![]()

Search Market Research Report

Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) Market Size, Share Global Analysis Report, 2026-2034

Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) Market Size, Share, Growth Analysis Report By Type (Direct ORC Systems, Indirect ORC Systems, Cascaded ORC Systems, and Others), By Application (Waste Heat Recovery, Geothermal Power, Biomass Power Generation, Solar Thermal, Marine and Transport, District Heating, and Others), By End-User Industry (Industrial, Power Generation Utilities, Oil and Gas, Commercial and District Energy, Maritime, Data Centers, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

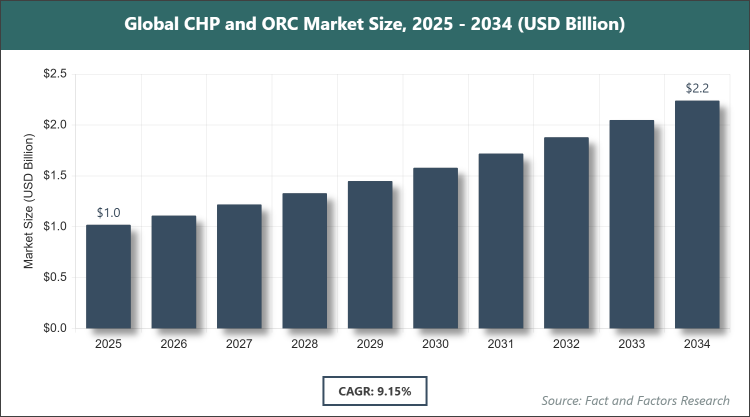

[235 Pages Report] According to Facts & Factors, the global Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market size was estimated at USD 1.02 billion in 2025 and is expected to reach USD 2.26 billion by the end of 2034. The Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) industry is anticipated to grow by a CAGR of 9.15% between 2026 and 2034. The Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) Market is driven by policy momentum on industrial decarbonization and stricter emission rules.

Market Overview

Market Overview

The Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market encompasses technologies that enhance energy efficiency by capturing and utilizing waste heat for power generation. CHP systems produce both electricity and useful thermal energy from a single fuel source, while ORC technology employs organic fluids to convert low-grade heat into electricity, making it ideal for applications where traditional steam cycles are inefficient. This market addresses the need for sustainable energy solutions in industrial, commercial, and renewable sectors, promoting reduced energy consumption and lower environmental impact through integrated heat and power processes.

Key Insights

- As per the analysis shared by our research analyst, the global Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is estimated to grow annually at a CAGR of around 9.15% over the forecast period (2026-2034).

- In terms of revenue, the global Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market size was valued at approximately USD 1.02 billion in 2025 and is expected to reach USD 2.26 billion by 2034.

- The market is driven by stricter emission rules and investments in low-temperature renewable power.

- Based on the type, Indirect ORC Systems dominated with 46.1% share, due to robustness in 300-400°C applications like cement and petrochemical processes, reducing maintenance needs.

- Based on the application, Waste Heat Recovery dominated with 46.5% share, for energy savings in smelters and enabling efficient utilization of industrial exhaust.

- Based on the end-user industry, Industrial dominated with 53.2% share, converting furnace exhaust into electricity and supporting decarbonization goals.

- Based on region, North America dominated with 42.9% share, supported by tax incentives like U.S. Production Tax Credit and Canada's Clean Technology Investment Tax Credit.

Market Dynamics

Growth Drivers

- Stricter Emission Rules

The global push for stricter emission regulations is accelerating the adoption of CHP and ORC technologies, as they enable significant reductions in carbon footprints across high-emission industries. These systems allow for efficient waste heat capture, transforming otherwise lost energy into usable power, which aligns with international climate agreements and national policies aimed at curbing greenhouse gases. This driver fosters innovation in fluid selection and system design to meet evolving standards, enhancing overall market appeal.

In addition, regulatory frameworks incentivize investments in low-emission technologies, leading to widespread integration in sectors like manufacturing and energy production. As compliance becomes mandatory, companies are increasingly turning to CHP and ORC solutions to avoid penalties and achieve sustainability targets, thereby propelling market growth through expanded applications and technological advancements.

- Geothermal and Biomass Expansion

The expansion of geothermal and biomass energy sources is fueling demand for ORC systems within CHP frameworks, as these renewable resources provide consistent low-temperature heat ideal for ORC conversion. This integration supports diversified energy portfolios, reducing reliance on fossil fuels and enhancing grid stability in remote or resource-rich areas. The driver emphasizes sustainable development, attracting investments in green infrastructure.

Moreover, advancements in binary cycle technologies optimize efficiency in geothermal plants, while biomass applications benefit from organic fluid adaptability to variable heat sources. This trend not only boosts energy output but also contributes to rural economic development through job creation and local resource utilization, driving long-term market expansion.

- Government Subsidies

Government subsidies and incentives are pivotal in lowering barriers to entry for CHP and ORC deployments, making these technologies more financially viable for end-users. Programs offering tax credits and grants encourage adoption in both developed and emerging markets, stimulating research and scaling of efficient systems. This support accelerates market penetration by addressing initial cost concerns.

Furthermore, policy alignments with clean energy goals foster public-private partnerships, leading to innovative financing models and broader accessibility. As subsidies evolve to prioritize decarbonization, they enhance competitiveness against traditional power generation methods, sustaining growth momentum in the sector.

- Industrial Decarbonization Targets

Industrial sectors are increasingly committing to decarbonization targets, driving the integration of CHP and ORC for efficient heat recovery and reduced emissions. These technologies enable on-site power generation, minimizing transmission losses and supporting circular economy principles in heavy industries. This driver underscores the shift toward sustainable manufacturing practices.

Additionally, the focus on net-zero ambitions prompts upgrades to existing infrastructure, incorporating hybrid systems that combine CHP with ORC for optimal performance. This evolution not only improves operational efficiency but also enhances corporate sustainability profiles, attracting eco-conscious investments and propelling market advancement.

Restraints

- High Upfront CAPEX

High initial capital expenditures pose a significant barrier to widespread adoption of CHP and ORC systems, particularly in cost-sensitive markets where return on investment timelines may extend beyond short-term financial planning. This restraint limits scalability for small and medium enterprises, despite long-term savings in energy costs.

Moreover, inflationary pressures on components like turbines and seals exacerbate affordability issues, delaying project implementations. While incentives help mitigate this, the need for customized engineering further elevates costs, hindering market growth in regions with limited financing options.

- Shortage of Skilled EPC Contractors

The shortage of skilled engineering, procurement, and construction (EPC) contractors for complex CHP and ORC installations creates bottlenecks in project execution, leading to prolonged lead times and increased risks. This challenge stems from an aging workforce and competition from other renewable sectors.

In response, industry efforts toward training and modular designs aim to alleviate this, but persistent gaps affect deployment efficiency. As demand rises, this restraint could impede timely market expansion unless addressed through targeted education and collaboration initiatives.

- Supply Bottlenecks for Seals and Expanders

Supply chain constraints for critical components like seals and expanders, often sourced from concentrated manufacturing hubs, disrupt production and increase costs for CHP and ORC systems. This restraint is amplified by geopolitical factors and material shortages.

Efforts to diversify suppliers and invest in local production are underway, but ongoing vulnerabilities pose risks to project timelines. This dynamic challenges market stability, necessitating strategic stockpiling and innovation in component alternatives.

- Regulatory Uncertainty over PFAS Refrigerants

Uncertainty surrounding regulations on per- and polyfluoroalkyl substances (PFAS) in refrigerants affects fluid selection in ORC systems, potentially requiring costly transitions. This restraint impacts confidence in long-term investments, particularly in stringent regions.

Adaptation through research into alternatives like super-critical CO2 helps, but transitional costs and compliance complexities slow adoption. This factor underscores the need for clear policy guidance to sustain growth trajectories.

Opportunities

- Integration with Solar-Thermal Hybrids

Opportunities arise from integrating ORC with solar-thermal hybrids to achieve higher efficiency in variable heat environments, expanding applications in sunny regions. This synergy enhances reliability and output, attracting investments in renewable hybrids.

Such developments open new markets for district energy and off-grid solutions, leveraging technological convergence to meet diverse energy needs. This opportunity drives innovation and market diversification.

- District Heating in Nordic Regions

The potential for ORC in district heating networks, especially in cold climates like Nordic countries, offers growth avenues by utilizing low-grade heat for communal systems. This application supports urban sustainability goals.

Collaborations with local utilities can scale implementations, reducing heating costs and emissions. This opportunity strengthens regional market positions through tailored solutions.

- Data-Center Heat-to-Power

Emerging opportunities in data centers involve converting server waste heat to power via ORC, addressing high energy demands and sustainability mandates. This niche drives specialized system designs.

Partnerships with tech giants enable pilot projects, potentially leading to widespread adoption. This trend capitalizes on digital growth for market expansion.

Challenges

- Labor Shortages and Supply Chain Constraints

Persistent labor shortages in skilled trades challenge timely deployments of CHP and ORC projects, compounded by supply chain disruptions. This affects scalability and cost management.

Strategies like automation and global sourcing mitigate impacts, but ongoing issues require industry-wide resilience building. This challenge tests operational adaptability.

- Regulatory Shifts on Refrigerants

Evolving regulations on refrigerants demand fluid substitutions, posing technical and financial challenges for existing ORC installations. This requires proactive R&D.

Industry responses include transitioning to eco-friendly options, but adaptation timelines may delay growth. This dynamic necessitates agile compliance strategies.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.02 Billion |

Projected Market Size in 2034 |

USD 2.26 Billion |

CAGR Growth Rate |

9.15% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Turboden S.p.A., Ormat Technologies Inc., Exergy S.p.A., Kaishan Compressor Co. Ltd., ElectraTherm Inc., and Others. |

Key Segment |

By Type, By Application, By End-User Industry, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is segmented by type, application, end-user industry, and region.

Based on Type Segment, the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is divided into Direct ORC Systems, Indirect ORC Systems, Cascaded ORC Systems, and others. The most dominant segment is Indirect ORC Systems with 46.1% share, followed by Cascaded ORC Systems as the second most dominant. Indirect systems dominate because of their ability to handle higher temperature ranges effectively in industrial processes, offering lower maintenance and higher reliability, which drives the market by enabling broader adoption in energy-intensive sectors and contributing to overall efficiency gains and cost reductions.

Based on Application Segment, the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is divided into Waste Heat Recovery, Geothermal Power, Biomass Power Generation, Solar Thermal, Marine and Transport, District Heating, and others. The most dominant segment is Waste Heat Recovery with 46.5% share, followed by Geothermal Power as the second most dominant. Waste Heat Recovery dominates due to its direct applicability in capturing industrial exhaust for power generation, reducing energy waste and operational costs, which propels market growth by aligning with global efficiency and sustainability initiatives.

Based on End-User Industry Segment, the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is divided into Industrial, Power Generation Utilities, Oil and Gas, Commercial and District Energy, Maritime, Data Centers, and others. The most dominant segment is Industrial with 53.2% share, followed by Power Generation Utilities as the second most dominant. The Industrial segment dominates owing to its high demand for on-site energy recovery from processes like manufacturing and refining, enhancing productivity and reducing emissions, thereby driving the market through widespread integration in heavy industries.

Recent Developments

- July 2025: European Commission allocated EUR 1 billion to Industrial Decarbonization Bank for waste-heat projects favoring ORC.

- June 2025: Canada enacted 30% Clean Economy Investment Tax Credits for ORC equipment.

- May 2025: Ormat reported USD 150.3 million Q1 EBITDA and acquired 20 MW Blue Mountain geothermal plant for USD 88 million.

- February 2025: U.S. Treasury finalized clean-electricity credits for ORC plants post-2025.

Regional Analysis

- North America to dominate the global market

North America dominates the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market, with the United States leading through its advanced infrastructure and supportive policies for renewable integration. The region's focus on energy security and innovation in waste heat technologies fosters widespread adoption across industries. Strong R&D ecosystems and collaborations between government and private sectors enhance system efficiencies. Additionally, the presence of vast geothermal resources bolsters market leadership. Overall, North America's commitment to clean energy transitions solidifies its position.

Europe exhibits robust growth in the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market, led by Germany with its emphasis on industrial efficiency and renewable mandates. The region's integrated energy policies promote district heating and waste recovery applications. Collaborative frameworks among EU nations drive technological advancements and cross-border projects. Focus on circular economy principles accelerates ORC deployments in manufacturing hubs. Europe's proactive stance on climate goals ensures sustained market development.

Asia Pacific is experiencing rapid expansion in the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market, with China dominating through large-scale industrial and geothermal initiatives. The region's burgeoning manufacturing sector demands efficient heat recovery solutions. Government incentives for green technologies spur investments in biomass and solar integrations. Urbanization trends amplify district energy needs. Asia Pacific's dynamic economic growth supports innovative ORC applications.

Latin America shows promising potential in the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market, led by Brazil with its biomass-rich resources and renewable focus. The region leverages agricultural waste for energy generation, enhancing sustainability. International funding aids infrastructure development for geothermal projects. Industrial sectors adopt ORC for cost savings. Latin America's transition toward cleaner energy sources drives gradual market uptake.

The Middle East & Africa region is emerging in the Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market, with Saudi Arabia leading through diversification efforts beyond oil. Geothermal and waste heat applications gain traction in industrial zones. Multilateral partnerships facilitate technology transfers for remote power needs. Focus on water desalination integrates ORC systems. The region's resource endowments support targeted growth.

Competitive Analysis

The global Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is dominated by players:

- Turboden S.p.A.

- Ormat Technologies Inc.

- Exergy S.p.A.

- Kaishan Compressor Co. Ltd.

- ElectraTherm Inc.

- Enertime SA

- Triogen B.V.

- General Electric Company

- Siemens Energy AG

- Climeon AB

- Againity AB

- Zuccato Energia Srl

- Enogia SAS

- Spirax-Sarco Engineering plc

- Atlas Copco AB (Opcon ORC)

- CycloPower Ltd.

- Air Squared Inc.

- Infinite Power Systems

The global Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is segmented as follows:

By Type

- Direct ORC Systems

- Indirect ORC Systems

- Cascaded ORC Systems

- Others

By Application

- Waste Heat Recovery

- Geothermal Power

- Biomass Power Generation

- Solar Thermal

- Marine and Transport

- District Heating

By End-User Industry

- Industrial

- Power Generation Utilities

- Oil and Gas

- Commercial and District Energy

- Maritime

- Data Centers

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Combined Heat and Power (CHP) and Organic Rankine Cycle (ORC) market is dominated by players:

- Turboden S.p.A.

- Ormat Technologies Inc.

- Exergy S.p.A.

- Kaishan Compressor Co. Ltd.

- ElectraTherm Inc.

- Enertime SA

- Triogen B.V.

- General Electric Company

- Siemens Energy AG

- Climeon AB

- Againity AB

- Zuccato Energia Srl

- Enogia SAS

- Spirax-Sarco Engineering plc

- Atlas Copco AB (Opcon ORC)

- CycloPower Ltd.

- Air Squared Inc.

- Infinite Power Systems

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors