steel fibers in Asia to serve the fast-growing infrastructure market in India and Southeast Asia.

- In 2025, Euclid Chemical released a new alkali-resistant glass fiber bundle for shotcrete and precast applications exposed to aggressive environments.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific is the largest and fastest-growing region in the concrete fibers market, with China as the dominant country due to its unparalleled scale of concrete consumption, massive infrastructure investment (high-speed rail, highways, bridges, ports, airports, mega-cities), rapid urbanization, and government mandates to improve construction quality and durability. Domestic synthetic and steel fiber producers have scaled aggressively, while international leaders are building local capacity. India is the second-largest growth engine thanks to the National Infrastructure Pipeline, Bharatmala highway program, smart cities, metro rail expansion, and increasing specification of fibers in industrial floors and precast elements.

North America remains a high-value, technologically advanced market led by the United States through the Infrastructure Investment and Jobs Act, strong industrial & logistics construction, very large warehouse and data-center boom, airport modernization, and widespread adoption of macro-synthetic fibers in slabs-on-ground to replace mesh. Canada benefits from mining and oil & gas infrastructure.

Europe shows steady, quality-focused growth, dominated by Germany due to its world-class engineering standards, strong precast industry, extensive road & rail maintenance programs, tunneling projects, and early adoption of high-performance synthetic fibers in industrial floors and overlays. Nordic countries lead in sustainable construction applications.

Latin America is accelerating, led by Brazil through large infrastructure concessions (highways, ports, airports), mining expansions, and growing precast sector. Mexico benefits from nearshoring-driven manufacturing construction.

The Middle East & Africa region is growing rapidly due to giga-projects and energy diversification, with Saudi Arabia as the dominant country through Vision 2030 (NEOM, Red Sea, Qiddiya, sports cities) and massive concrete volumes requiring durable, low-maintenance solutions in extreme climatic conditions.

Competitive Analysis

The global Concrete Fibers market is dominated by players:

- Bekaert

- Sika AG

- GCP Applied Technologies (Saint-Gobain)

- Euclid Chemical (RPM International)

- BASF SE

- ABC Fibers

- Fabpro Polymers

- FORTA Corporation

- Owens Corning

- BarChip Pty Ltd

- Nycon Corporation

- Fibercon International

The global Concrete Fibers market is segmented as follows:

By Type

- Steel Fibers

- Synthetic Fibers

- Glass Fibers

- Natural Fibers

- Others

By Application

- Concrete Reinforcement

- Shotcrete

- Precast Concrete

- Pavements & Flooring

- Others

By End-User

- Residential Construction

- Commercial Construction

- Industrial Construction

- Infrastructure

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Bekaert

- Sika AG

- GCP Applied Technologies (Saint-Gobain)

- Euclid Chemical (RPM International)

- BASF SE

- ABC Fibers

- Fabpro Polymers

- FORTA Corporation

- Owens Corning

- BarChip Pty Ltd

- Nycon Corporation

- Fibercon International

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors